Impending news on Heathrow’s third runway project

Are we about to get some clarity on the government’s preferred plan for LHR?

Next Wednesday, the UK's Chancellor of the Exchequer Rachel Reeves will announce details of the country's annual budget. The last couple of months have been filled with a blizzard of media rumours and speculation as the Chancellor desperately seeks to reconcile a raft of conflicting objectives. She wants to boost the UK’s moribund growth rate and protect public spending plans (“no return to austerity!”), all whilst avoiding unpopular tax rises and without spooking the bond market.

Whether or not she manages to pull off this balancing act successfully, one thing is certain. She loves projects like the third runway at Heathrow which drive growth but can be financed entirely by the private sector, at least in theory. So it seems likely that in addition to finding out how much more tax we will all be paying, we may also get some announcements on Heathrow next week from the government.

To move forward with the third runway, the government needs to redo its “Airports National Policy Statement” (ANPS). The last one received parliamentary approval in 2018, but COVID put paid to that plan. Too much time has now passed for the government to proceed without redoing it.

The last ANPS set out the preferred location and scheme for new airport capacity and defined key parameters such as the runway length and the number of additional air transport movements that a scheme should deliver. It also set high level conditions and requirements, mostly of an environmental nature. But details of the precise design were left to be decided during the “Development Consent Order” (DCO) phase. It also left open the question of who would build the runway and related terminal infrastructure. As well as proposals from incumbent HAL, there was a competing proposal from Heathrow West Limited (HWL), backed by Arora Group. Arora are significant land owners and property developers at Heathrow and at other airports. For example they built the T5 Sofitel and the Hilton Garden Inn in the central terminal area, in both cases on time and on budget.

What might get announced next week? The big question is whether to stick with the statement in the previous ANPS that the runway should have a length of “at least 3,500m”. That is still HAL’s proposal, but HWL are pushing an alternative plan for a lower cost 2,800m runway option. The HWL plan would avoid moving the M25, with all the cost, complexity and risk that would entail. In a statement to parliament last month, Transport Secretary Heidi Alexander said that “the M4 and M25 must not turn into Europe's largest car park” during the construction work. Is that a hint that the government is at least considering a switch of plan? Or just an indicator of a long list of expensive mitigations that will be imposed, further pushing up costs?

If an announcement on this is indeed planned for next week, one would think that this critical decision has already been made. But I thought it would be worth summarising the issues at stake, as well as highlighting the other key decisions that will need to be made in subsequent steps.

What does the market need?

Before talking about the details of the different schemes that have been proposed, I think it is worth reflecting on what new infrastructure is needed by the market. It is important to understand that Heathrow has been slot constrained for decades and there have been strong economic drivers for slots to migrate to their highest economic value use. Since you get a lot more revenue and profit from a long-haul flight than a short hop to a UK domestic destination, that has meant that short range services have been crowded out over the years in favour of extra long-haul flights.

You can see this from the following chart of annual departing flights by distance band. The blue bars show the number of flights under 1,000 km, which have dropped by 22% over the last twenty years. The red bars show the number of flights over 4,000 km, which have grown by 38%. That’s an annual growth rate of 1.6%, which isn’t very different from the growth rate of long-haul flights from other Western European hubs like CDG and AMS, although it is below the growth rate of long-haul flights from Western Europe as a whole, which has averaged 2.9% over the same period.

My point is that if the runway capacity constraint is released and the process of continually eroding LHR’s short-range network is halted and goes into reverse, the main increases in flight numbers will happen at shorter flight distances. Yes, the restoration of LHR’s short-range network will drive incremental feed into the long-haul network, stimulating long-haul growth in destinations, frequency and average aircraft size. But what the airport is going to need most is extra capacity suitable for narrow-body operations. Those extra short-haul flights don’t need super long runways or huge wide-body stands. The passengers on those flights won’t want long walking distances or to have to take a train to get to their gate. And the flights need to be kept as close as possible to existing long-haul services so that connections can be fast and efficient.

So how well are these market needs being met by the proposals from HAL and from HWL?

Size isn’t everything

For some reason, HAL seem to be fixated on building a “full length” runway. Quite why a three runway Heathrow should need three very long runways is not clear, when 98% of existing take-offs at Heathrow last year would have been able to use a 2,800m runway without operational penalty. Most of the 2% that used more runway distance could probably have taken off fine with a bit more throttle. Or more obviously, those can just continue to use one of the existing runways.

If the third runway was being built in a desert, you would probably build it longer for maximum operational flexibility, as the cost of a bit more concrete isn't that big. But when the cost of accommodating a longer runway is having to divert a 12-lane motorway and meddle with one of the most complicated and busiest motorway junctions in Europe, you surely need a really compelling reason to do so, which I don’t see.

Heathrow’s biggest operator, British Airways, has spoken out in support of a shorter runway option. Speaking recently at the Airlines 2025 conference in Westminster, BA’s CEO Sean Doyle said:

"If you can avoid moving the M25, you should avoid moving the M25. I can't argue against the logic of that. I think we should look at ways of potentially building a shorter runway."

How hard can it be to move a motorway?

HAL play down the difficulties of moving the M25, but even they put the price tag at £1 billion back in 2018. Experts believe that this is almost certainly an underestimate, even allowing for cost inflation since.

It is also a huge risk factor in the timeline. Clearing and preparing ground, building runways, terminals and baggage systems are all expensive and risky projects. But moving a 12-lane motorway without disruption is quite another.

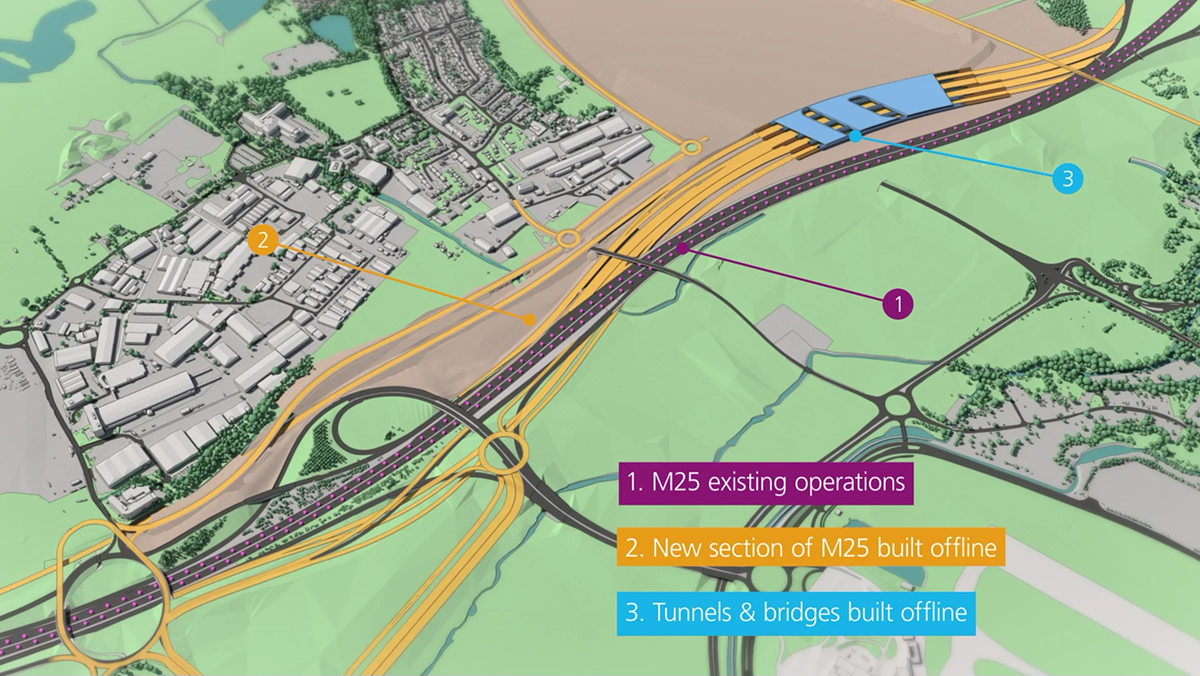

Let me illustrate some of the complexities. To provide adequate clearance above the M25, the runway will need to be raised by 5m above ground level. That might not sound like a lot, but you need an awful lot of dirt to lift a km or so of runway up by 5m. All of that soil will need to be brought in by truck on roads that are already full.

The M25 also needs to be moved 100m west and dropped in elevation by 7m. I’ve shown below HAL’s overview of the scale of works required. The picture shown here already looks scary enough, but one of the trickiest parts will be to reconnect the M25 back into the junction with the M4. As well as linking in with a complex set of slip roads, the M25 needs to climb back up to an elevation high enough to get over the M4 in a very short distance. On the plan below that’s at the top right of this image and you can see that they don’t really show how they are planning to do this.

HAL would say that the competing proposal from HWL will also need to bridge the runway over a motorway, in this case the M4 spur road that links the M4 to the central terminal area (see diagram below). HWL point out that the complexity and cost of doing that is of a different order of magnitude to moving the M25. The section that needs to be bridged is a simple stretch of dual carriageway. The elevation of the roadway doesn’t need to be changed and the overall effect on the runway earthworks is limited due to the height of the existing terrain at this end of the airport. The traffic volumes on the M4 spur are also a fraction of what the M25 carries.

Terminal and apron layouts

It is unlikely that the government will say anything next week about the terminal infrastructure and apron layouts that go with the third runway. But that will be at least as big a decision as the length of the runway, and the two competing proposals take a very different approach.

HAL are proposing new terminal infrastructure next to T5, with only 18 stands as far as I can tell, despite occupying a huge area. I guess the rest of this space is intended to be taken up by a massive shopping mall. There is another big satellite terminal building adjacent to the new runway which hosts the other 28 pier served stands. The majority of the passengers using the new runway would need to travel by track transit out to the new satellite. As well as being an expensive option, it is also not very passenger friendly.

In their alternative plan, HWL are proposing parking stands and provision for maintenance facilities near the third runway, but all the contact stands and terminal facilities are located adjacent to the existing T5. Even the furthest stands are accessed via a passenger bridge - no track transit required.

In terms of stands, at this stage of planning, HWL is showing them as flexible between narrow-body and wide-body. In “max narrow-body” mode, the HWL layout provides 46 pier served stands in the area next to T5, plus another six off-pier. There would be fewer stands if used for wide-body services, but as we saw earlier, most of the incremental movements enabled by the third runway will be short-haul flights operated by narrow-bodies. Those new stands should be easily enough to handle the extra 40m passengers the new runway is expected to deliver.

You can see from the plan below that it avoids moving the M25 and the development “wraps around” existing buildings along the A4, rather than bulldozing them as the HAL plan does. Overall, the plan requires 49 hectares less land.

It won’t surprise you to hear that I think it is a far better plan.

Who will build and operate the new facilities?

In principle, the location and length of the new runway, the layout of the terminal facilities and apron, and the identity of the developer and operator are all independent decisions. But would HAL embrace an alternative vision for the runway and the terminals if they are confirmed as the developer? I’m sure that HWL would live with a 3,500m runway decision and leave HAL to build the runway element if they were allowed to take on the role of delivering and running the terminal facilities, which could still follow the design vision set out in their proposal for those elements.

Some people question the operational and financial practicality of having different companies develop and operate different parts of one airport. But that is exactly what happens at airports like New York’s JFK. The cargo facilities at Heathrow are separately owned and managed today. BA runs the operations at T5, except for passenger security screening. There are precious few opportunities to introduce some much-needed competition into the provision of airport facilities at Heathrow. The third runway is one of those.

If the government leaves open the question of who will build and operate the new facilities, it will be important for them to set out a clear and transparent process to make that decision. Nobody is well served by having this done behind closed doors without proper scrutiny. This is simply too big a piece of national infrastructure to allow that to happen.

Cost differences

In headline terms, HWL estimate that their proposal will cost a cool £10 billion less than the £33 billion bill outlined by HAL for the third runway element of their plans. HAL also want to spend another £15 billion adding terminal capacity in existing terminals to support bringing the total airport capacity up from 84 million today to 150 million by the early 2040s, bringing the total bill to an eye-watering £49 billion. The reason that doesn’t quite add up is due to rounding, which of course increases the total, but then what’s a billion pounds between friends?

Nobody really knows where the £10 billion difference on the supposedly “like for like” element of the HAL plan comes from. Although HWL have given a pretty detailed breakdown of their figures, HAL have not done the same, at least publicly. Some of the difference of course is down to the higher cost of the roadway changes, the cost of terminal facilities near the runway and the track transit system that will serve it. Arora and the airlines also believe that there is a lot of “gold-plating” and inefficient procurement by HAL, linked to a cost-plus regulatory system that rewards the airport for spending more.

If HAL are given the go ahead to spend £49 billion on the airport, that will inevitably push up prices for airlines and their customers. The “Regulatory Asset Base” used to set charges is about £20 billion today, and results in airport fees that are amongst the highest in the world. There is no way that spending another £49 billion won’t push up airport charges a lot. I think there is a real risk that if HAL is permitted to build the wrong kind of infrastructure at the wrong cost for the needs of the market, the expansion of Heathrow could turn into something of a financial disaster story and national embarrassment.

Does the third runway even make economic sense?

Airlines, including BA, are still supportive of building a third runway, but not at any cost. If we do get statements next week on LHR, it will be important to see whether the government reiterates assurances given in the past that airport charges should be kept “close to current levels”.

HAL has set out what it sees as the economic benefits of the development. I do believe these are significant, but HAL’s numbers and the way they have built them up don’t make much sense to me. For example, they say that any increases in costs to airlines won’t be passed on to consumers. At the same time, they assert that the elimination of “scarcity rents” will see consumer prices fall by the equivalent of £80 per short-haul passenger. All of this will be achieved at the same time that passenger numbers rise by 79% and the airline industry absorbs ever rising emissions costs.

Personally, I believe that even the lower cost HWL scheme is at the limits of what might be affordable for airlines and justified economically. Frankly, if economics were the only consideration, what should actually be done is to lift the 480,000 air traffic movement cap imposed on the airport when T5 was approved and move to fully exploit the potential of the existing runways. You could probably get another 20% increase in movements if “mixed-mode” was adopted. Yes, additional terminal capacity would be needed to go with that, but it could be delivered at a fraction of the cost of any of the third runway schemes. It wouldn’t be popular with local residents but they would probably prefer it to a third runway, so surely it should be considered as a valid option?

Final thoughts

Whatever position you take on whether expansion of Heathrow should proceed, if it does the development must be done in a way that meets the needs of the market - the airlines and customers that use Heathrow.

The biggest tragedy would be if local residents, airlines, travellers and the UK economy all end up as losers because the wrong development is allowed to go ahead.