Assessing the hit to airline valuations from the Iran war

The fog of war

Airline valuations have taken a sizeable hit due to the war in Iran. That’s understandable of course. Jet fuel prices have doubled and airline revenues are sensitive to the state of the world economy. At times like this, investors tend to sell first and ask questions later.

Whilst short-term share price movements will be driven by automated trading algorithms and sentiment, at some point analysts will return to looking at the fundamentals. Whilst the fog of war is still thick, I thought I’d take a first look at whether the valuation moves we’ve seen make any sense.

Who has been hit the worst?

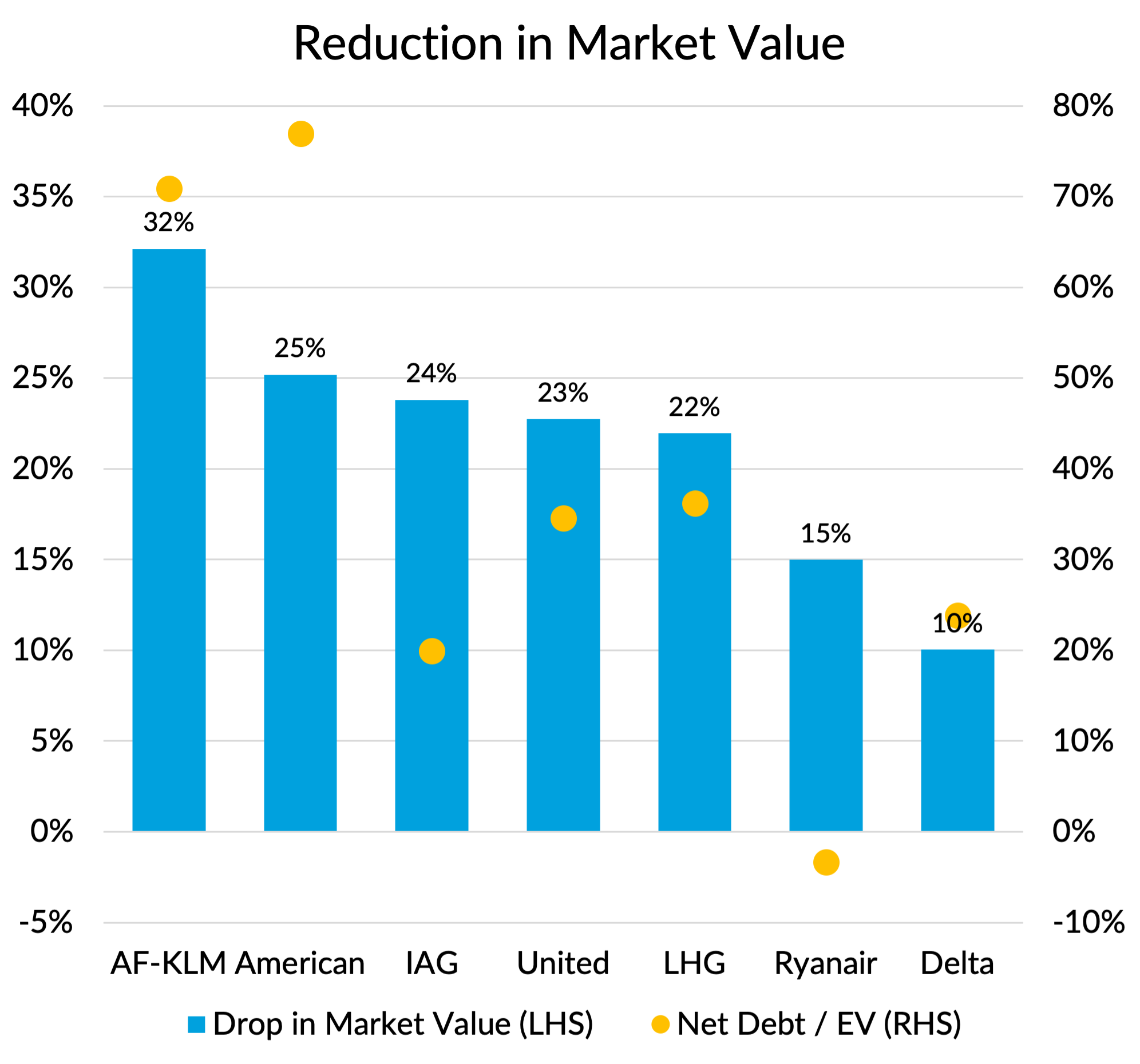

I’m going to look at the change in valuations since the 26th February. Note that I did all this analysis based on the closing share prices on Friday. As I finalise this article on Monday, airline share prices are currently trading up about 4%.

For my airline sample, I’ve included the three big Western European airline groups, the three big US network airlines, plus Ryanair as benchmark to represent the low cost carrier segment. it would have been interested to include the Gulf carriers of course, but they are not listed entities.

You would expect the most highly indebted companies to have been hit worst. For any given % reduction in operating cashflows, the impact on equity value will be amplified by higher leverage. I’ve chosen net debt as a percentage of the pre-war enterprise value (market cap + debt) as my measure of leverage. The blue bars in the chart below show the change in market capitalisation, and the leverage figures are shown as gold circles.

The two most highly geared airlines, AF-KLM and American Airlines, have indeed seen the biggest valuation hit at 32% and 25% respectively. Two of the least leveraged companies, Ryanair and Delta have seen the smallest hit. So that does seem to have been a factor, although IAG is also relatively low on my leverage score and was the third worst affected.

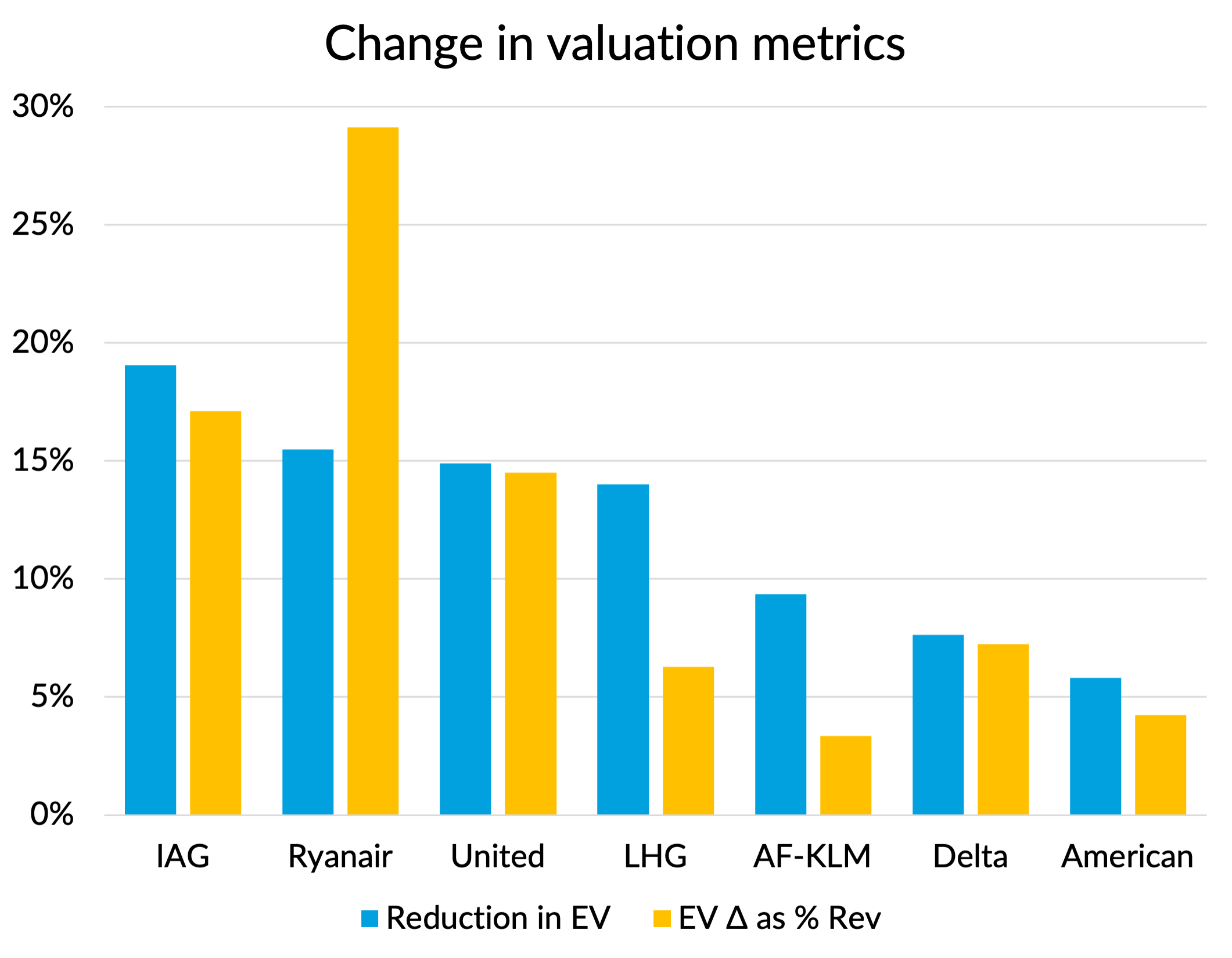

One way to try to eliminate the effect of leverage is to look at the change in enterprise value (EV). That’s the market capitalisation plus the net debt. All other things being equal, you might expect to see a consistent drop. There is also an argument that the expected reduction in future cashflows and hence EV should be proportional to the revenue base. So the reduction in value as a percentage of revenue might also be expected to be quite consistent.

I’ve shown both these metrics on the following chart. My take on what this shows is that IAG, Ryanair and United seem to have seen their valuations hit harder than you might expect, relative to AF-KLM, Delta and American.

Fuel impacts

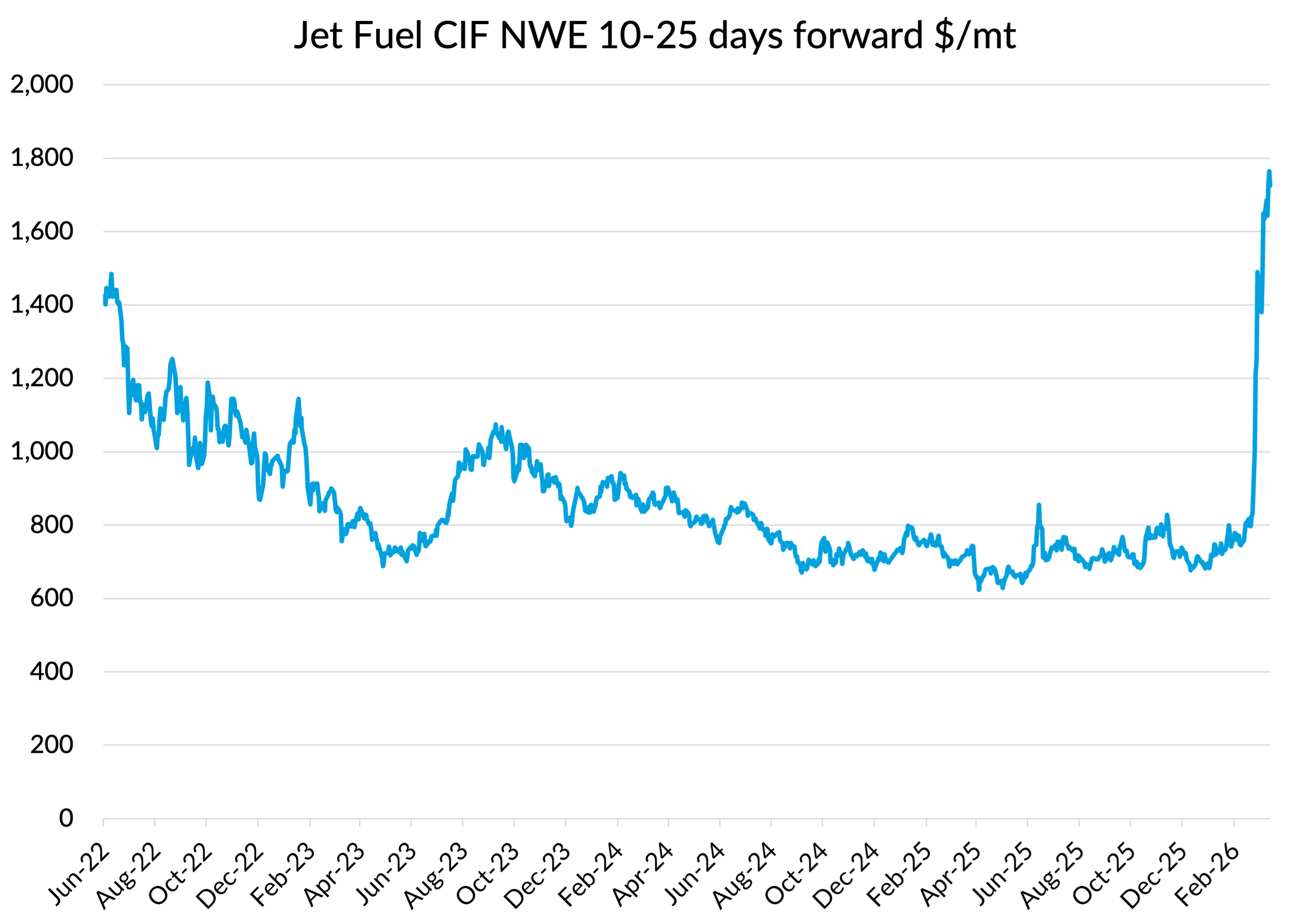

It is time to dig into the specifics of the fuel price impacts and the impact of airline fuel hedging. Jet fuel prices have more than doubled since before the war. The following chart shows the price of jet fuel in North Western Europe for delivery in the next 10-25 days.

Crude oil prices haven’t increased by anywhere near that much, going from about $72/bbl before the war to $112/bbl today, an increase of about 55%. That means that the “crack spread” between the price of jet fuel and crude oil has exploded from about $23/bbl in 2025 to something like $107/bbl today for jet fuel deliveries in North Western Europe.

About 65% of the jet fuel price increase since the 26th February is accounted for by the widening of the crack spread, and only 35% by the rise in the price of crude. Another way of saying that is that airlines that hedge their fuel exposure using financial derivatives linked to the price of crude are only protected against 35% of the price increase.

Another popular price to use for hedging is the gasoil price. That’s more closely related to the price of jet fuel than crude is, but spreads on diesel have only widened by about half the jet fuel spread. So even using gasoil futures will only have provided about 67% protection in current market conditions.

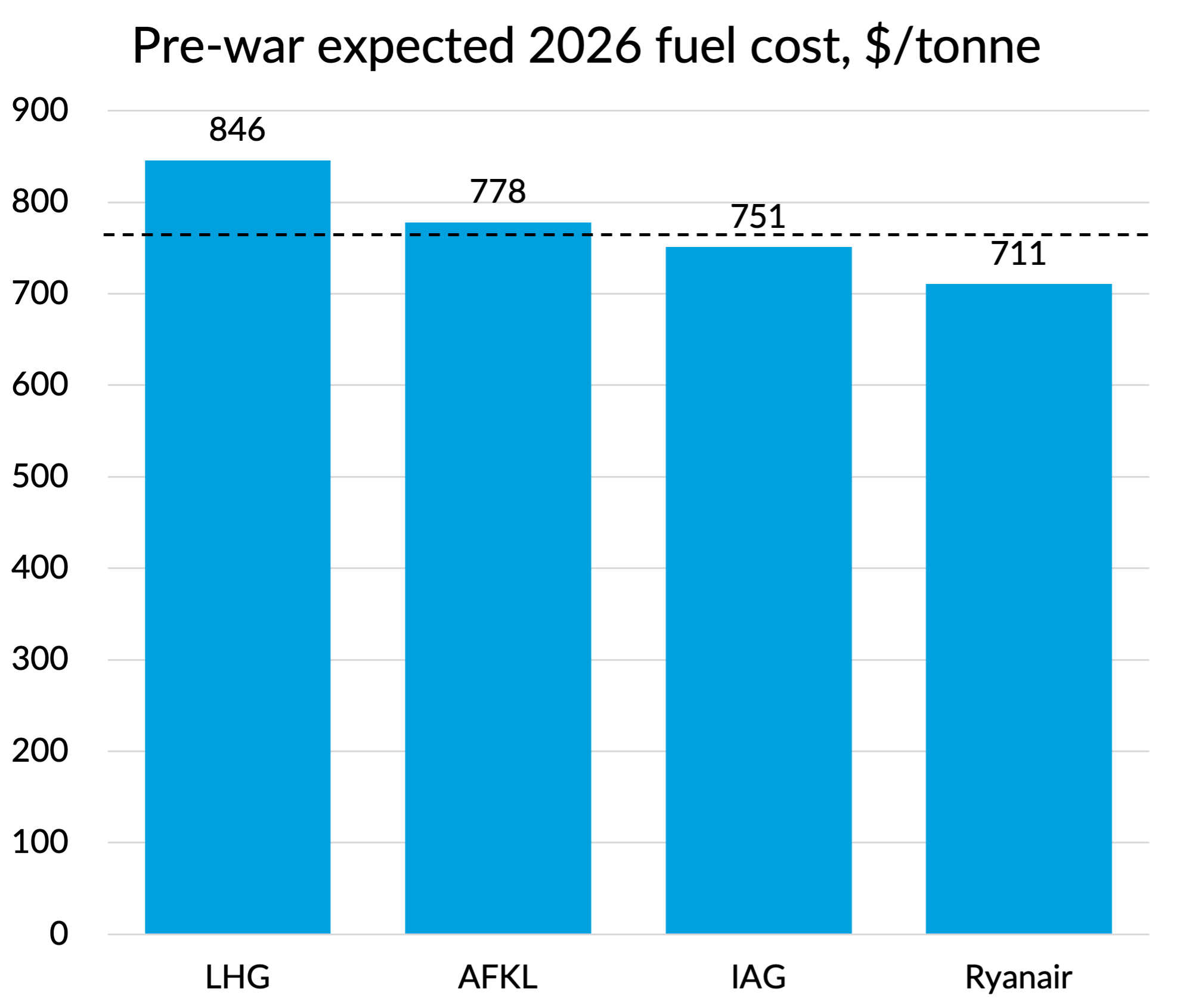

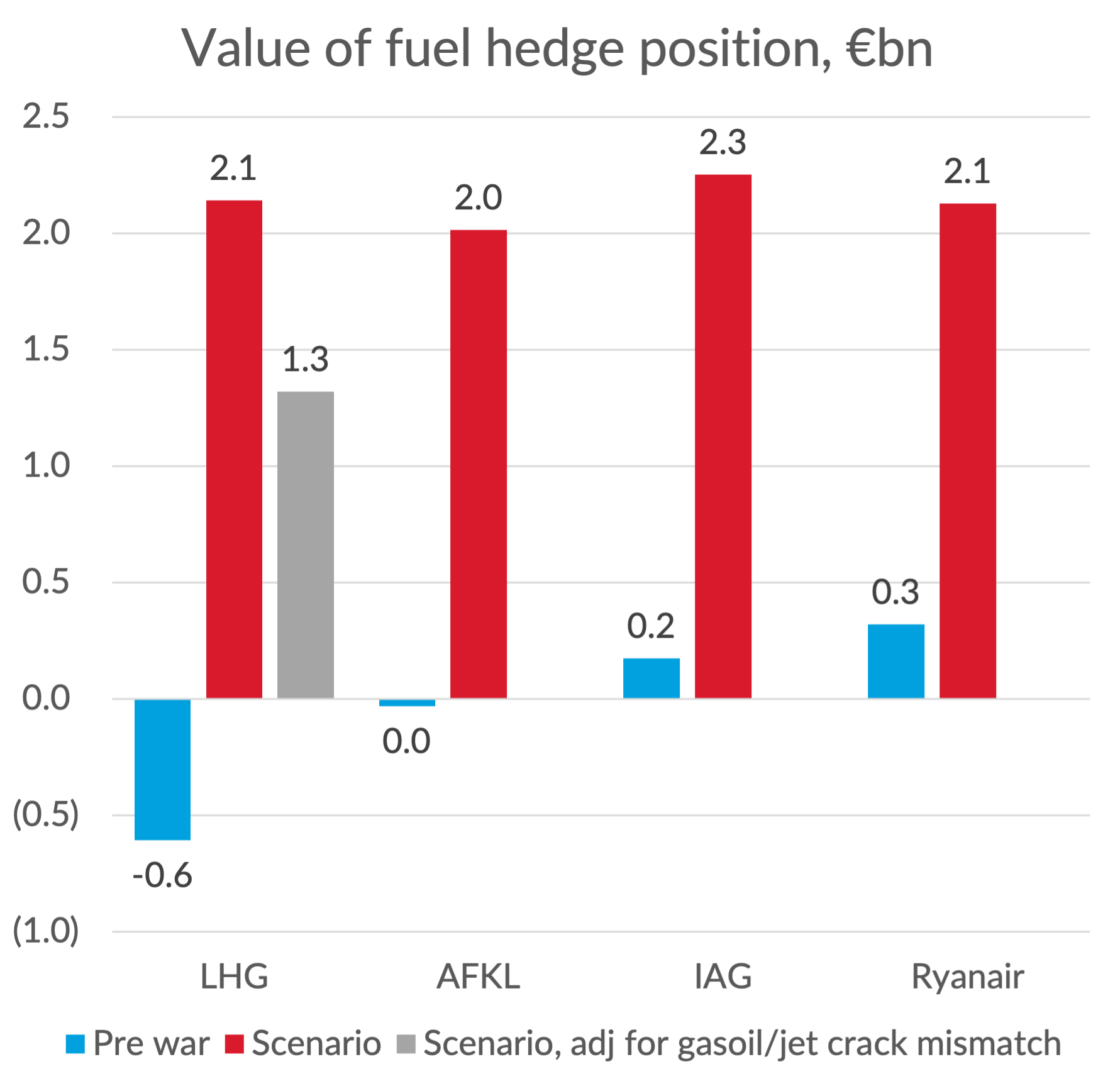

I’ve had a go at calculating the value of the hedge positions of the European airlines. The first thing to say is that the airlines were in different positions before the war. Ryanair was the most heavily hedged, with 81% of its calendar 2026 fuel costs hedged. Lufthansa was next, with 77% covered. IAG and Air France - KLM were slightly behind, at 61%. But that doesn’t tell the whole story. They were hedged at different prices. Using the pre-war forward price curve for the unhedged element of their fuel costs, their expected fuel costs for 2026 were quite different, as you can see from the following chart. The dotted line shows what an unhedged airline would have been expecting. IAG and Ryanair were “in the money”, whilst Lufthansa was quite heavily underwater.

Despite the worse pricing of their fuel hedges, perhaps Lufthansa’s higher level of hedging compared to IAG and AF-KLM would stand them in good stead now, given what has happened to fuel prices?

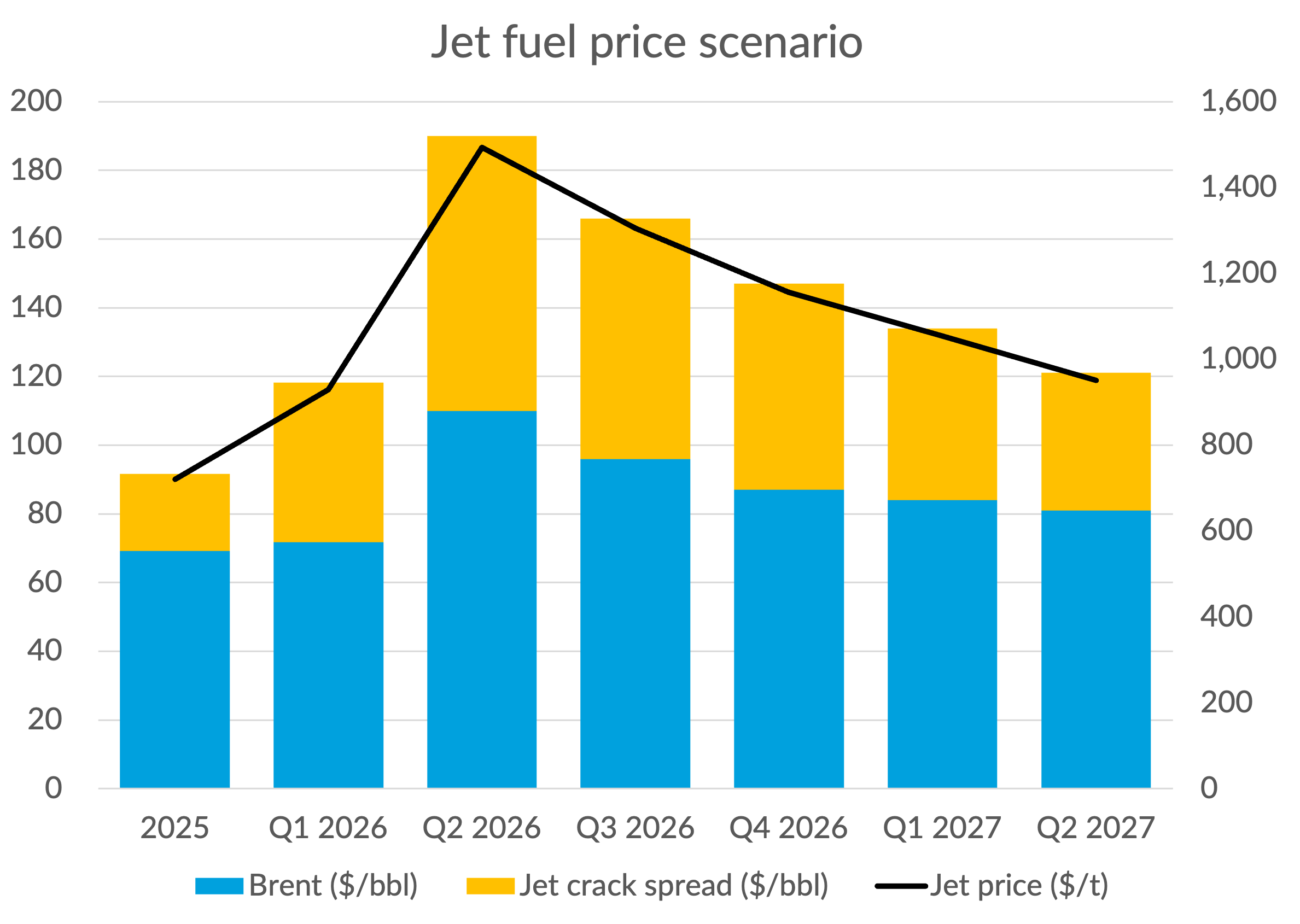

To evaluate that, we need a scenario for future oil and fuel prices in the rest of 2026. The following chart shows the one I’m going to use. It is based on current future prices for Brent and my own assumptions for what happens to the crack spread. I’ve assumed it falls back from $107/bbl today to $80 in Q2, $70 in Q3 and $60 in Q4. That compares to $23 in 2025, so it assumes that the current “distress” in refined products persists for some time, albeit improving slowly. In total, that means jet fuel prices fall from current inflated levels back to below $1,200 per tonne by the end of the year and around $1,000 by the middle of 2027.

Using those assumptions, I’ve calculated the value of the current fuel hedge position for each of the four European carriers, as it relates to fuel use in 2026. Some carriers do have positions extending into 2027, but the disclosures on those are a bit patchy so I’ve not included them. That will understate the total value of their hedge positions a bit.

For IAG, AF-KLM and Ryanair I’ve assumed that their fuel hedges are fully effective. I don’t know for sure that this is the case. To the extent that they’ve used financial instruments that don’t fully capture the rise in jet fuel prices, I may have overestimated the value.

For Lufthansa, we do know that they don’t hedge jet fuel directly. Their 77% hedge for 2026 is based on a 45% hedge on gasoil prices and a 32% hedge on Brent. I’ve shown two figures in the chart below. The first assumes that the gasoil price fully captures the jet fuel exposure. The second assume that it only captures half of the increase in the jet crack spread, which I think is about what we are seeing currently.

Lufthansa’s management has been pitching to the market that they are better placed for 2026 when it comes to hedging than AF-KLM and IAG. I don’t think that bears scrutiny. Their pre-war hedging was underwater and the instruments they used to hedge their exposure weren’t well suited to a supply dislocation like the one we are seeing. Perhaps we will see that the other three also have mismatches in their hedging positions, which reduce the gap. We’ll find out more at the next quarterly updates, I guess.

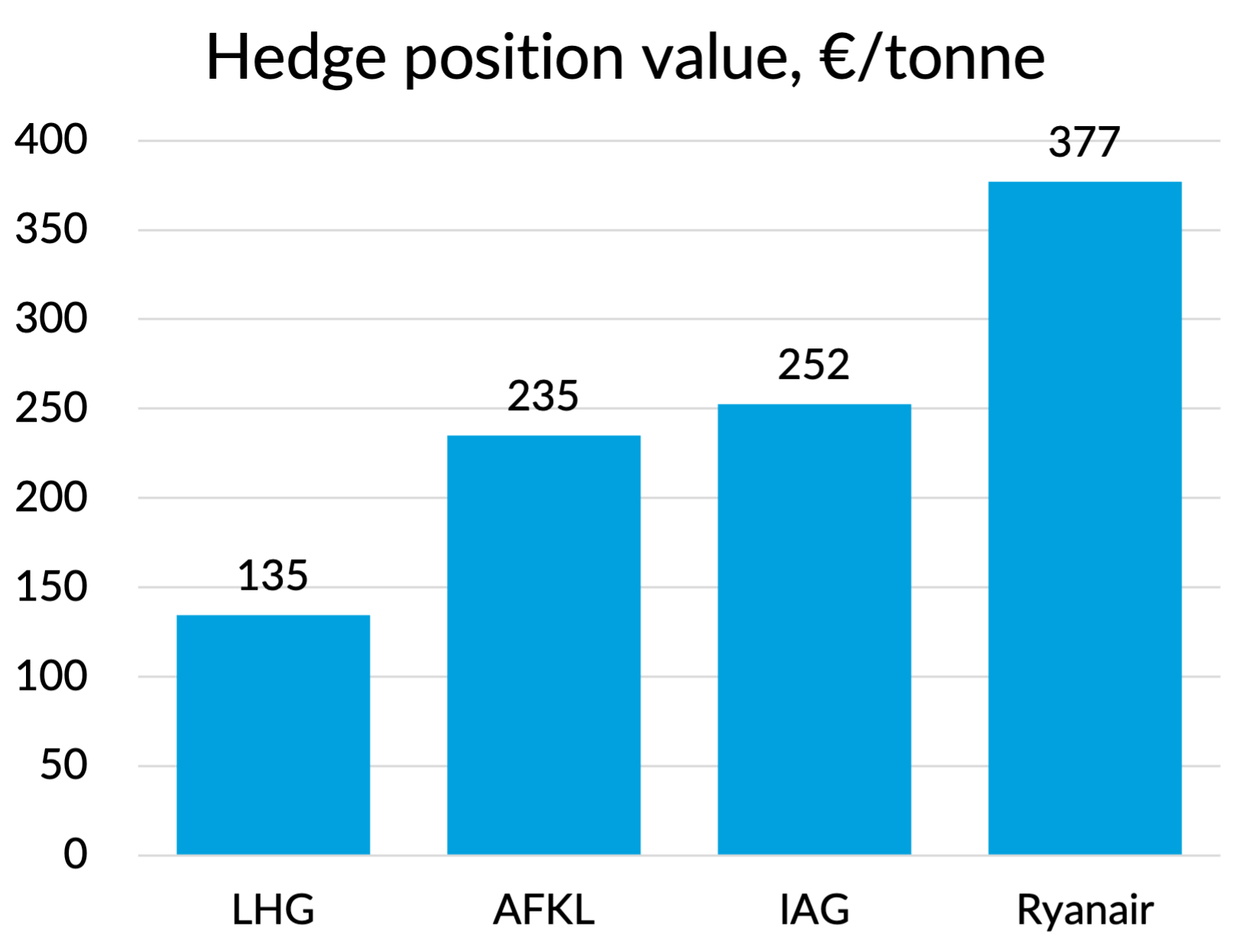

It is also the case that Lufthansa uses more fuel than the other three (~14% more than AF-KLM and 10% more than IAG), so on a per tonne basis their hedge position looks even a bit worse. Ryanair’s fuel use is about 37% below IAG, so they look even better on this basis.

Source: GridPoint analysis

What about the US majors?

The US majors have made a point in recent years of not hedging their fuel costs. The logic is that averaged over the long-term, hedging costs money. They also argue that hedging just makes airlines delay putting up prices when fuel costs go up, which is unhelpful for industry profitability.

I have some sympathy with those arguments, but I think they are overstated. There are definitely transaction costs associated with hedging - the bankers need to pay for their mansions somehow, don’t they? But those are pretty small in the scheme of things. The bigger question is whether buying forward should be structurally more expensive than buying spot. That’s a question of the balance in the market of people wanting to sell forward (producers) versus those buying forward (consumers). I’m not an expert by any means, but there is an argument that the you might even save money on average buying forward. And of course there is some value in reducing risk and volatility.

I agree that the correct industry response to higher input costs is to raise prices. But you can’t raise prices on tickets you’ve already sold. In the US domestic market, tickets might be sold quite close to departure, but for long-haul travel seats are sold well in advance. It makes sense to me to fix the fuel price for seats when you sell them. So for long-haul carriers, having a high percentage of your fuel costs covered for the next 3-6 months makes perfect sense to me.

In any event, the US carriers don’t hedge their fuel costs, so they are facing the full impact of the current fuel price spike. There is one partial exception, which is Delta. A few years ago, they bought a refinery to protect themselves against increases in the jet fuel crack spread. That decision will be paying dividends in the current market. How big a mitigation could that be?

Delta’s refinery processes 200,000 barrels of crude per day. In terms of the total amount of refined products, that is equivalent to about 75% of Delta’s usage. So given that 65% of the fuel price increase can be attributed to the widening of the crack spread, on the face of it that should be a really strong hedge. Unfortunately for Delta, it won’t be quite that good. They might be able to ramp up the jet fuel mix to about 30% of the total, with gasoline dominating the residual. Spreads on gasoline have increased, but by nothing like what has been seen in the jet fuel market. Nevertheless, that might give them something like a $1.5 billion reduction in their net 2026 fuel bill under my fuel price scenario, or about $115 per tonne. Not to be sneezed at, but still at the low end of what the European airlines will gain from their fuel hedges.

The strategic implications of different hedging positions

Having an “in the money” fuel hedging position is of obvious financial value, but does it have strategic value too? Many people in the industry believe so, but I think the logic they often apply is flawed. Let me explain.

Airlines talk about their hedging position in percentage terms (“we are 80% hedged for Q2”) and cite the blended fuel price (“at current forward rates, our average fuel cost will be $850 per tonne”). But the truth is that hedging contracts are for fixed volumes of fuel. So if an airline with 80% of its planned volumes hedged cuts capacity by 20%, it will become 100% hedged and the average fuel cost will go down to the level of your hedging contract. Put another way, any management decision that you can take that changes your fuel use will do so at the current marginal fuel price. Your hedging position is irrelevant. Some airline management teams get this wrong of course and use the blended fuel cost in their spreadsheets and models. But the sophisticated ones will get it right. Certainly when I was running Network Planning at British Airways, I made sure we always used the spot or forward rate when making capacity decisions.

People also often argue that an airline which is well hedged will be under less financial pressure to increase prices or cut capacity. That’s true I suppose, but only in the same way that an airline with higher cash reserves will be under less immediate financial pressure. The short-term economics of raising prices and cutting capacity will be the same, regardless of the hedging position. The strategic value of pursuing market share instead is also unaffected. The only difference is that a well hedged airline has a stronger balance sheet, which might increase their flexibility to pursue strategies which are suboptimal in the short-term, but have long-term strategic benefits, such as pursuing market share gains.

The Ryanair case study

Of all the airlines, Ryanair’s short-term incentive to adjust capacity in response to higher fuel costs is probably the strongest. They have a very variable cost base and fuel makes up a much higher percentage of their costs than the network carriers. The percentage increase in fares they require to pass on any given increase in fuel costs is therefore greater. Coupled with the fact that their customer base is very price sensitive, their ability to offset fuel cost increases through price is lower. As I argued in the last section, this short-term financial incentive is unaffected by their actual hedging position.

As a short-haul carrier, Ryanair also doesn’t sell very far in advance. So you would think there would be no need to buy fuel forward for that reason either. But in fact Ryanair has always hedged very heavily compared to other airlines. I think the reason for this is that going for market share during downturns is a core and recurring strategy for Ryanair. Hitting the competitors when they are weakest and growing when airports and other suppliers are desperate for volume is a strategy that has worked well for Ryanair over the years.

With one of the strongest balance sheets in the business, I would argue that Ryanair doesn’t need the extra boost to their financial firepower that comes from being well hedged when fuel prices go up. But an extra €2 billion in the bank undoubtedly helps in keeping nervous shareholders onside and reinforces the message to competitors that Ryanair won’t back down when it comes to a market share battle. The drag on profits when fuel prices fall is not a material strategic issue for an airline like Ryanair with industry leading unit costs and margins.

Back to valuations

Freshly armed with our calculations of the financial value of the fuel hedging positions, we can have another look at the change in company valuations.

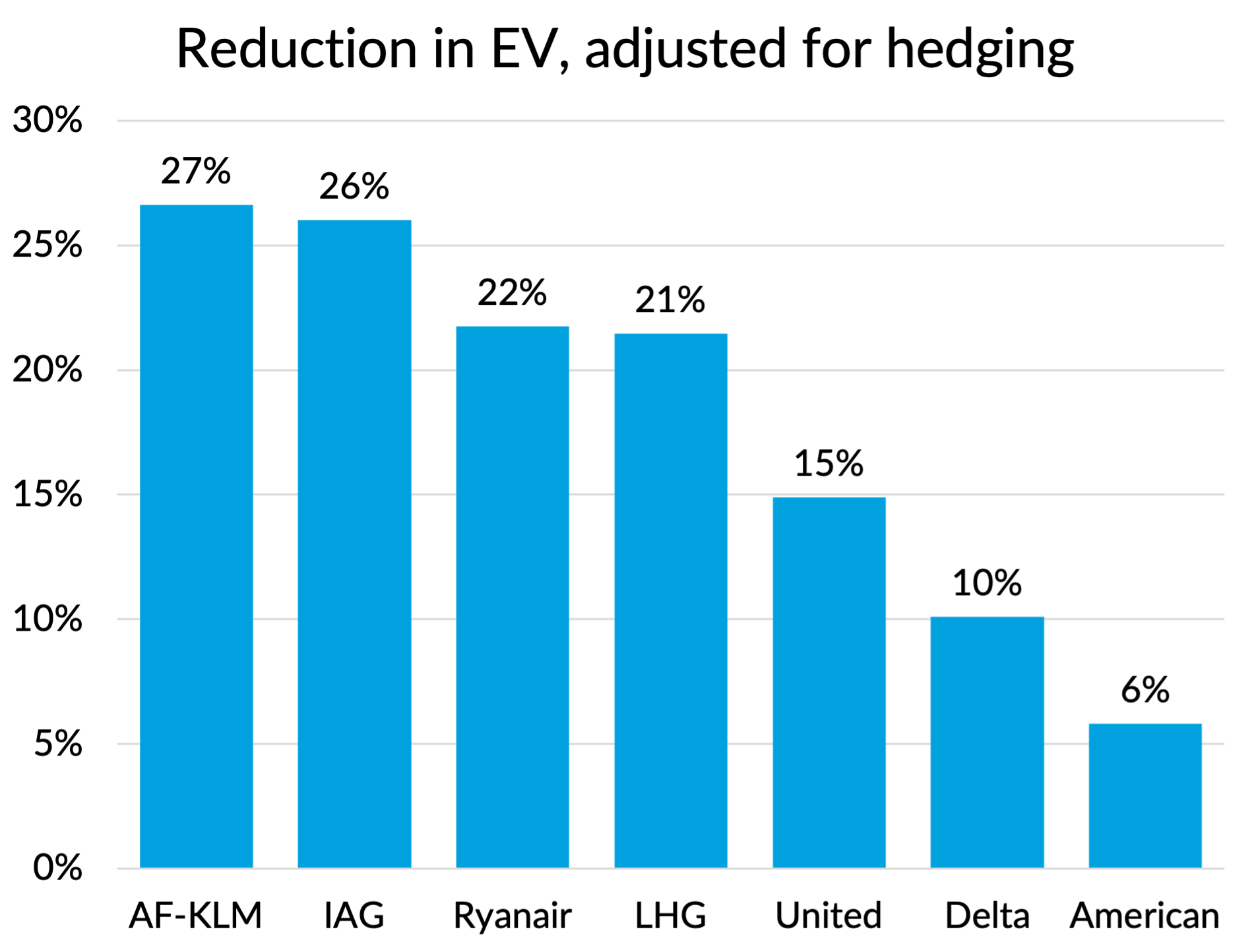

In the chart below, I showed the change in Enterprise Value due to the war, but I’ve adjusted the current value to exclude the change in the value of the hedging position. So American's and United’s drop is as we calculated before, but I’ve increased the value drop for those airlines that have seen a jump in the value of their hedging positions. If you believe the market is efficient, this is an estimate of how much value has been lost, excluding the hedging position gain.

Source: GridPoint analysis

Air France - KLM now jumps to the top of the “biggest losers” pile. The gain in the value of its hedging position was particularly large relative to its Enterprise Value. So if that is excluded, the drop in the value of the rest of the business looks much bigger.

On this revised metric, there looks to be a bit more consistency between the valuation hits, at least within region. However it exacerbates the difference between the hit on European airline valuations and what has happened to the unhedged US carriers.

To be honest, I find that puzzling. Yes, the European airlines have more direct exposure to the Middle East, but it is being more than offset by the benefit they are seeing from the disruption to the operations of their Gulf competitors. Demand shifts may also favour European airlines. European tourists going to the Middle East, primarily on Gulf carriers, may in future go to European destinations or fly West on European airlines.

There is probably an effect of European jet fuel supplies being more impacted than in the USA. I guess analysts also have more faith in the ability of the US carriers to pass on their fuel cost increases to customers in the more concentrated US market. I’m not sure I agree with that, but I’m sure that’s what the US airlines are saying to the analysts.

Does a 20-25% drop in Enterprise Value pass the common sense test?

In theory, Enterprise Value should be related to the discounted value of future pre-financing cashflows. Let’s do some fag packet analysis on the IAG numbers as an exercise. IAG had a pre-financing cashflow in 2025 of €4 billion, so a 25% hit to Enterprise Values suggests a long term hit to cashflows of about €1 billion a year, equivalent to a drop in operating margins of about 4 percentage points. That’s not outlandish if you consider that fuel costs make up 21% of revenue, so a doubling of fuel prices would hit margins by 21 points. Of course, if a fuel price increase of that magnitude is sustained, it will be passed on in higher prices. If you assume that 80% of the hit can by passed on to customers over time or be offset by other cost savings, that will put you in the right ball-park to explain the hit to 25% hit to valuations.

However, this logic should suggest that higher margin players should see their valuations impacted by less. A four point hit to margins for a 15% margin airline like IAG is a 26% reduction. A four point hit to airlines making only 5-6% like AF-KLM and Lufthansa Group is a 70-80% reduction in operating profits and cashflows. Yet as we just saw, all three have seen their Enterprise Values impacted by very similar percentages.

This is not financial advice

None of the above should be taken as financial advice. As you can see, I am often puzzled by the way the stock markets behave in the short-term. For what it is worth, in relative terms I would view the valuation hits to IAG and Ryanair as being overdone, with American and Delta perhaps looking vulnerable to more falls.

Having said that, the bigger question for the trajectory of airline share prices is what happens in the Gulf over the next few weeks. The duration of the war and the lasting impacts on oil and refinery infrastructure are key here.

Whatever happens, there will undoubtedly be more turbulence ahead for airlines and the world economy. Time to check your seat belts are securely fastened.