Castlelake confirms interest in a potential bid for easyJet

Castlelake considering a bid

On Friday, the news broke that the US based alternative investment company Castlelake was considering a bid for easyJet. Castlelake has a history in aviation, including as an aircraft lessor and as a partner to Air France - KLM in the acquisition of SAS. It is not known at this point whether the company is working with any airline partners, or is considering a bid as a purely financial transaction.

What might they have in mind? And why has easyJet become a potential takeover target? I had a look.

Long term share price underperformance

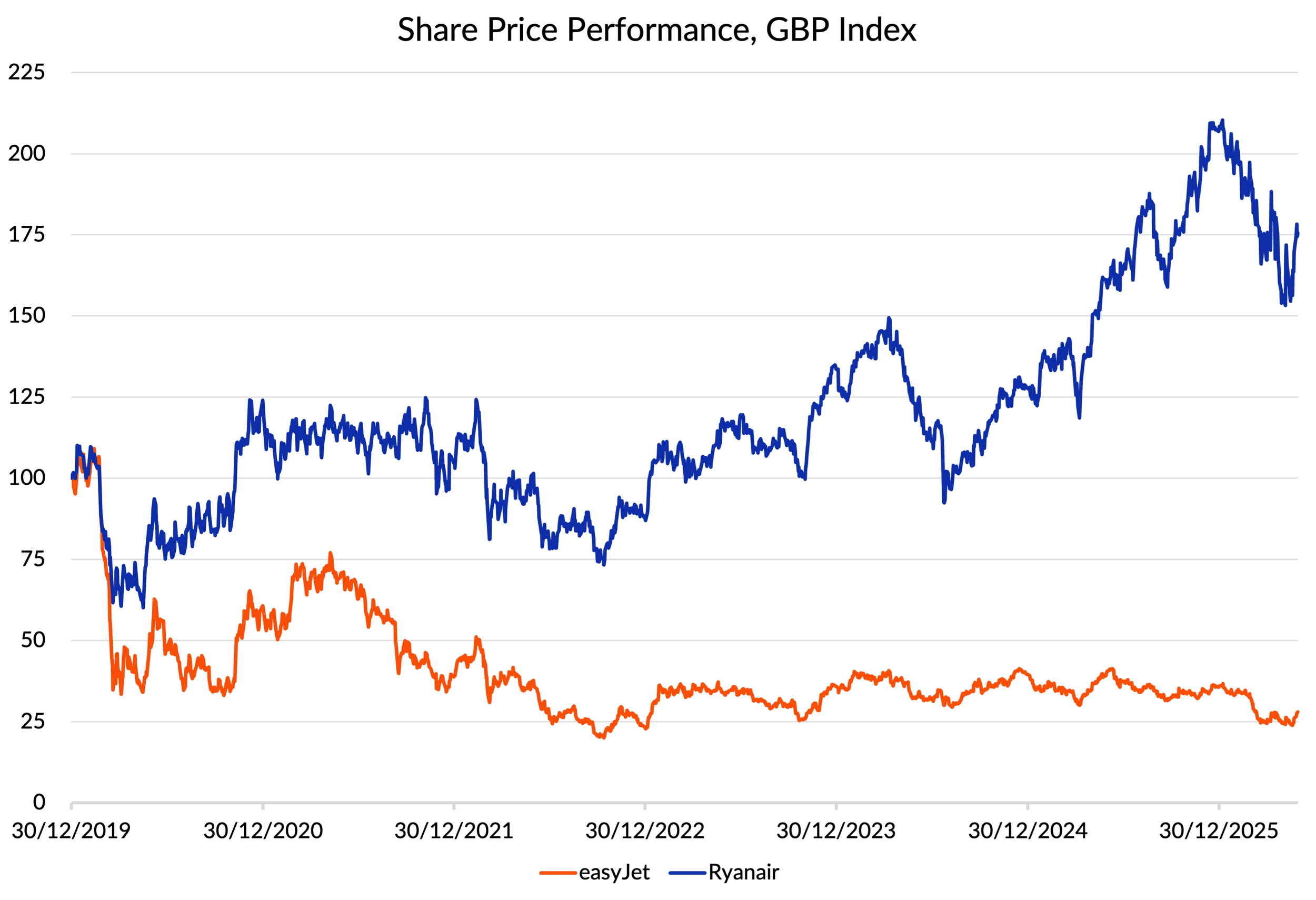

It is perhaps not surprising that easyJet might have become a takeover target, given the performance of their shares over the last few years. At the end of 2019, the company was valued at £4.8 billion and that has fallen to only £3 billion today. In fact, it’s even worse than that, because the company raised £1.7 billion of fresh equity capital during COVID. So overall, that’s £3.5 billion of shareholder value destruction.

In contrast, arch rival Ryanair has raised its value from €16 billion at the end of 2019 to €26 billion today. It did raise €400m of fresh equity during COVID, but it has spent over €2.4 billion in share buy backs since, giving an overall value creation of over €9 billion (£8 billion).

Another way of looking at this is to show the share price performance (see following chart). Since the end of 2019, Ryanair’s shares are up 76% in sterling terms, whilst easyJet’s are down by 72%.

Source: Yahoo Finance

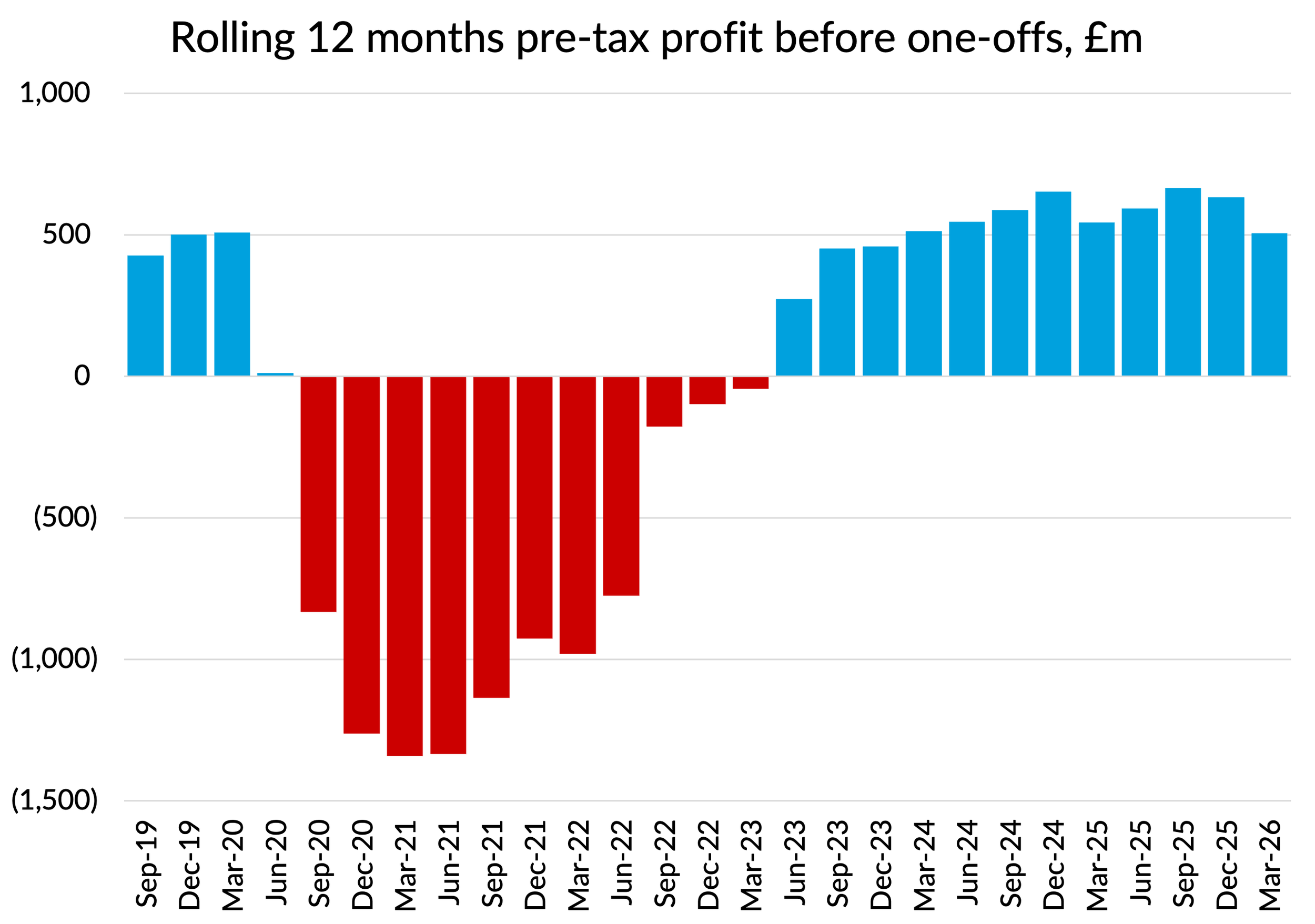

Pre-tax profits at easyJet did recover after big losses during COVID, getting back to similar absolute profit levels as before the pandemic. But adjusting for inflation they are down over 20%. Operating profit margins over the last twelve months of 5% were down from the 8-9% they used to make and compare poorly to Ryanair’s 15.8% margin for the same period.

Source: Company reports

Caught between a rock and a hard place

The huge rise in fuel prices since the latest phase of the Iran war has piled the pressure on easyJet’s management. On the one hand, the outlook for the profitability of their business has taken a hit. They are 72% hedged for the April to September period, but that still leaves 28% exposed. Their guidance on near term bookings didn’t suggest that they were having much success with passing on the fuel price increase. Ticket yield for their September quarter was described as “modestly up”.

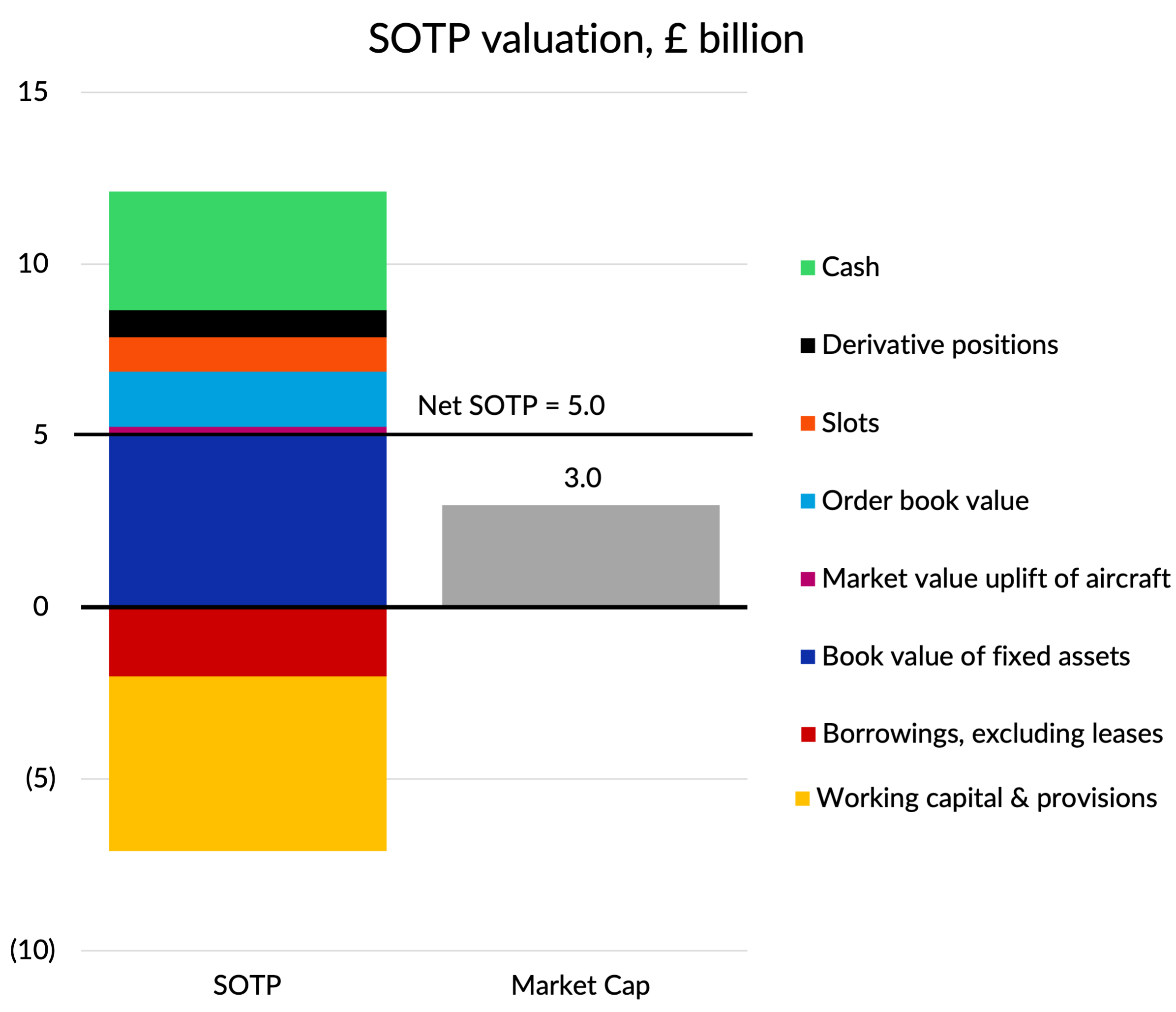

At the same time, the value of their aircraft assets has been going up. Higher fuel prices have increased the urgency with which airlines want to bring in new more efficient aircraft, but aircraft and engine supply chains are still clogged. The value of easyJet’s fleet of largely unencumbered A320/321neo aircraft has become a material percentage of the value of the company. Taken together with high cash balances, the “sum of the parts” (SOTP) valuation of easyJet may be substantially in excess of the actual market capitalisation.

Such exercises are notoriously difficult, but I thought I’d give it a go to illustrate how Castlelake may be thinking.

Sum of the parts

At the end of March, easyJet had aircraft and spares assets of £4.9 billion. That excluded their “right of use” aircraft assets, for which there is a matching lease liability on the other side of the balance sheet. I had a go at building up a market value equivalent, using assumptions for the value of their 208 owned aircraft, spare engines and other spares. I got to a figure of £5.2 billion. That’s a bit higher, but not a massive difference.

What is likely to be a bigger consideration is the value of their future order book. They have 287 firm orders and another 100 purchase rights. These are likely to have been placed at attractive prices. Boeing and Airbus normally offer airlines placing big orders better prices than they are willing to give to leasing companies. Taken together with the scarcity of delivery positions for A320/321neo aircraft, Castlelake may be assigning a significant value here. I’ve played with some figures, using $5m per A320neo position, $8m per A321neo position and $2.5m per purchase right. Are these figures correct? No, but they are not outlandish and suggest a “hidden value” of £1.6 billion.

As I mentioned earlier, easyJet has a lot of cash on its balance sheet. As at March 31st, they had cash of £3.4 billion, which exceeded their £2 billion of borrowings, leaving them with net cash of £1.4 billion excluding lease liabilities. However, most of their cash is actually customer money - the value of tickets which have been sold but where the travel hasn’t taken place yet. It would be wrong to include the cash in a sum of the parts valuation without also including that £3 billion liability.

There are some other working capital items that should be included too, notably £1 billion of maintenance provisions, another £1 billion of trade payables (net of receivables) and £0.8 billion of derivatives (“in the money” fuel hedges). A billion here, a billion there, can add up.

The last topic I want to discuss before I add up the numbers is the question of slots. The company has slots at quite a few slot constrained airports - this is one of the key differences between easyJet’s business model and that of the “ultra low cost carrier” models of Ryanair and Wizz. The Gatwick slots are probably the most valuable, with 196 daily pairs being worth perhaps £500m at the £2.5m per daily slot pair that past transactions might indicate. That price is probably too high in current market conditions, with carriers looking to cut back rather than expand. The second runway plan will also make airlines less likely to want to “pay up” for LGW slots. There is also a big difference between selling a few choice slots to a carrier with a specific need than trying to offload 46% of an entire airport. That’s not to say that the LGW position isn’t highly valuable, just that slot values are not a reliable way of assessing what you might get for selling it.

Elsewhere in Europe, easyJet has significant slot positions at other slot constrained airports, notably Amsterdam, Orly, Linate and Lisbon. Slots can’t be easily traded outside the UK, but there are mechanisms to do so if the value is high enough (e.g. moving the slots into a separate legal entity with an air operator certificate and then selling that company). For what it is worth, I am going to assume a total slot value of £1 billion for the purposes of my SOTP fag packet.

Without further ado, here’s my SOTP valuation, which adds up to £5 billion compared to the £3 billion “pre-bid” market capitalisation, a 67% premium. That’s certainly enough to justify a hostile bid premium, if you believe that you have ways to capture the SOTP value. I’ll discuss that question in the next section.

A real plan

SOTP based valuations are interesting and thought provoking. But they are only relevant if you have an actual plan to realise that value. What might Castlelake have in mind?

The easiest part to understand would be the attraction to Castlelake of the order book, given its background as an aircraft lessor. Delivery positions and purchase rights are not normally transferrable, so without securing an agreement from Airbus, Castlelake would have to take delivery of the aircraft at easyJet first before moving them on to other customers. That’s a complexity but could be done if Airbus refuses to play ball.

Selling off part of easyJet’s order book would of course require a revision to the airline’s plans. Their core business plan probably doesn’t need all the aircraft orders and purchase rights, so a partial sale might not have that big an impact. Also, remember that easyJet’s current financial performance isn’t great, so Castlelake probably assume they could rationalise easyJet’s network and free up aircraft without undue damage to the airline’s profits and cashflows. That’s almost certainly true in the short term. The longer term strategic risk is that this would signal weakness to competitors (cough, Ryanair), who might decide that this would an excellent time to apply a bit of extra competitive pressure and persuade the financial types who are now in command to pull back even more and sell more assets.

It is of course quite possible that Castlelake believe that financial performance can be improved, or that the business is just undervalued compared to its potential. But could Castlelake be considering a radical breakup plan? There would be issues with competition regulators for most of the large European airlines if they tried to buy the whole of easyJet. Some of them don’t have the financial resources to buy the whole of the business anyway. But if Castlelake were willing to auction off the airline’s network and related slots in pieces, they might find buyers prepared to pay a premium given the synergies and strategic advantages they would achieve.

The Stelios angle

A complication here is the position of the original founder, Stelios, and his family companies. Together they own about 15% of easyJet and they might not take kindly to a hostile bid and breakup plan. A 50% takeover premium would be worth £225m to them, but if it puts at risk the circa £25m of brand licence payments they receive each year that probably isn’t attractive financially, even leaving aside any emotional considerations.

The Stelios “concert party” couldn’t block a hostile bidder from taking control, but they could probably prevent a “squeeze out” to get to 100%. Nevertheless, Castlelake might be prepared to take that risk, as achieving control is probably sufficient for them to capture the kinds of value they might be looking to achieve.

Watch this space

I think I’m going to leave it here for now. I’m sure there will be more to analyse over the comings days and weeks. Whether that is further details from Castlelake, competing bids, or a more comprehensive response from easyJet. The first interesting data point will be to see how much the share price jumps when the markets open tomorrow morning. That will tell us a lot about the market’s assessment of the likelihood of a bid actually emerging.