The Iran war: where next for aviation?

BA’s first 787, G-ZBJB, about to commence its delivery flight from Boeing back in June 2013 (personal photo)

Taking stock after two months

It has now been two months since the Iran war started. Airline management teams will have been busy dealing with the immediate consequences. Suspending flights to the region, rerouting flights away from the area, dealing with disrupted passengers and putting up prices in response to the doubling of fuel prices. All pretty standard stuff for an experienced airline team.

At the start, I think most airlines were assuming that this would be a short-lived spike in fuel prices. The war would be over pretty quickly and things would get “back to normal” within a few weeks, or months at the most. Whilst that scenario is still a possibility, more and more airlines are beginning to face up to the potential for a long, sustained period of high fuel prices. Something that might even get worse before it gets better.

I thought it would be a good time to reflect on some of the issues they’ll be considering and what we might expect them to do when it comes to capacity.

Where are fuel prices now and where might they be going?

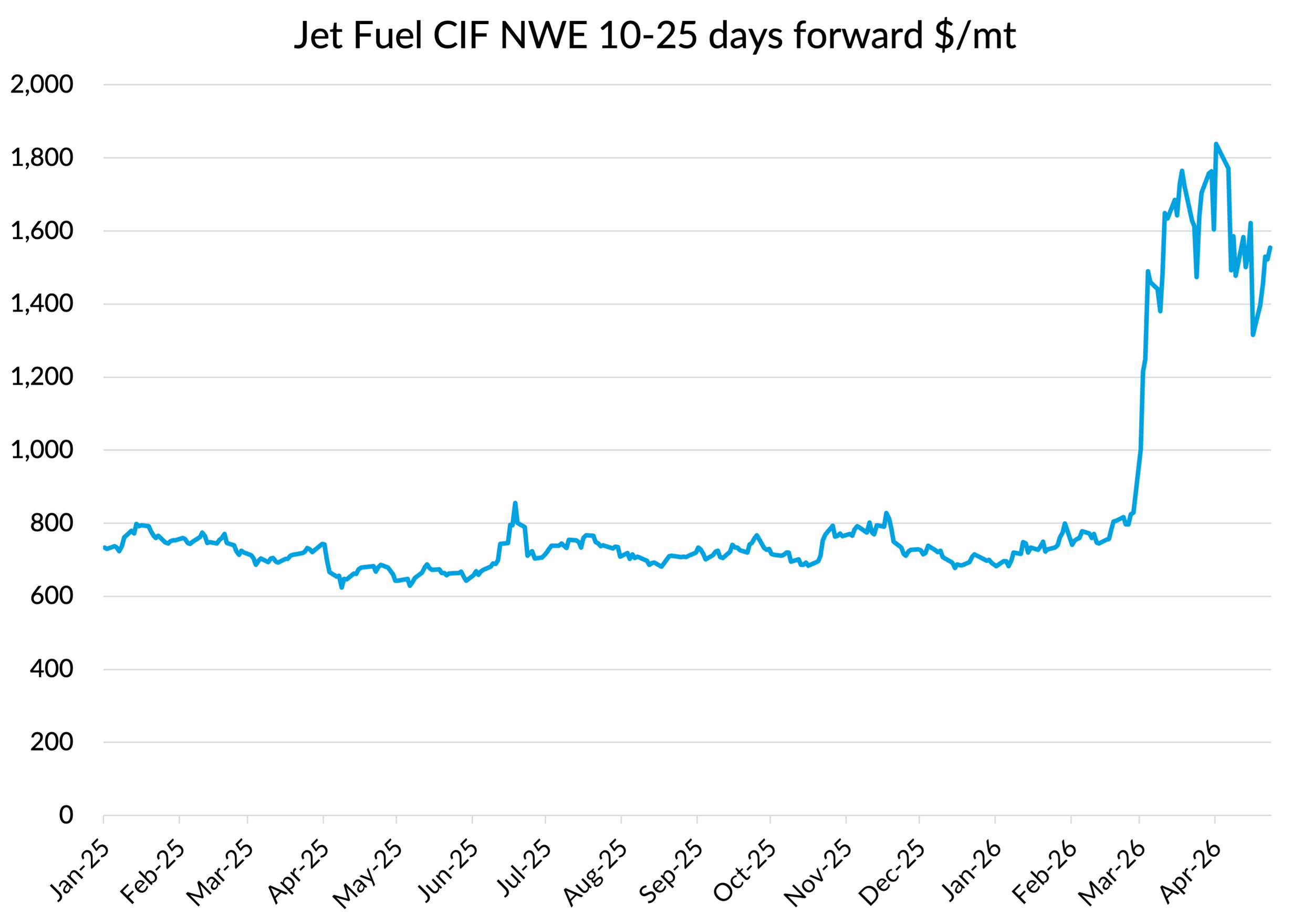

To some extent, the fuel price has already fallen back from its peaks, with current spot prices for jet fuel in Europe running at $1,555, down from a peak of over $1,800 at the start of the month. But the recent trend is actually up, as optimism that the Strait of Hormuz might reopen soon begins to fade.

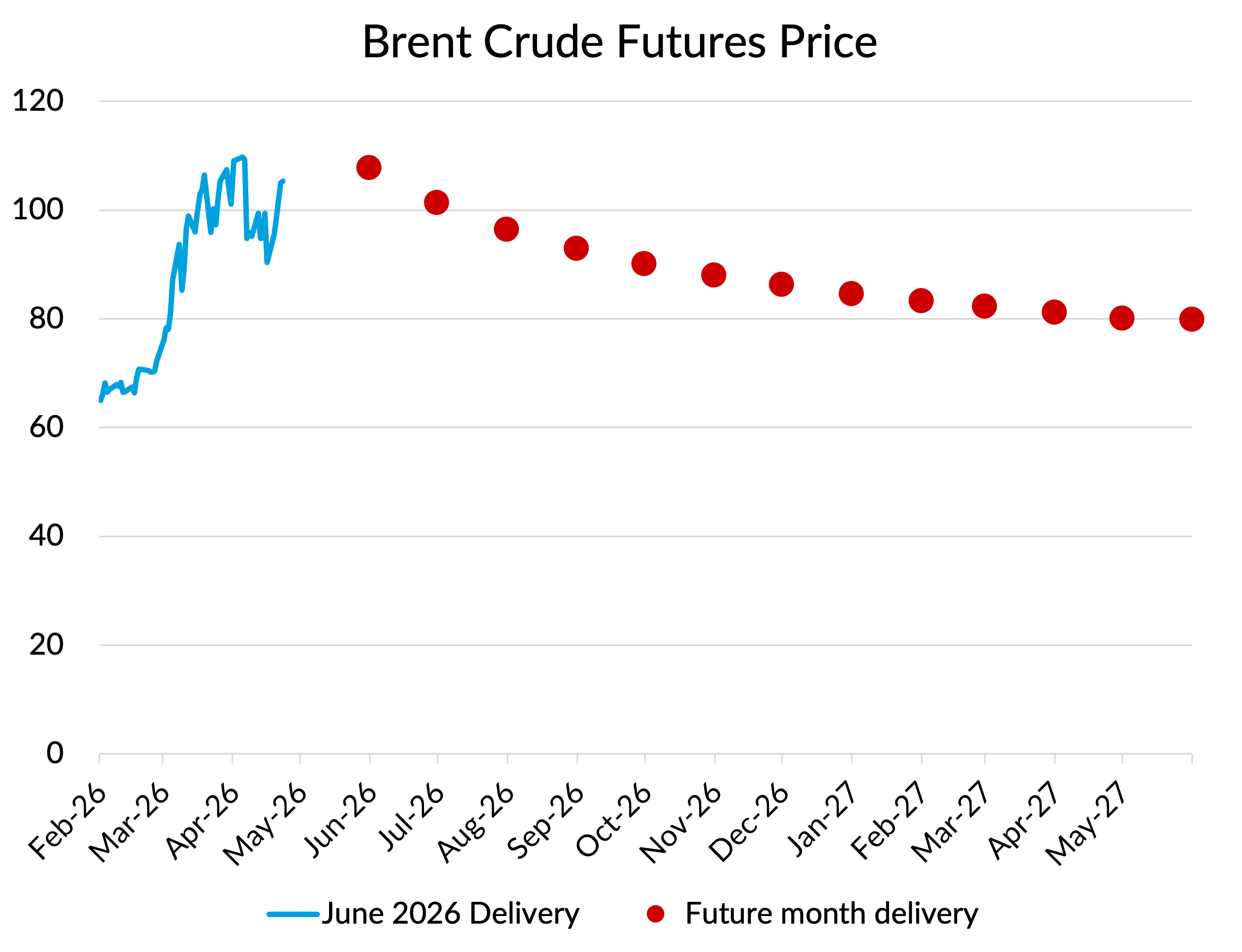

Looking forward, oil futures markets seem to be anticipating further moderation of crude oil prices over time. The blue line on the following chart shows the price of the June 2026 Brent futures contract. At the start of February, you could buy the contract at $65 and you’d have to pay $105 today. The red markers on the chart show the prices you’d have to pay today for Brent in future months, with prices following a steady downward path the further out you go. Not all the way back to pre-war levels, but at $80, in the sort of territory that most airlines would view as “normal”.

But oil analysts are now getting more jittery. Yesterday, Goldman Sachs warned that oil could trade at $120 a barrel later this year if peace talks fail to make progress. Even if exports from the Gulf normalise by the end of June, Goldman now forecasts oil prices ending the year at $90, up from its earlier $80 forecast.

The crude oil price is also only part of the story. Around 65% of the increase in jet prices has been down to the widening of the jet fuel “crack spread”, the gap between crude oil prices and the price of the refined product. That’s because the shortfall in supply from the Middle East is bigger for jet fuel than it is for crude and it’s not easy for other parts of the world to make up the difference due to constraints in refinery capacity. Whilst the futures market for crude oil may be showing a decline over time, futures for refined products like gasoil are not showing the same, suggesting crack spreads are likely to remain inflated.

Risks to physical supply

The media has been full of speculation about whether airlines are going to be facing physical fuel shortages over the summer. I’ve held off writing about this because the messages are frankly quite conflicting. Publicly, airlines in Europe generally insist that they are not experiencing fuel shortages, at least not now and not in the next month or so. Airlines are trying to keep customers and investors calm. But in private, they are also lobbying governments to do more to deal with supply risks.

Inventories of fuel and lags in the system mean that it takes time for lost supply from the Middle East to show up in shortages in Europe. The flip side is that even if the Strait of Hormuz is fully reopened in the near future, it will be over a month before the next deliveries arrive, as the "air pocket" of lost supply travels through the system at the pace of a supertanker.

The big question is whether the lost supply of jet fuel from the Middle East can be replaced by higher imports from the USA, Nigeria and elsewhere. According to Argus, only half of the lost jet fuel supply has so far been replaced, with jet fuel shortages in Europe predicted for June “on current trends”.

Europe imports about a third of its jet fuel and 75% of that was coming from the Gulf before the war. Losing half of that would mean a reduction in overall supply of 12%. Is there sufficient headroom in Europe's local refineries to make up for that? Or additional supply that can be sourced from other geographies? And of course, even if the refinery constraints can be overcome, the crude oil also needs to be there to support it.

For what it is worth, I think it is right to consider fuel shortages as a risk, but widespread shortages are not something we should be expecting. Airlines seem to have visibility on supply for June and governments are seeking to reassure travellers. The UK’s Department for Transport issued this statement last Friday:

“There is no current need for passengers to change their travel plans. UK airlines buy jet fuel in advance, and airports maintain stocks to support their resilience. The government is working closely with the aviation industry to monitor risks and minimise disruption to passengers.”

The peak months of July and August will be the point of maximum risk. Fuel demand will start to drop anyway once the peak travel season has passed, and if fuel prices remain where they are, airlines will start to cut capacity heading into the winter. That will help bring demand and supply into balance over time.

Let’s look at what we might expect on capacity adjustments next.

Capacity adjustments

Firstly, I want to remind you that if airlines are behaving rationally, their hedging position should not really be relevant to capacity decisions. Those should be made using the marginal price of fuel (i.e. spot/future), not the blended price including hedging. I explained why in a recent article, but basically for any given fuel price, the hedging gain is a fixed amount of money which doesn’t depend on the volume of fuel actually consumed.

The first port of call for a network planner is to look at any routes that are making a marginal loss at the new fuel price (i.e. revenues not covering variable costs). Even with a doubling of the fuel price, there won’t be much that meets that test during the summer months. Let me illustrate why with a some example numbers based on the easyJet network.

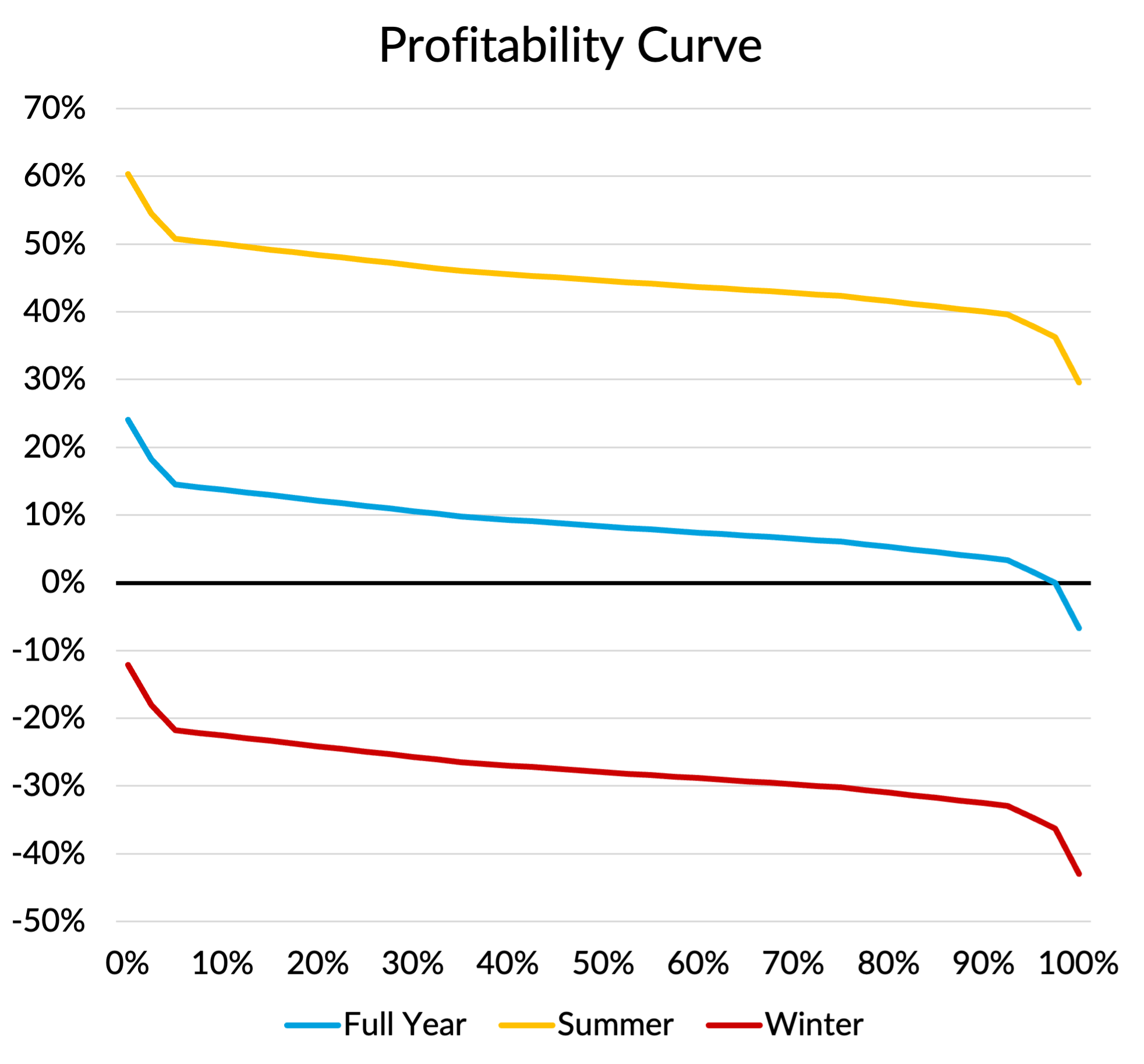

A few years ago easyJet published a slide in an investor presentation showing the profitability profile of their network, as measured by ROIC (Return on Invested Capital). I took the shape of that curve and adjusted it to match the slightly higher ROIC outturn for easyJet’s last financial year ending in September 2025. That’s shown as the blue line on the chart below. The blue line crosses the 0% ROIC line at 90% on the x-axis, meaning that only 10% of their capacity made a loss on a full year basis.

I’ve also shown a summer and a winter curve, keeping the same shape but adjusting for the difference in easyJet’s H2 (summer) and H1 (winter) margins. Whilst the precise shapes of the winter/summer curves are probably not quite right, my main point is the huge difference in the overall level of profitability.

A doubling of fuel prices with 50% pass through to ticket prices would only push the summer curve down to the blue curve. Exclude fixed costs and you’d be back up to the yellow curve again. So on a marginal basis, pretty much everything should still be making a solid contribution during the summer, even at current fuel prices.

The story will of course be very different in the winter season. The red line above shows nothing making money even before allowing for higher fuel prices. But excluding fixed costs, the winter line would look more like the blue curve - i.e. almost everything in 2025 still worked on a marginal basis in the winter, which is why easyJet was flying it.

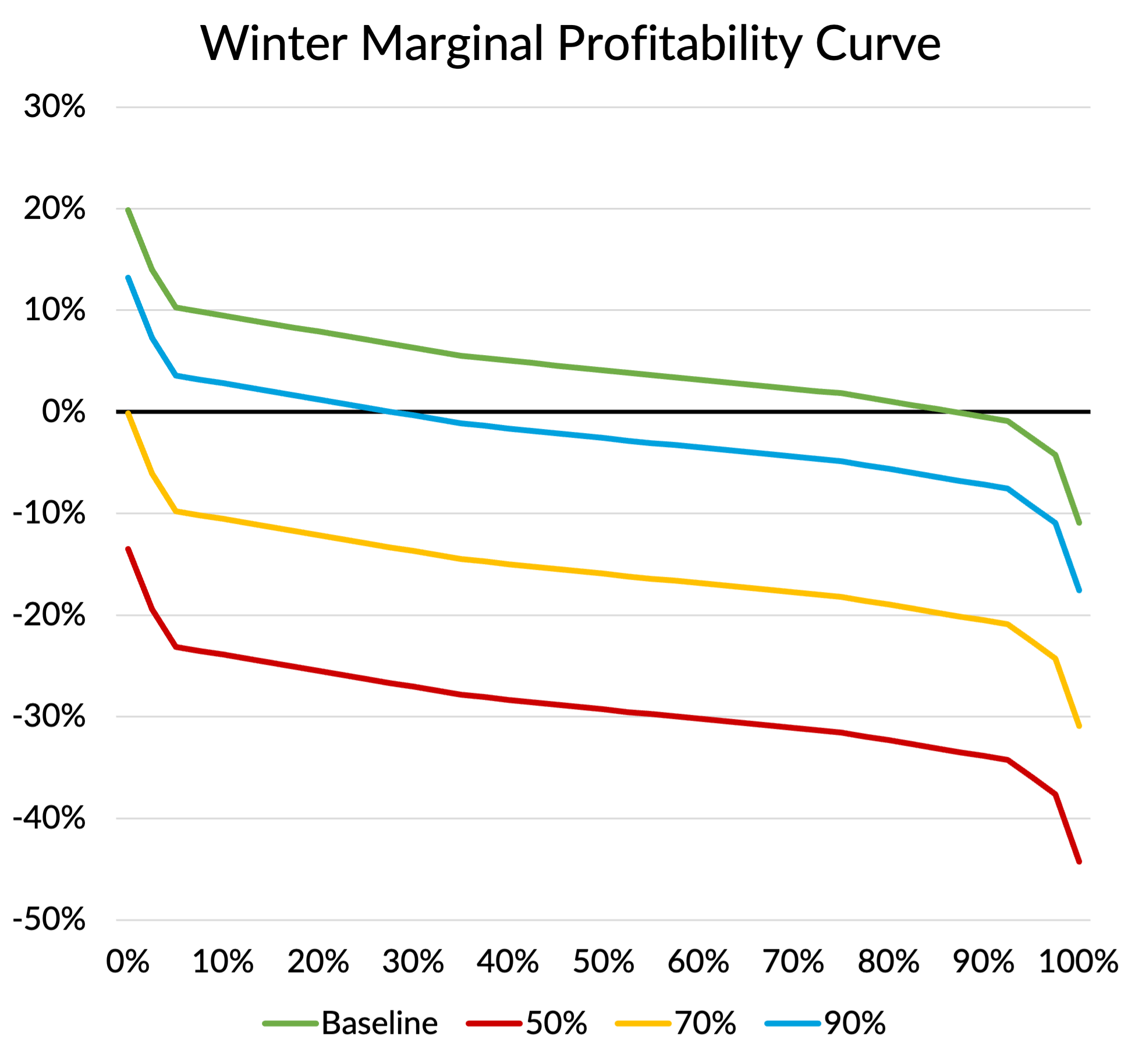

But add a doubling of fuel costs and much of the winter flying would be underwater. On the following chart (in green) I’ve shown an estimate of a 2025 winter marginal contribution curve. I’ve then added three lines where I’ve doubled fuel costs and assumed different rates of fuel cost pass-through (50%, 70% and 90%). You can see that even with a 90% pass-through rate (the blue line), 70% of easyJet’s network would be making a marginal loss in the winter. That means they’d be better off not flying it, at least in terms of short-term profitability.

Different airlines will have different seasonality profiles as well as different starting points for profitability. Lufthansa Group for example has announced the cancellation of 20,000 flights over the next 6 months in response to the spike in fuel prices. But the cancelled flights represented less than 1% of capacity and they were all flown by its regional operator, CityLine, a loss-making unit that was due to close anyway next year. CityLine is more of a business airline, where results in summer months are likely to be below average if anything.

All this is only illustrative of course, but I hope I’ve demonstrated why airlines really do need to find a way to pass on the vast majority of such a big fuel price increase in higher ticket prices. If they don’t, most off-peak flying won’t make any financial sense, even on a marginal contribution basis.

Consolidating flights

The other thing I should say is that “deleting the worst routes” is not going to be a major part of the adjustment process. Yes, there will be routes that were pretty marginal already, and can’t be rescued (like Lufthansa’s Frankfurt to Bydgoszcz route perhaps). But “revenue recapture” is generally required to make the economics of cutting capacity work. Take a route with one daily flight and delete it and you’ll lose all the revenue. Take a route with four daily flights and cut it to three and a proportion of the passengers you would have carried on the cancelled flight will be retained on the other three. The rate of recapture depends on load factors - if all the flights are booked at 90% load factors, the economics of consolidating flights is not going to work. But four flights with a 70% load factor will fit on three without much revenue “spill”.

I think a good way to think about the process going on in airlines is that they are pushing up the prices, watching how demand (and competitors) respond, and then adjusting capacity on each route by reducing frequency or substituting smaller aircraft to bring load factors back up as necessary. That’s a process that will take time to work its way through the system and will mainly play out as we go into the winter season.

What kind of capacity reduction might that process lead to?

Fully passing on a doubling of fuel prices for an airline like easyJet would need an extra £24 per passenger of revenue, equivalent to a 26% price increase. It doesn’t really matter how that is made up, but it is likely to be some combination of higher fares and higher baggage and other fees. Assuming that all airlines will be trying to raise prices by similar amounts, we can use a “whole market” elasticity factor to estimate the impact on demand. A 26% price increase would be expected to lead to a 24% reduction in demand, using a the -0.924 whole market elasticity assumption estimated by IATA for the intra European market.

I don’t think easyJet or any other airline will be planning to cut capacity by anything like 24%, but it does give you an idea for the potential scale of adjustment that might be required if fuel prices remain elevated, or even go up from here.

There will be some differences depending on the traffic mix. For airlines with substantial business traffic, fuel costs make up a lower percentage of revenue, so the required price rise will be lower and demand may also be less price elastic. At the other extreme, the lowest cost competitors will hope that financially weaker and higher cost carriers do more of the heavy lifting of removing capacity from the market, including by going bust and ceasing operations.

Airline strategists will also be loathe to take a hatchet to their networks for what could still be a temporary spike in fuel prices. Airlines which are well hedged and/or have strong balance sheets will have the option of taking a more strategic approach, letting competitors who face more immediate financial pressures make the first moves on capacity reduction.

In such an uncertain environment, trying to work out an optimal capacity adjustment is a bit of a mug’s game anyway. I suspect that round numbers will exert their usual attraction and we’ll see a lot of 5%, 10% and 15% adjustments for the winter season. For the next few months, I expect very small adjustments (at least for airlines in the Northern Hemisphere), with individual weakly booked flights being cancelled. The job of airline planners will be greatly facilitated if the “use it or lose it” slot rules are relaxed, as airlines have requested. The weakest performing flights with low load factors understandably tend to be the flights that get cancelled in the case of disruption. That means that they will be ones that are already “closest to the edge” under the slot rules.

Longer-term changes

Airlines may have to make more significant adjustments to their capacity and business plans If oil and fuel prices remain high going into 2027 and beyond, especially if this triggers a global recession. Over a 3-6 month timeframe, there is not much that can be done about fixed costs. That’s why they are called fixed. But as the lead time to take action extends, more costs become at least potentially variable.

The biggest fixed cost that becomes mostly variable over a 1-2 year time horizon is fleet. Leases which might have been renewed can be left to lapse instead. Orders that might have been made can be delayed. Existing orders can be rescheduled. Old aircraft can be retired earlier than previously planned.

How airlines best adjust their fleet plans in response to a more challenging economic environment depends a lot on the “shape” of those challenges. A “classic” recession scenario triggered by central banks pushing up interest rates to tackle rising inflation will see a reduction in demand as customers cut back on travel, higher interest rates will make the financing of new aircraft more expensive, and energy costs might also be falling. Delaying new aircraft orders might be a good response to such a scenario.

But when the challenge is a sustained jump in fuel prices due to supply reductions like now, access to more fuel efficient aircraft is of crucial strategic importance to competitiveness. Early retirement of older aircraft will therefore be the dominant mechanism used by airlines to adjust capacity in this scenario, especially where entire fleet types can be removed, unlocking significant cost saving opportunities. Airlines did a lot of that kind of clean-up work during COVID, but six years on I’m sure there will be some new sub-fleets whose time has finally come to face the axe.

One thing I don’t see at the moment is a demand risk to Boeing and Airbus, although there may be issues on the supply side that I’m not aware of. If financially weak airlines are forced to defer their aircraft orders, I would imagine that those positions will be snapped up by stronger carriers.

Final thoughts

The thing that airlines will be most keen to see is some stability. They know how to replan and reoptimise around a different fuel price level and whilst some of the weakest airlines won’t come out the other side of that adjustment process, the industry will find ways to pass on the cost increase to customers over time. The industry might be a little smaller than it would have been, but the best run and most financially robust airlines will probably be in an even stronger relative position.

The biggest difficulty I think is dealing with the profound uncertainty. If airlines assume prices will come down again later in the year and then they don’t, the window of time to make the necessary changes that they have thanks to their fuel hedging programmes will have been wasted. On the other hand, if they move quickly to cut capacity and then prices come down again, they might lose out to competitors who take a more aggressive approach. Finding ways to retain some flexibility to respond at short notice will be a key differentiator.

Of course there will be airlines who don’t have the cash resources either to ride things out or to restructure their business to adjust. They will be the casualties. It is no surprise that airline management teams are once again emphasising their cash and liquidity numbers in their messages to investors. The airlines with the most financial firepower are likely to be the ones that come through this latest financial shock as the winners.