Dissecting Virgin Atlantic’s 2025 Results

Profitability trends

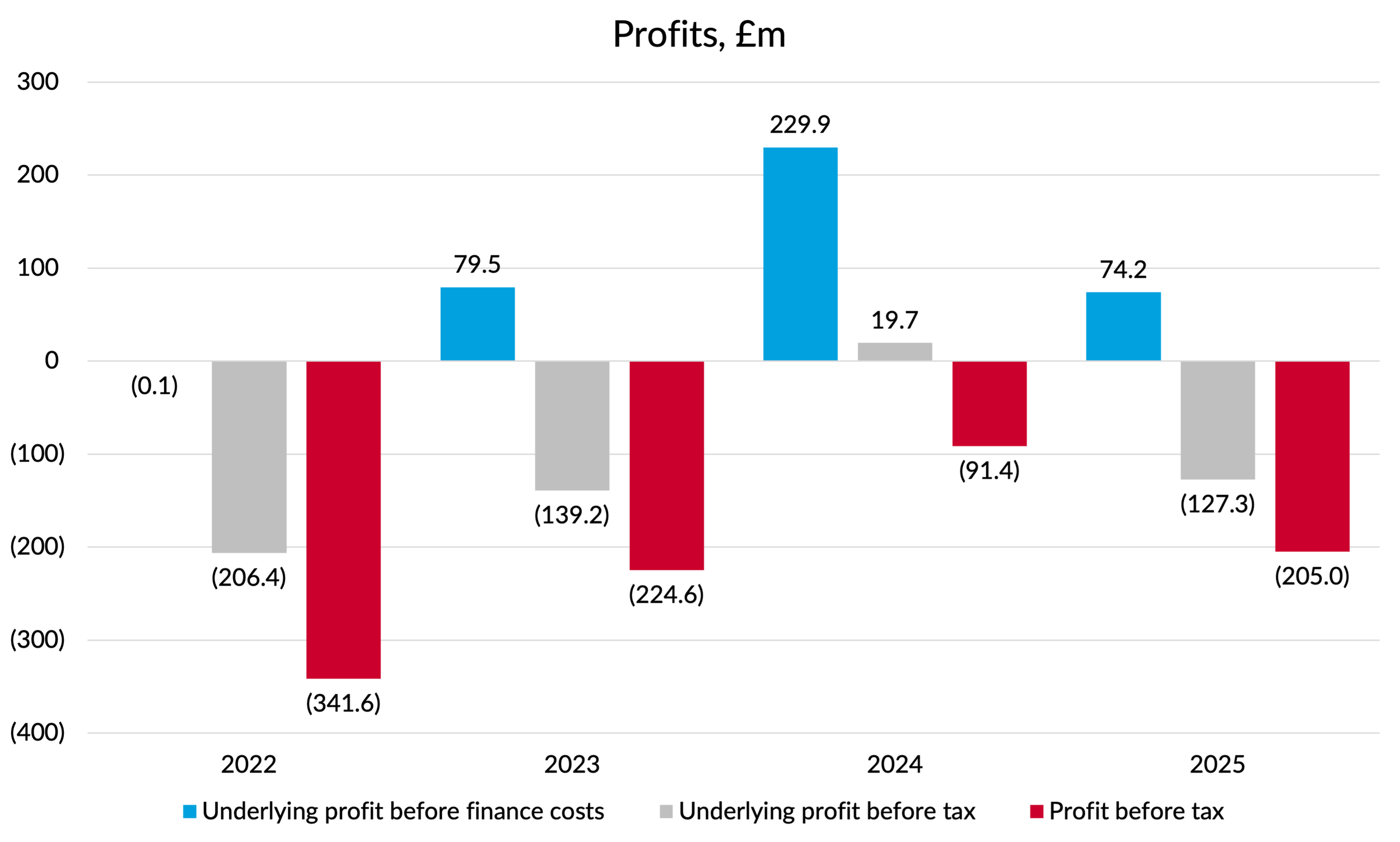

We are a bit spoilt for choice when it comes to choosing a profit measure for assessing Virgin’s 2025 results.

The statutory results for 2025 showed an operating profit of £123.4m and a loss before tax of £205m. That pre-tax loss was more than double the loss they made in 2024.

However, Virgin likes to focus on a measure of “underlying” profits, which excludes large one-off items, unrealised gains/losses on derivative contracts, and treats their interest-free shareholder loans as zero cost (the accountants invent a notional interest cost in the statutory accounts). On that alternative profit measure, Virgin celebrated what I think was their first ever year of pre-tax profitability, with an underlying pre-tax result of £19.7m. Normal service was resumed in 2025 though, with the company slipping back into a £127.3m loss. Underlying operating profits of £74.2m represent a meagre 2% margin.

I don’t think Virgin Atlantic has ever managed to record a net profit on a statutory basis. Even on an underlying basis, they barely broke even last year. 2025 was a good year for their biggest rival, British Airways, who grew operating profits by 8% compared to 2024 and recorded a record operating margin of 15%.

With that context, you might have thought that Virgin’s management would see a 32% reduction in operating profits and a swing back into losses as representing something of a crisis, especially given recent events in the Middle East. Whilst that happened after the end of the year, it was known before they published their annual report and the Iran war is referenced in the Chairman’s statement. However, the tone of their Annual Report remains relentlessly upbeat. Here is what the CFO had to say about the results:

“Whilst it is disappointing to report a loss following our return to profitability in 2024, we are proud to have grown our load factors and increased our capacity despite significant spare aircraft engine availability challenges.”

As we will see in a minute, the decline in profitability came mainly from a 10% jump in non-fuel costs, and yet the CFO had this to say:

“Cost control continues [to] underpin our overall financial performance - since the Pandemic we have kept increases in overhead and operating costs below UK inflation. In 2025, our NFCASK increased by 9% vs 2024 predominantly driven by inflationary increases in labour costs as well as the one-off costs within engineering and continued investment in technology. We remain focused on controlling the controllables.”

I can understand that outgoing CEO Shai Weiss would want to celebrate the positives of his final year in command, after a difficult seven years dealing with the pandemic and the aftermath. I guess you have to admire the company’s ability to put a positive spin on what I would regard as a pretty bad set of results. In his “incoming CEO’s statement”, Corneel Koster acknowledges the need to improve the financial performance, although a sense of urgency still seems to be somewhat lacking to me:

“The foundations we stand on today are strong because of the discipline, resilience and belief shown across the organisation. Together, we will build on them and we will improve financial returns working as one team to be the most loved travel company, and to fly with a level of performance that gives us real freedom for the future”

Revenue results

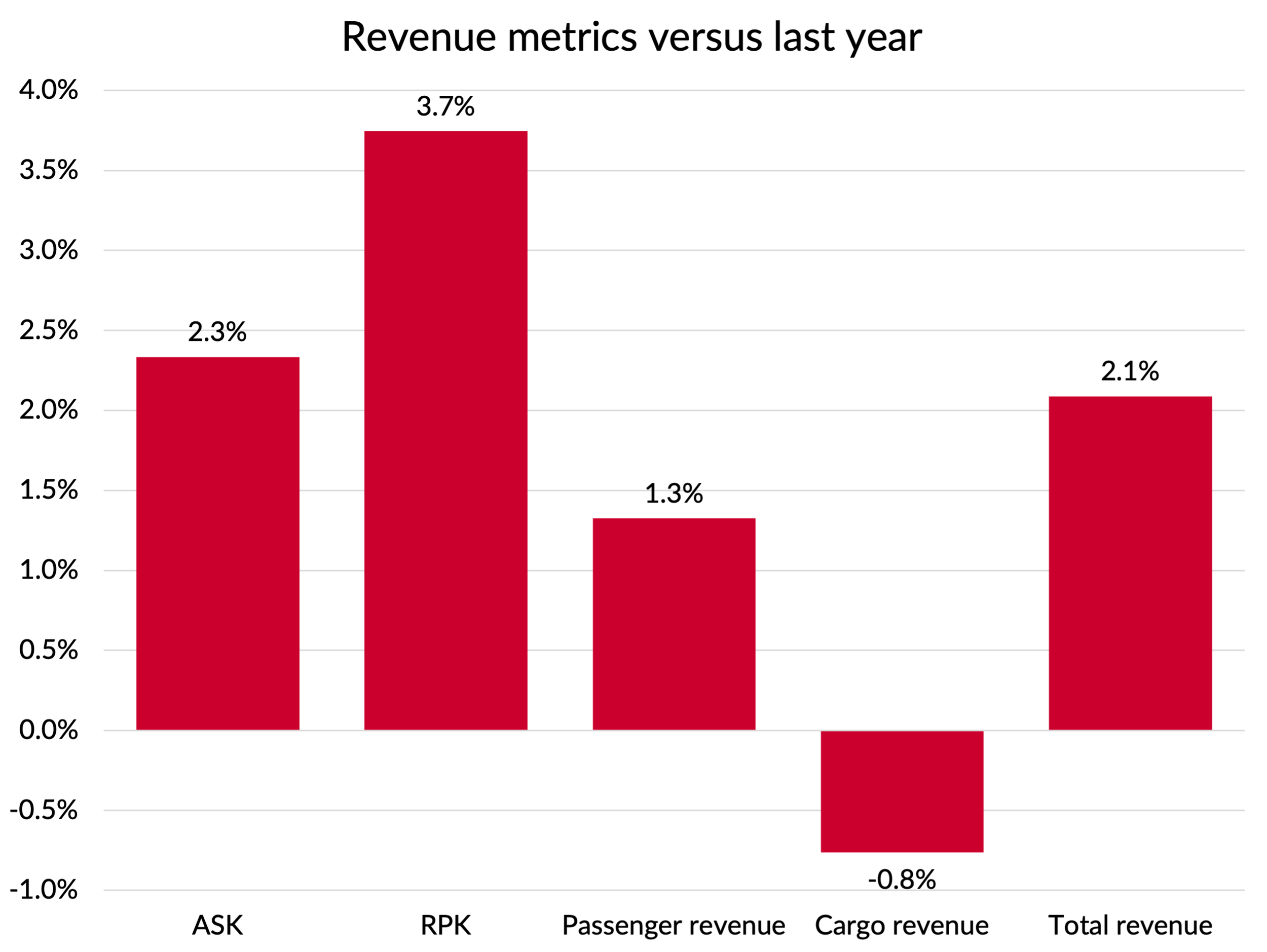

The revenue performance compared to last year was a bit patchy. Capacity grew by 2.3% in terms of ASKs and load factors improved by almost 2 percentage points to 79.2%. That’s still slightly below the 81.1% level they achieved back in 2019 and quite a bit worse than BA’s 83.8%, but it’s an improvement nonetheless. The areas of weakness were passenger yield (down by 3%) and cargo volumes (down by 1%). Other revenues did better and brought the overall revenue growth up to around 2%, leaving RASK essentially flat.

Fuel costs

Fuel costs were down 5% despite the increase in capacity. Fuel volumes were up 1%, slightly less than capacity, with fuel prices dropping by 6%. The average price paid of £639 per tonne was about 1% higher than what British Airways paid during the same period, so that had little to do with the divergence in relative profitability.

Employee cost increases

Employee costs increased by an eye-catching 12.7%. 5.3% of that came from increased employee numbers, which implies a productivity drop of around 3%. Wages and salaries per head went up 5.5%, about 2% higher than inflation. Pension costs rose even faster and social security cost per head jumped by over 17%, thanks I assume to the Rachel Reeves national insurance raid. Not a pretty picture.

Within the overall employee cost numbers, one thing that stuck out to me was the jump in payments to the four executive directors. In total, they almost tripled compared to last year, with the highest paid director’s total pay more than tripling to £6.9m. I guess that’s one reason why Shai was in such a positive mood about the year.

Airline direct operating costs

Another cost line which saw a startling increase compared to last year was “airline direct operating costs”, which grew by 17.5%. At £726.8m, this is Virgin’s largest cost category after fuel so that cost increase was worth a cool £108m.

It is not entirely clear what is included here, although we know that it doesn’t include aircraft maintenance or ownership costs, employee costs or marketing and distribution costs, all of which are separately reported. There is another category of “other operating and overhead costs”, so I assume this cost line is only used for variable costs like landing fees, overflying charges, third party handling and catering costs.

I’m at a bit of a loss to explain what is going on here. It seems quite an extraordinary increase and as far as I can find the only explanation given is “inflationary pressures”.

Sustainability targets

In 2021, Virgin set a target for 2026 to reduce carbon emissions intensity by 15% compared to 2019, as measured by CO2 equivalent tonnes per Revenue Tonne Kilometre (RTK). That would require a figure of 0.615 t/RTK to be achieved next year. By 2025, they had achieved only a 9% reduction in six years, requiring another 6% in one year. They said that they expected to achieve only another 2% in 2026, leaving them about 4.5% over their target.

The explanation for the shortfall to the target set out in the Annual Report was all about the failure of Sustainable Aviation Fuel (SAF) to develop as quickly as expected. Whilst that is true, I don’t find this very convincing as an explanation. In 2025, Virgin used only 11,688 tonnes of SAF, representing 1.0% of their total fuel use. With a SAF mandate of 2% for fuel uplifted in the UK, that means that Virgin only did the bare legal minimum on SAF. British Airways managed to find sufficient SAF to meet 4.5% of their worldwide needs in 2025, whilst slightly beating Virgin on overall fuel cost per tonne. If Virgin had matched that performance, their overall emissions would have been about 2.5% lower. I take two things from this. Firstly, as BA has demonstrated, it would have been possible to secure much higher SAF volumes at affordable prices if the company had been as active as BA has in working with SAF producers. Secondly, even if they had matched BA’s performance, they still would have missed their target. If a shortfall on SAF was the only reason they missed their target, they must have been expecting a usage rate of around 7%.

Perhaps they have fallen short on the fuel efficiency benefits of their new fleet? I’ve been looking at that issue recently, so let us dive into that.

Fuel efficiency trends since 2019

In my last post about the fuel efficiency of the world’s fleets, I noted that according to my calculations, Virgin had improved is fuel efficiency by 23% since 2019. The metric I used was “seat-block-hours per tonne”, using a standard “all economy” seat count for each aircraft type. I was therefore puzzled to see that when I calculated the improvement in what should be a highly correlated metric of “ASKs per tonne”, I only got a 12% improvement for Virgin between 2019 and 2025.

First of all, I got my pencil sharpener out and reviewed all my figures. My estimates for fuel burn were within 2.5% of the actual figures, but I replaced my estimated figures with the actual numbers. Next, I reviewed my “all economy” seat counts for the specific aircraft types Virgin have flown since 2019 and made some revisions (did you know that Wamos manage to cram 529 economy seats into a 747-400?). Together, those corrections slightly reduced the improvement to 19%, but we are still left with a 7 point gap to explain.

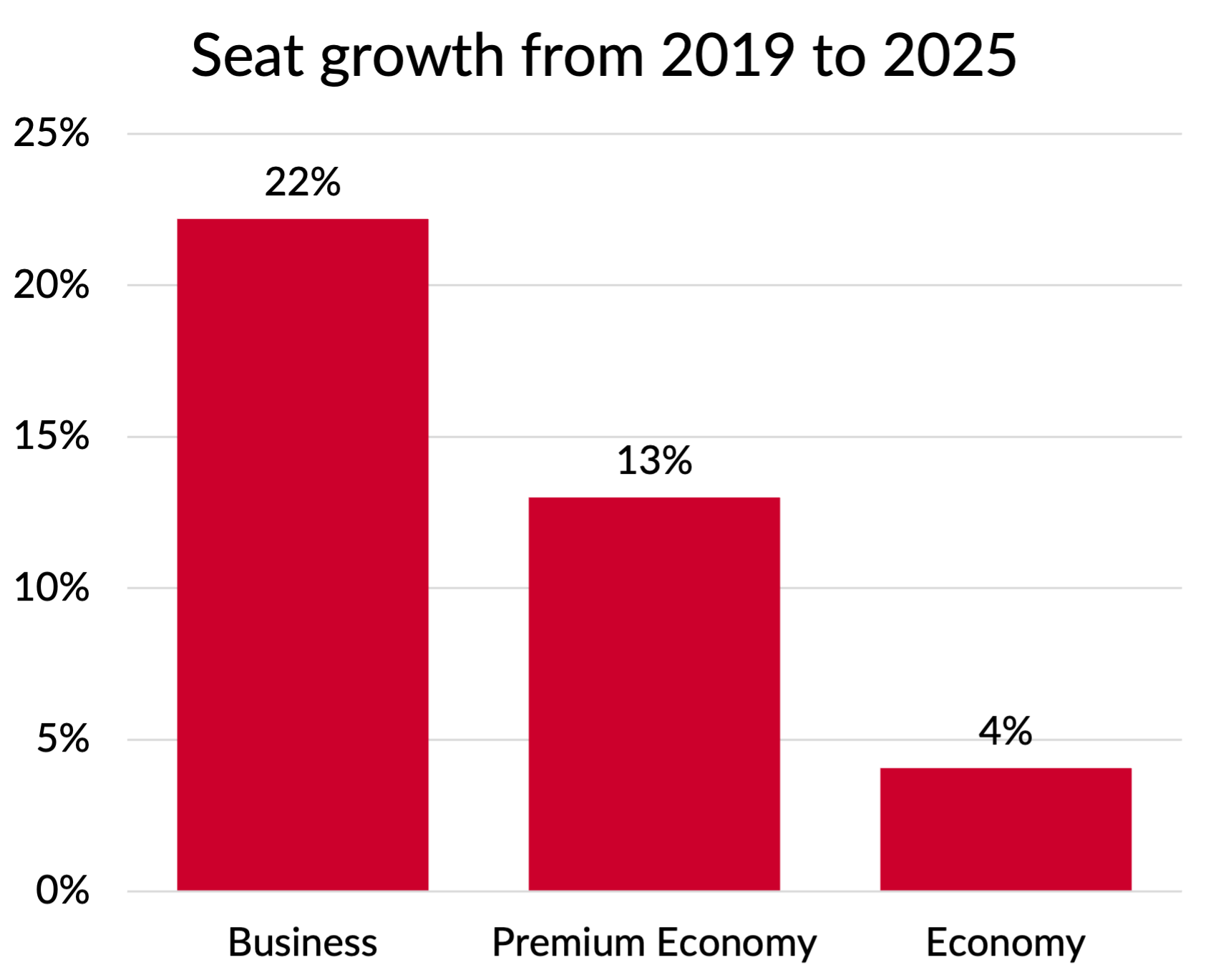

The first part of the explanation is that Virgin have reduced their average seating density since 2019. The actual number of seats has dropped from 67.5% of the “all economy” count in 2019 to only 65% in 2025. That was driven by business and premium economy class seat capacity growing faster than economy capacity (see next chart). That accounts for about 4 percentage points of the difference in the fuel efficiency metrics. I think the biggest thing driving that was the retirement of the high density 747-400s with only 14 business class seats that used to serve the Caribbean and Florida.

The remaining 3 points of missing fuel efficiency improvement is due to a drop in average speed, as measured by great circle distance flown per hour of scheduled block time. That’s equivalent to about an extra 15 minutes on a typical flight. A few things contribute to that. The 747-400 flew at mach 0.85 whilst the replacement Airbus wide-bodies fly at 0.82, a drop of 3.5%. When I measured fuel efficiency using a “per hour” metric, I didn’t take that effect into account. Secondly, Virgin has transferred all its Gatwick operations to Heathrow. The additional congestion has also likely contributed to longer block times. Finally, there will perhaps have been some contribution from flying longer routings due to the Ukraine war, although that’s probably not significant for Virgin as it doesn’t do much flying to Asia.

Coming back to Virgin’s missed sustainability targets, they work on a “per RTK” basis. RTKs per tonne of fuel used has only improved by 10% since 2019, even worse than the 11% we saw for ASKs per tonne. That’s been driven by reductions in both passenger and cargo load factors compared to 2019.

So to summarise, it looks to me like Virgin missed their targets for reductions in emissions intensity on their chosen metric because their load factors have worsened, they reduced the seat density of their aircraft, they consolidated their operations at Heathrow and they didn’t use as much SAF as they planned to because it was too expensive. With the possible exception of the load factor drop, those are all reasonable business decisions to have taken. But it is not as if their financial performance has been sparkling as a result.

Balance sheet stresses

If profitability has taken a turn for the worse, how does Virgin Atlantic’s perennially overstretched balance sheet look?

In his statement, the CFO celebrated the fact that £600m of the debt they took on during the pandemic had been repaid by the end of 2025 and that the remainder was expected to be repaid by the end of Q1 2026. But during the year they raised a new debt facility of $745m from Apollo, secured against their Heathrow slot portfolio (which works out at about $22.5m per daily pair in case you are interested). They’d only drawn $500m of it at the end of 2025, but presumably plan to use the rest to repay the balance of their pandemic era loans.

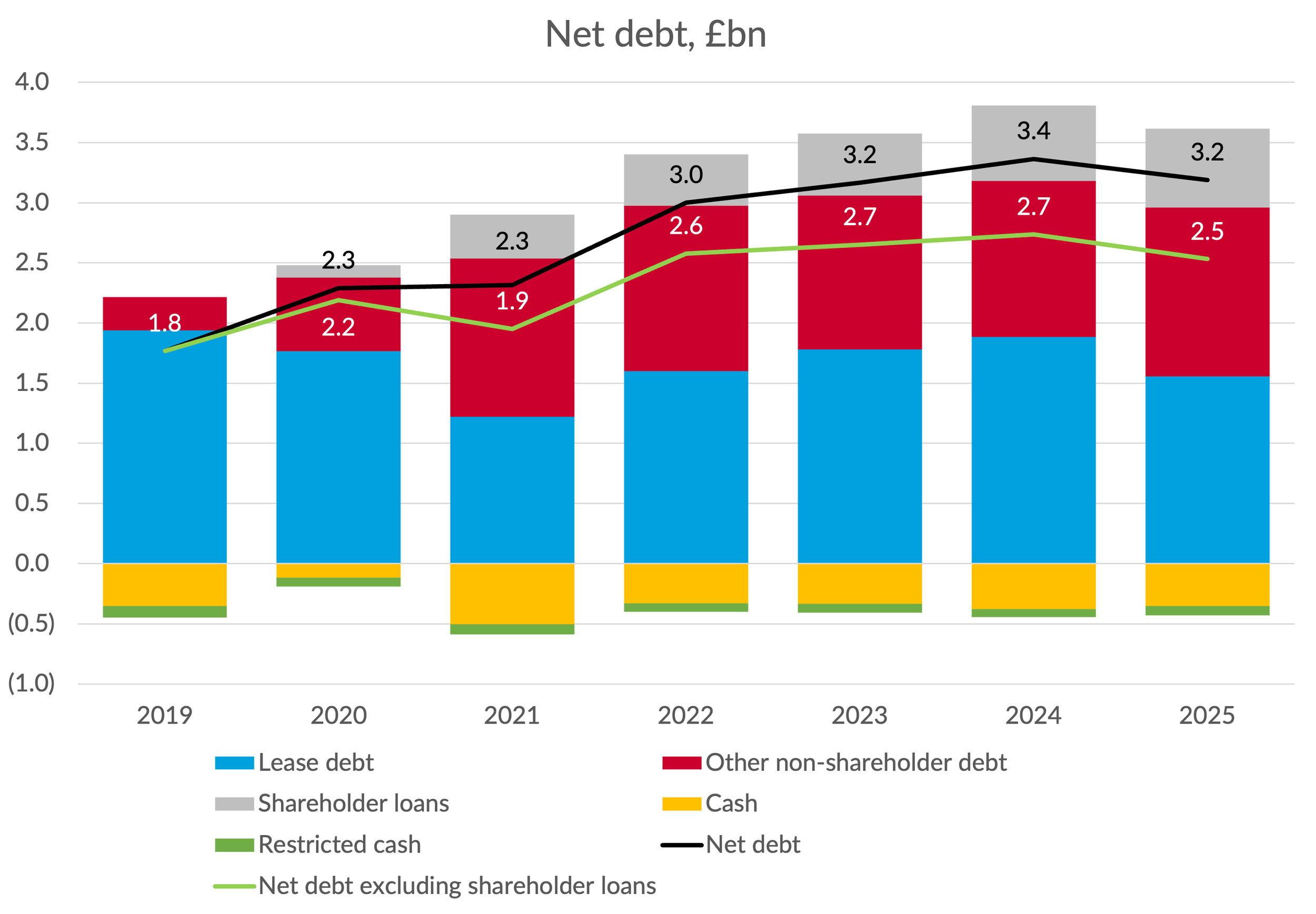

Virgin have been investing heavily in new aircraft and, as we’ve seen, not generating any profits. As a result, their net debt levels have been on a rising trend, although they did dip slightly in 2025 as they took a break from taking on new aircraft (see next chart). Virgin argue that their shareholder loans are not really debt since they don’t pay interest. They were supposed to be repaid in 2026, but Virgin’s shareholders agreed to extend the repayment date to 2030. The accountants rewarded that by reducing the value of the loans on Virgin’s balance sheet by £98.3m, which also helped reduce the reported debt total. A debt that doesn’t pay interest and apparently never needs to be repaid perhaps does deserve not to be included in net debt, so as well as the statutory definition of net debt, I’ve also shown the figures excluding shareholder loans. On that basis, net debt stood at £2.5 billion, representing 75% of revenue. That’s pretty high by any standards (the equivalent figure for BA was 37% for reference).

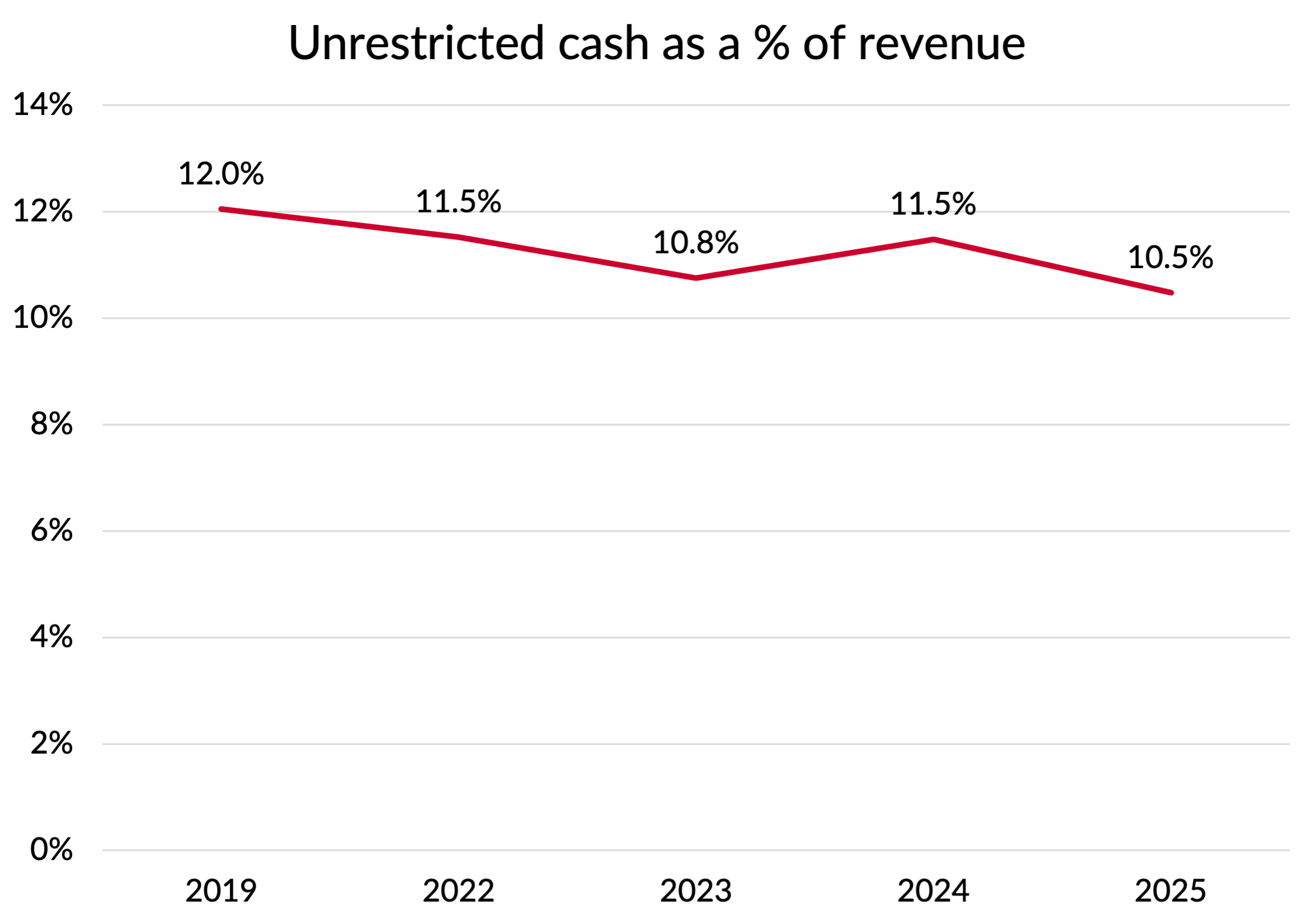

Cash levels have also been on a downward trend, at least when expressed as a percentage of revenue. In the chart below I included 2019 for reference but missed out 2020 and 2021 as revenue basically disappeared making this ratio rather meaningless.

The unrestricted cash balance of £353m at the end of 2025 was almost identical to the one Virgin had at the end of 2019, despite revenues having grown by 15%. As a side note, cumulative inflation since 2019 has been about 30%, so in inflation adjusted terms Virgin’s revenue is about 15% smaller than pre-pandemic and its cash balance is 30% lower.

Holding cash of 10.5% of revenue is about half the 20% guide level we used to use at IAG as a healthy cash balance. Another way of looking at the adequacy of cash levels is with reference to the value of pre-sold tickets. Virgin’s cash at the end of 2019 was equivalent to about two thirds of that value, whereas at the end of 2025 it is only half. Basically, Virgin has already spent half the money it has collected from customers for flights not yet operated. To be clear, I’m not saying that Virgin is going bust, just that its shareholders Virgin Group and Delta Airlines have not provided the company with any cash cushion to deal with things going wrong. In fact, they are even less well prepared financially for the next crisis than they were for the pandemic.

Fuel hedging

We now know of course what that next crisis is going to be - the huge rise in jet fuel prices triggered by the war with Iran. Virgin spent £774m on fuel during 2025 and as we saw earlier, they paid an average price of £639 per tonne, around $850. Current jet fuel prices in Europe have reached $1,875, more than double last year’s prices.

How well hedged are Virgin on their fuel expenses? Virgin don’t give a lot of information about their hedging position. They say that their policy “enables us to hedge an average of 50% of our exposure in the next 12 months”, but were they actually maximising that headroom when the crisis hit?

In the notes to the accounts, they show that a 30% rise in the fuel price would increase the value of their hedging positions by £68.4m. Since the physical cost of fuel would go up by £232m in that scenario, that seems to suggest that they were only 29% hedged at the end of 2025. The equivalent number for BA calculated in exactly the same way was 68%.

They also show that they had hedging contracts for 5.2m barrels of crude oil and 1.2m barrels of crack spread. Their annual fuel consumption is about 9.5m barrels of fuel, so the crude element is 57% covered but the crack spread is only 23% hedged. Given that 65% of the recent increase in fuel prices has come from the crack spread widening, Virgin’s fuel hedging position looks pretty weak to me.

Squeaky bum time I suspect at Virgin.