European network airline results for 2025 - the calm before the storm?

Hamad International Airport, Doha - October 2013, one month before opening. A personal photo taken on the occasion of Qatar Airways joining the oneworld alliance.

The full year results for 2025 are in

With Lufthansa releasing their results on Friday, we’ve now had the full year results from all three of the big Western European network carriers. Of course, the attention of analysts was less on the backward looking figures for 2025 and more on the implications of the war in Iran for the 2026 outlook.

I will come back to that question later in this post, but let us look first at last year’s performance. As usual, most of the charts that follow will look at “rolling 12 month” figures to show the quarterly trends without being affected by seasonality.

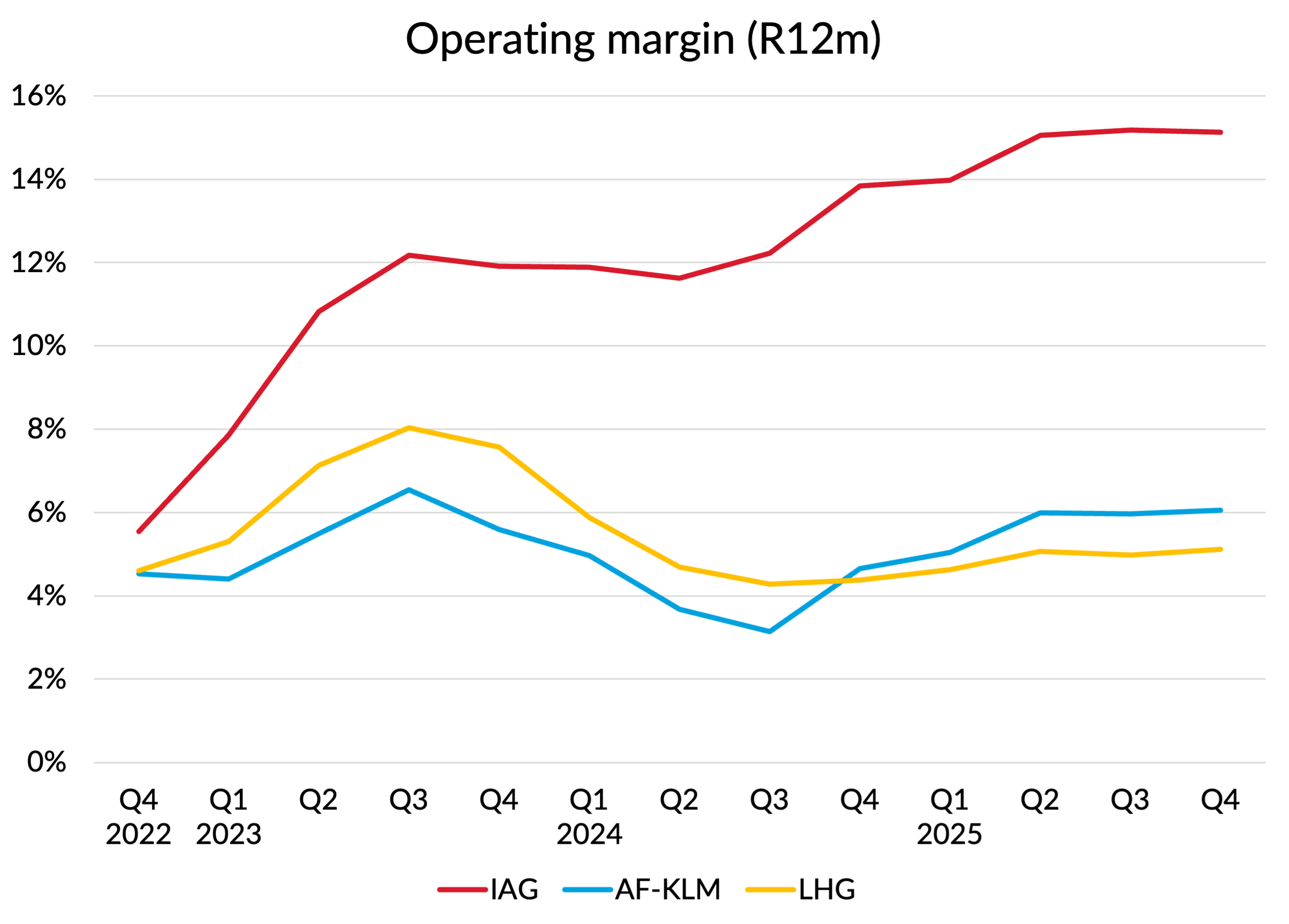

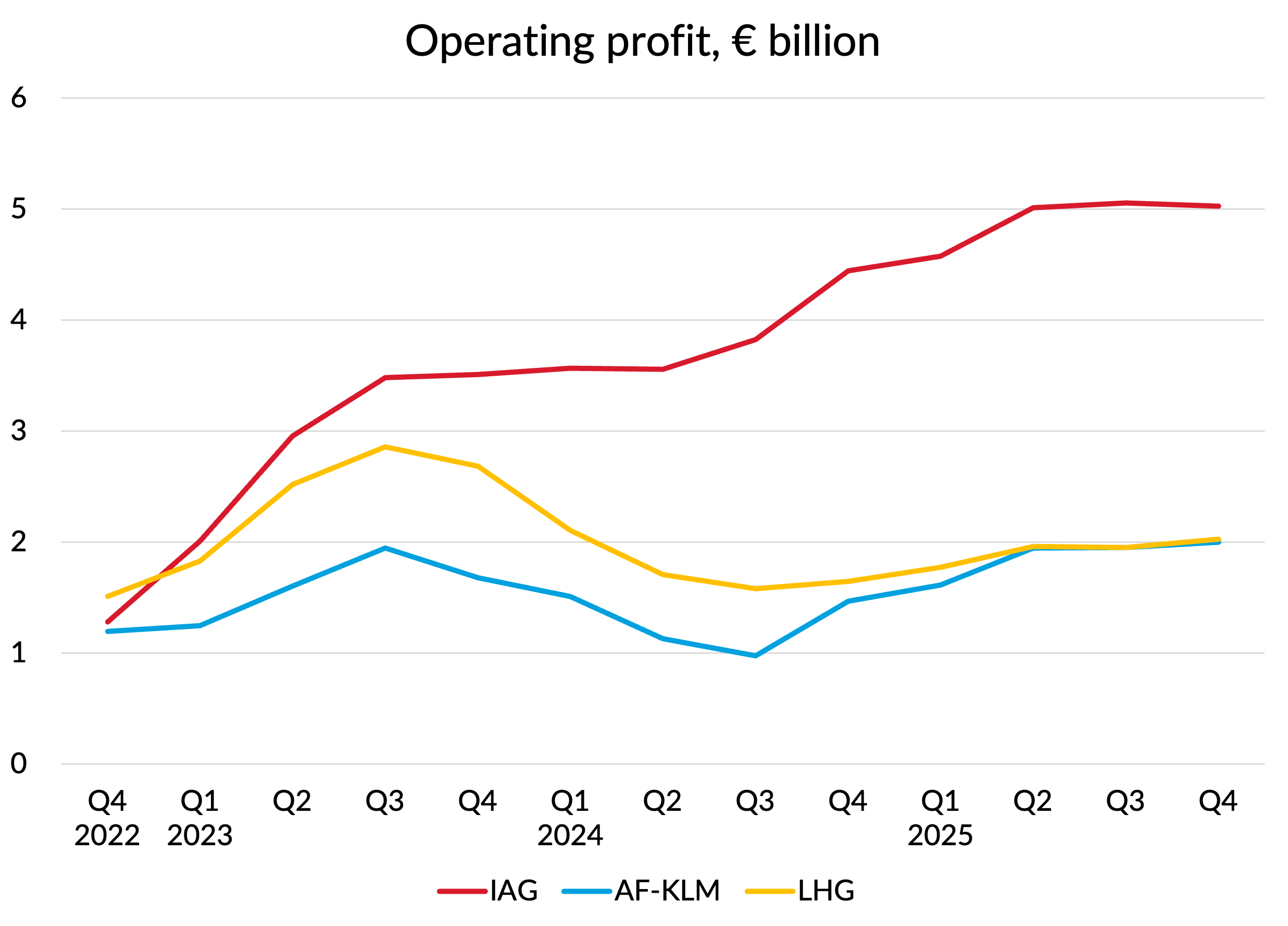

Operating profitability

Margins have been quite stable at all three carriers recently, but IAG continues to lead the pack with more than double the level of profitability of the other two. Despite having a much more stretching target margin range (12-15%) than Lufthansa’s (8-10%) and AF-KLM’s (> 8%), IAG is already delivering performance at the top end of its target range, whilst the other two are still some way below the bottom of theirs.

Lufthansa is about 20% bigger in revenue terms than the other two, thanks to its relatively larger MRO and Cargo businesses. So in terms of absolute operating profits, it manages to sneak into second place in the rankings when it comes to total operating profits over the last four quarters.

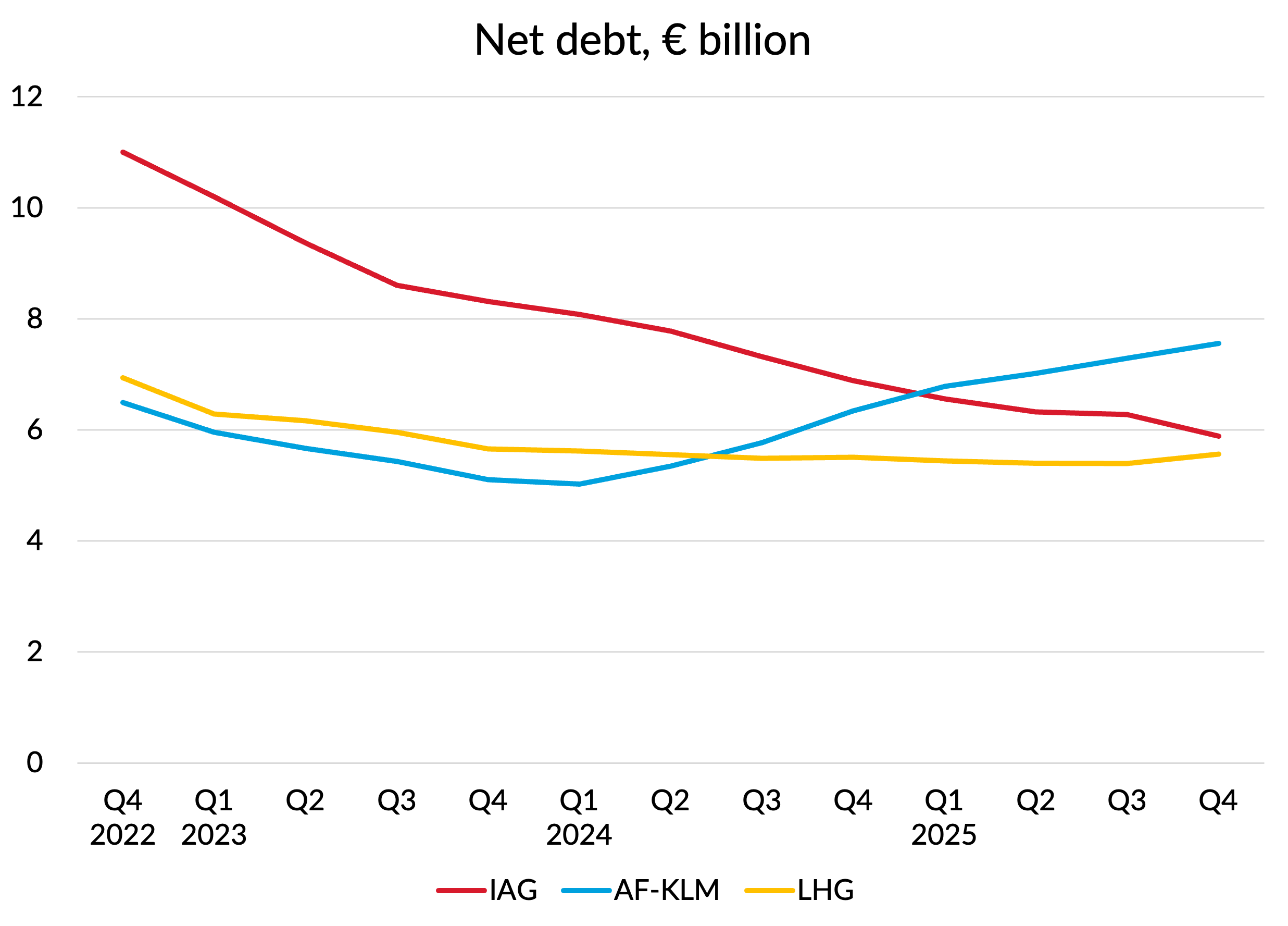

Net debt

Despite making significantly larger payments to shareholders through a mixture of dividends and share buybacks, IAG’s superior profitability has enabled it to reduce its net debt much faster over the last few years, a trend which continued into the final quarter of 2025.

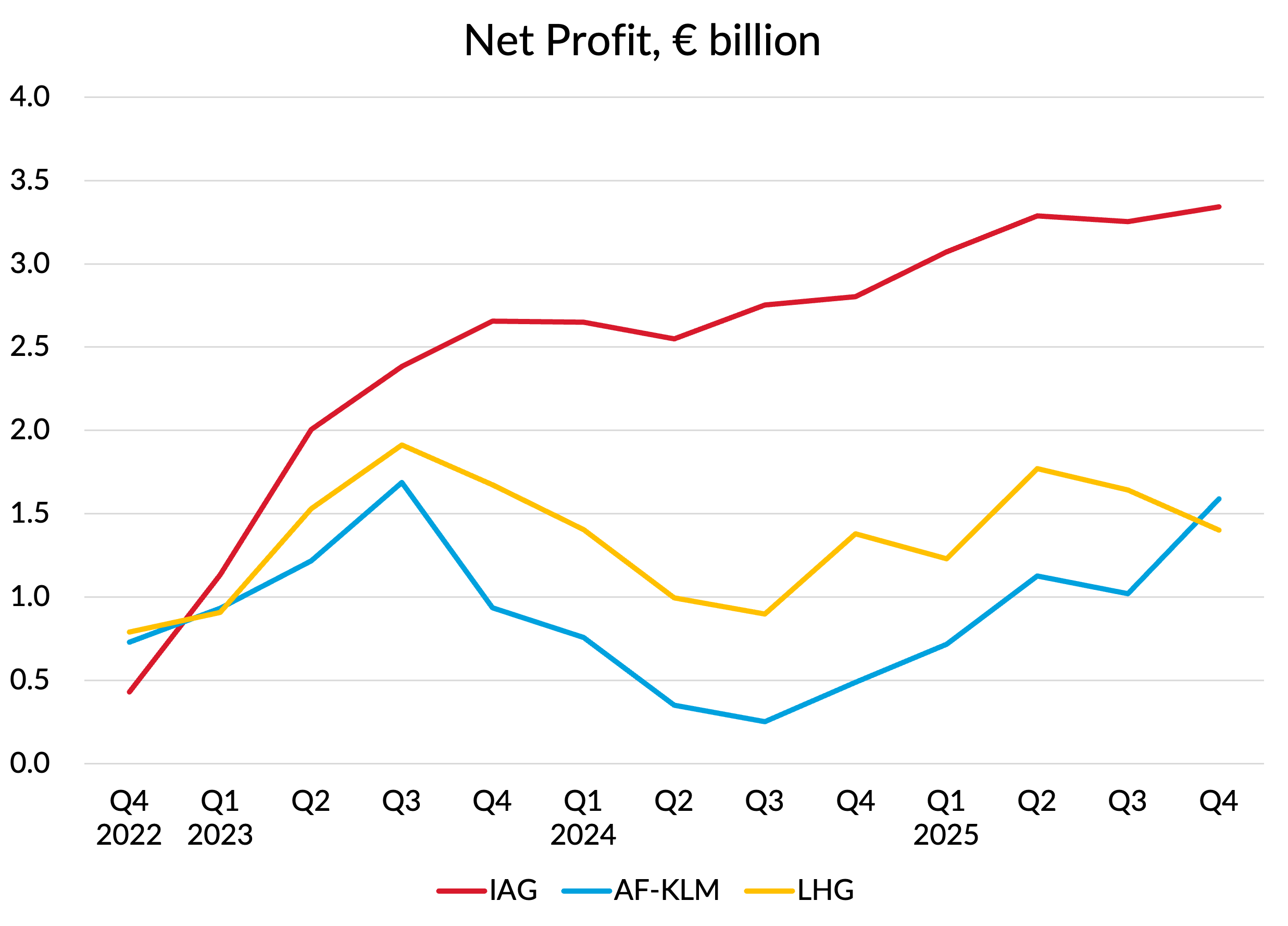

Net profit

IAG’s superior operating profits and cashflows contributed to a much healthier trend for net profits too, with the group making more profits that the other two combined in 2025.

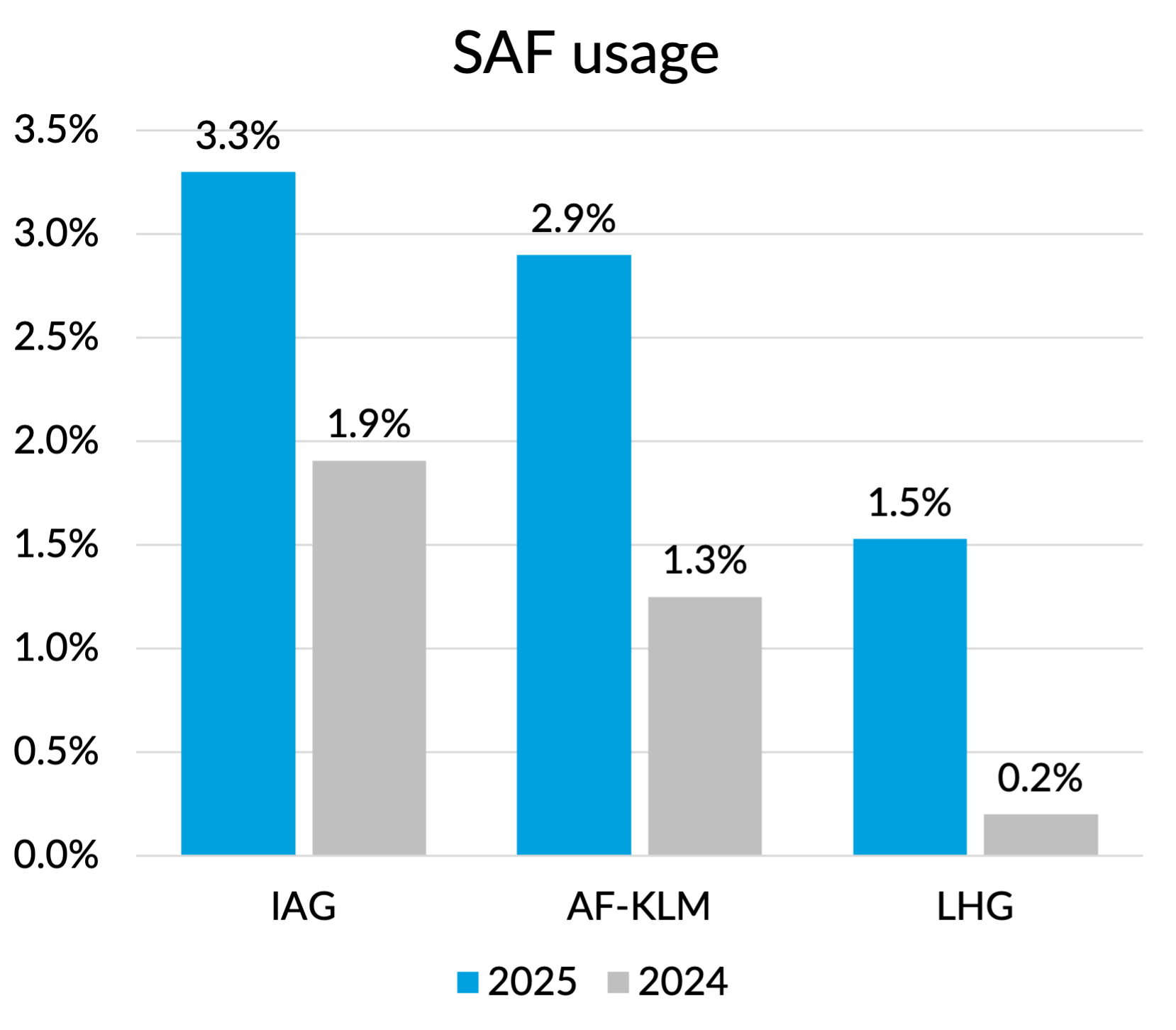

SAF usage

Before moving on to the outlook for 2026, I did want to share some interesting statistics disclosed by the carriers on their use of Sustainable Aviation Fuel (SAF) in 2025. All three groups significantly increased their use of SAF compared to 2024, in part in response to the introduction of SAF mandates in Europe. But despite a big jump compared to last year, Lufthansa Group remains the laggard of the three in terms of the percentage of their fuel use coming from SAF.

Outlook for 2026

The outlook statements for IAG and AF-KLM were both given before the Iran war kicked off, whilst Lufthansa’s later release meant they were able to provide some more commentary on the likely impact of the war.

IAG indicated a “positive outlook” overall and guided non-fuel unit costs down around 1%, including an FX benefit of 2%. Other figures given were for a capacity growth of 3% and capex of €3.6 billion.

AF-KLM also declined to give specific guidance on the outlook for profits or revenues. Unit costs were guided as being up 0-2% at constant exchange and fuel prices, and excluding increases in ETS costs. Maybe that’s a bit worse than IAG’s guidance for costs, but pretty similar. Capacity growth was given as 3-5% and capex plans totalled €3 billion.

Lufthansa’s main outlook statement was also given on a “pre Iran war” basis. Capacity growth of 4% and net capex of €2.9 billion is planned. Non-fuel unit costs were expected to increase at about half the rate of inflation. They stuck their neck out a bit more on profitability, forecasting that adjusted EBIT would be “significantly above 2025”. But quite how big an increase would be regarded as significant is not clear.

What about the impact of the war?

Lufthansa had quite a bit to say about the likely impact of the Iran war on the outlook for 2026, and I think they summarised the main issues well.

The first topic is the spike in fuel prices. With tankers unwilling to sail through the Strait of Hormuz, crude oil prices have jumped from around $60/barrel at the start of the year to over $87 today. Even worse for airlines, jet fuel prices have risen much more. The “crack spread”, which gives the difference between the prices for jet fuel and crude oil has hit an all time record of over $100/barrel in Europe due to worries about disruption to supplies. This has resulted in jet fuel spot rates hitting an eye-popping $1,473 per tonne in Europe, compared to levels of around $810 in late February.

European airlines are well hedged on fuel prices in the short-term, with Lufthansa 77% hedged for 2026 and both IAG and AF-KLM hedged at 62%. These hedges are weighted to the early part of the year and airlines hope and expect that any supply disruption will be short-lived. There is even an opportunity to gain at the expense of the US carriers, who don’t hedge their fuel costs at all.

Next is the impact from the closure of Gulf airports and airspace. There is a direct profit hit from flight cancellations, which Lufthansa estimated at €5m a week. However, in their case they said that this is being more than offset by the positive benefit from the elimination of Gulf carrier capacity, with Lufthansa saying their bookings on Asian and African routes for 2026 had jumped by 20%. The airline is redeploying capacity from the Gulf to Asian markets to take advantage. Cargo revenues are also getting a big boost, with 18% of global air capacity being taken out of the market and shippers desperately looking for alternative lift.

According to Lufthansa, there does not appear to be any negative impact on bookings on the transatlantic or for travel within Europe, at least so far. Overall, Lufthansa stuck to their guidance for 2026 profits despite the war, although they acknowledged the much greater uncertainty.

Share price impacts

Airlines always take a hit to their share prices at times like this. Some of that comes from the direct impact of higher fuel costs and disruption to travel, but the general rotation of equity markets away from “risky assets” is probably more important.

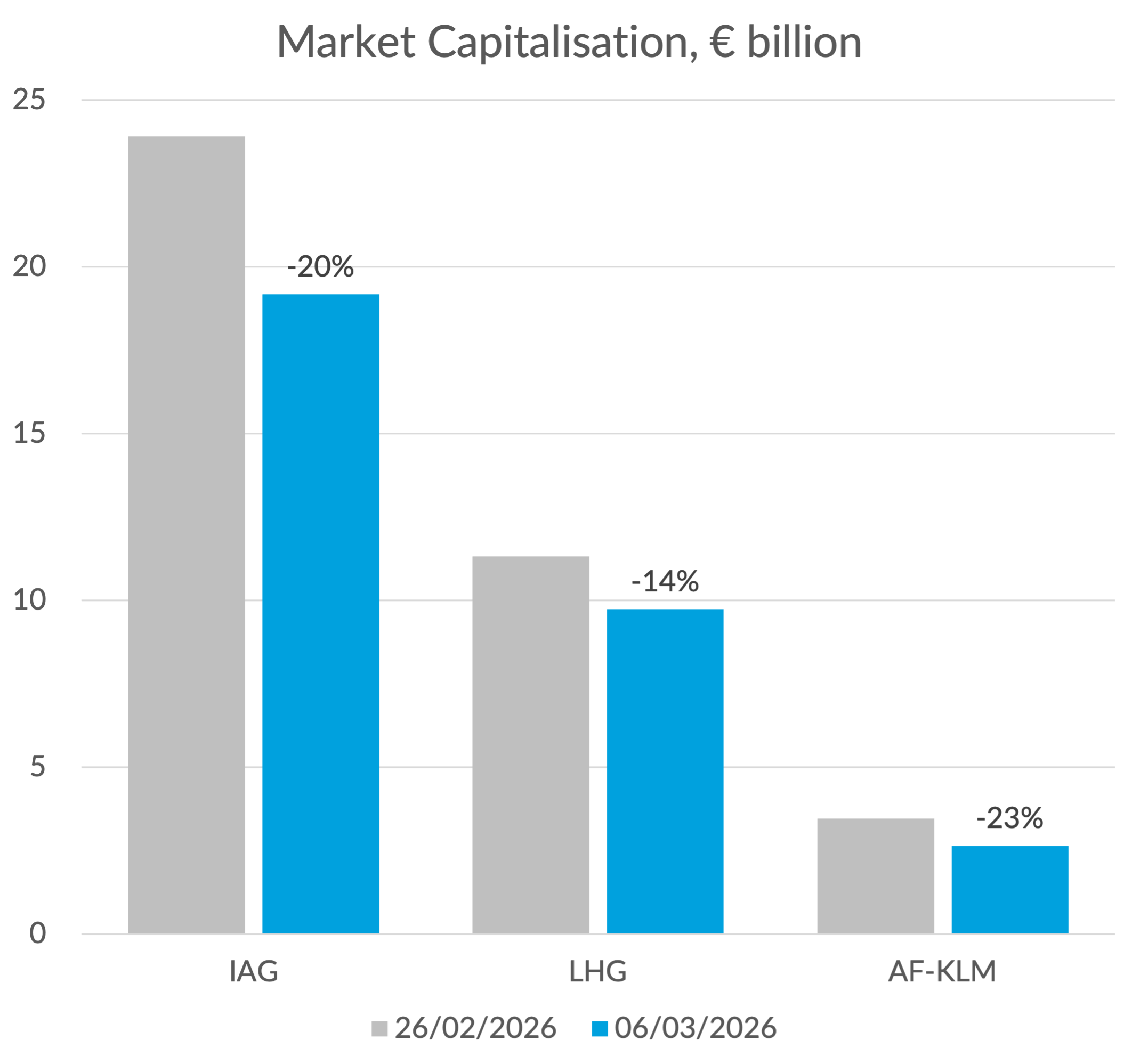

In the chart below, I’ve shown the change in market capitalisation for the three groups over the last 11 days, with IAG losing 20%, or €4.7 billion. Have expectations for IAG’s future cashflows really fallen by €4.7 billion as a result of the war? I don’t think so. That’s equivalent to completely wiping out IAG’s post tax profit for around a year and a half.

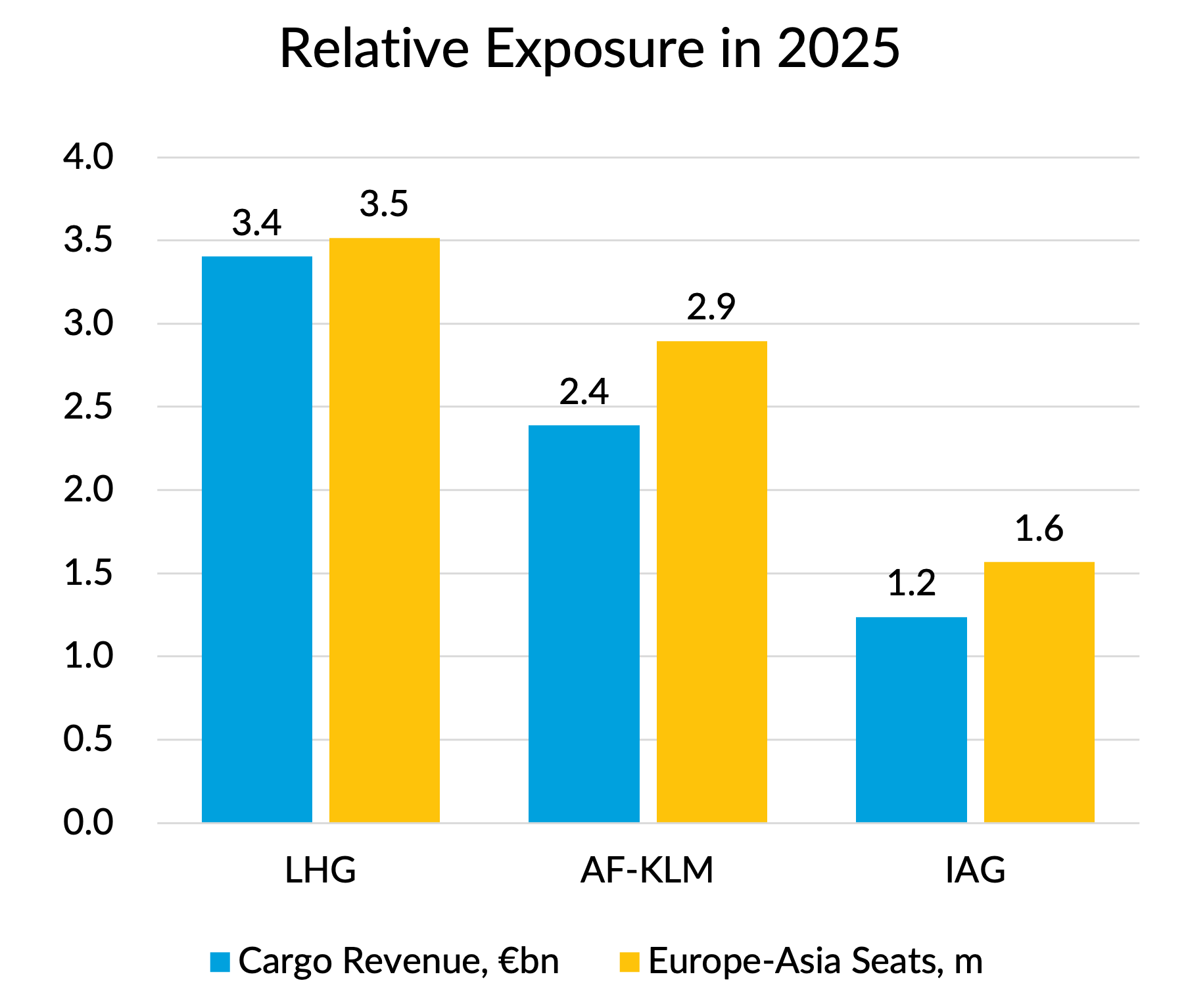

Lufthansa’s share price has been the least impacted in percentage terms and maybe that’s fair. With a higher exposure to Asian routes and a bigger cargo business (see next chart), they probably stand to benefit the most from the reduction in Middle East capacity. Their higher level of fuel hedging will help too. In absolute value terms, they lost €1.6 billion, only a third of the value hit that IAG took.

AF-KLM’s market capitalisation only dropped by €800m. Like Lufthansa, they have a fair amount of Asia capacity and a large cargo business. But the absolute value loss was also heavily constrained by the fact that their market capitalisation was only €3.5 billion to start with.

Lasting impacts

Nobody knows how long the current military action in Iran and the associated disruption to the oil and fuel markets will continue. It is possible that President Trump will quickly decide to “declare victory” and end the war, with Iran ending its retaliatory strikes in response. So far, there hasn’t been any real lasting damage to oil infrastructure, so things could in theory get “back to normal” within a few weeks, with oil and fuel prices falling back and Gulf airspace reopening.

Even in that most benign of scenarios, it seems likely that the risk of hostilities breaking out again and terrorism risks will remain elevated. Will there be a long-term impact on the attractiveness of the Gulf as a tourism destination, or on the confidence of travellers to transit via Gulf airports? European airlines might hope to get a lasting benefit from that, but personally I’m rather sceptical. Traveller memories are short and the Gulf carriers will cut prices if needed to fill their aircraft.

A scenario where the Gulf carriers remain disrupted is much more likely to be associated with prolonged conflict and longer lasting impacts on energy prices. That will spill over into global economic impacts which are never good for airline demand and profitability.

The industry argues that it is much more resilient to economic and other shocks than it used to be. Low airline valuations relative to profits suggest that investors remain sceptical of this.

For years, investors have priced airlines as though the next shock is always just around the corner, with profits turning rapidly into losses. 2026 may be the year to test whether that scepticism is still justified.