EasyJet board accepts revised Castlelake offer

The price haggling reaches a conclusion

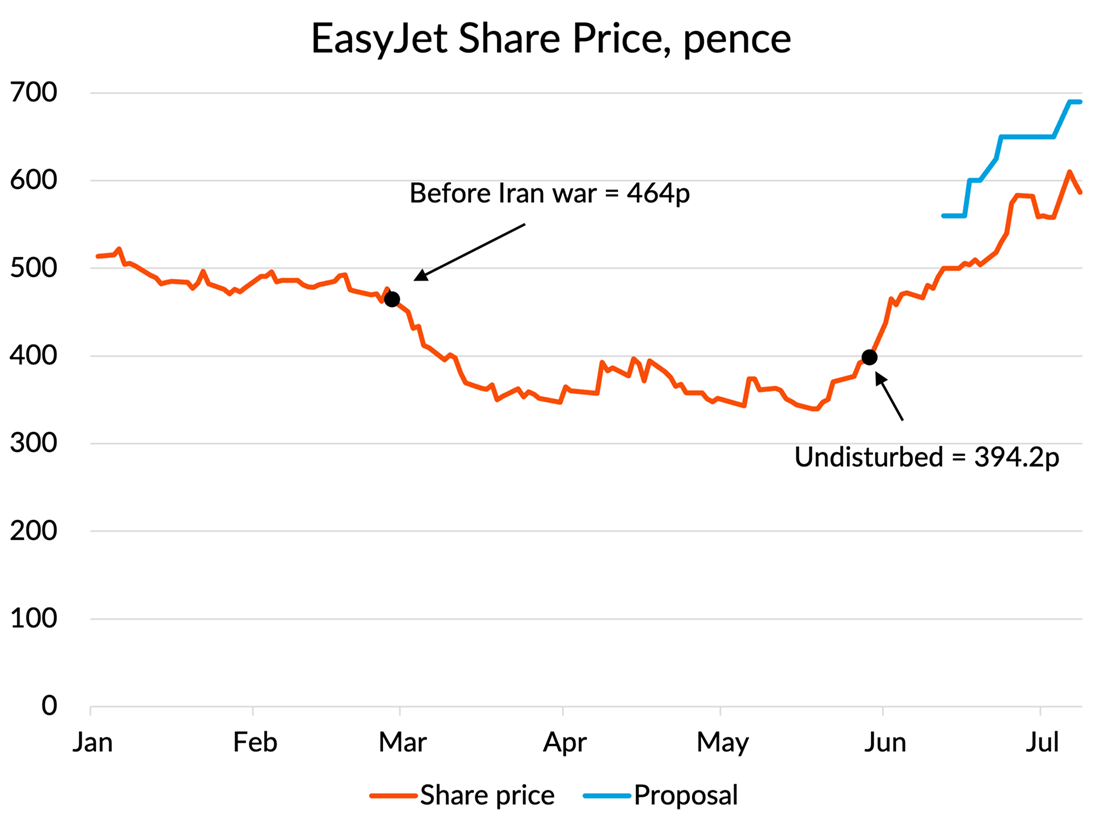

On 29 May, news of a possible offer by Castlelake emerged, although no intentions on price were disclosed. Over the course of the next five weeks, a series of non-binding proposals were made to the easyJet board by Castlelake, starting at 560p and then proceeding in steps to the final offer of 690p, which was conditionally accepted by the Board as something they would recommend to shareholders.

Is 690p a good offer? It values the business at £5.5 billion. That compares to the £5 billion “sum of the parts” valuation I calculated in my last post, so the bid clears that hurdle.

In terms of price/earnings ratio, Castlelake focuses on the consensus earnings per share of 37.9p for the year ending September 2027, which gives a P/E ratio of 16.5x. That’s about a 20% premium to Ryanair’s multiple on the same basis, for a company that has never delivered Ryanair-like performance.

Compared to the 394.2p easyJet traded at just before the news of a possible bid emerged (the “undisturbed price”), 590p represents a 75% premium, which is at the upper end of typical takeover premia paid in the UK market. I suspect that that price wasn’t genuinely undisturbed - you can see from the above chart that the shares had a significant run up in the days before the “possible bid” statement. I think it was probably that run up based on leaks that forced Castlelake’s hand in making an announcement, as would have been required under UK takeover rules. The genuine undisturbed price might have been as low as 340p.

The easyJet board argued that the share price was “temporarily” depressed by the war in Iran and the correct reference price is the pre-Iran war price of 464p. Compared to that, the proposal represents a 49% premium. That would still be above the 30-40% level that might be considered to be a “normal” takeover premium.

Overall, I’m not surprised that the Board decided to recommend the offer.

What is the chance of a deal going through?

EasyJet’s share price today is 587p, 15% below the offer price. That indicates a strong level of scepticism from the market about whether the bid will go through. You can work out the breakeven probability using assumptions about where the share price would go if the bid falls through. If you take the undisturbed price and uplift it by the 8% share price recovery seen at Wizz and IAG over the last few weeks, that gives you a “no deal” value of 426p. The 690p will only land in shareholders’ bank accounts in around 6 months, so I took 17p off for the time value of money giving me a “deal” value of 673p. Those assumptions give you a breakeven probability for the deal going through of only 65%. If you believe the share price wouldn’t fall back all the way if the deal fell through, then the market’s implicit “deal probability” would be even lower.

Why is the market so sceptical? The biggest issue mentioned is uncertainty about how Castlelake, a US company, will deal with the EU’s ownership and control restrictions, which require an airline that flies within the EU to be majority owned and controlled by EU interests. Let’s look at that one first.

Satisfying EU ownership and control requirements

Castlelake says that the US bid vehicle will only own 49% of easyJet post deal, with 51% held by an EU company which will at all times be owned and controlled by EU nationals, including two named individuals Peter Bellow and Mark Breen. Since it is unlikely that Peter and Mark are personally investing £2.8 billion, the structure is clearly more of a “legal device” to engineer around the problem without fundamentally changing the economics for Castlelake.

How might the structure work? Castlelake says that “This proposed structure is consistent with structures adopted by a number of other European airlines that are subject to the same EU ownership rules as the Company.” A number of European airlines have clauses which enable them to restrict the voting rights of non-EU shareholders as needed to ensure that EU shareholders have a voting majority. Those restrictions don’t affect the economic rights of the non-EU shareholders, so the structure could be as simple as the EU company having 51% of the votes, but minimal economic interest, whilst US shareholders have 49% of the votes but close to 100% of the economic interest.

I suspect the structure is more complicated than that. It is probably modelled on the “national control structures” that IAG put in place to protect the Spanishness of Iberia, the Britishness of BA and the Irishness of Aer Lingus. Whilst the structures are slightly different in each case, they share the same essential features. The national entities have an economic interest which is de minimus in normal circumstances, but there are a few legal “bells and whistles” to provide a bit more substance to their ownership rights (e.g. being entitled to a majority share of any proceeds in the event of a wind-up of the company). When it comes to voting, they have a majority vote, but are required to vote in accordance with IAG’s instructions, except where doing so would compromise the operating companies interests due to national control requirements. It is a legal structure which gives IAG full control unless a regulator or court decides it can’t have it on a specific issue. Like Schrödinger’s cat, the national control company exists in a superposition of two states when not being observed. If looked at by financial investors, it plays no real role and just follows IAG’s instructions. If looked at by regulators worried about ownership and control issues, it has majority control on any issue that the regulator says is important.

The IAG structures have been subjected to a number of legal tests over time and found to be robust. I’m certain that Castlelake will have taken good legal advice from people familiar with the IAG structures, so I suspect that this issue won’t in practice stand in the way of a deal going through. It was certainly an issue raised by easyJet’s board and apparently they got themselves sufficiently comfortable on it to move to a conditional recommendation of the deal.

The Stelios issue

EasyJet’s founder Stelios and his family own about 15% of the company. They also get a 0.25% royalty for use of the easyJet brand, worth about £25m a year. At the 690p bid price, they will pocket £825m, about £340m more than the value of their stake before the bid emerged.

Castlelake have made a provision for EU shareholders who want to remain invested post acquisition to do so via their EU vehicle. That’s not likely to be interesting to individual shareholders or regular institutional investors, since the stake will be highly illiquid. It is probably aimed at giving Stelios an option to “stay in” if he feels there is more upside to be had. The size of the Stelios family holding means that he could have more of a role as part of a privately owned company than he does today, if he wants it. I suspect that Stelios will decide to “take the cash”, at least on a big slice of his holdings. But whatever he decides, I think giving him an option is a very clever way of dealing with his possible objections.

The business plan

We still don’t really know what Castlelake intends to do with the business post acquisition. It has made a number of statements about its intentions to continue to grow and invest in the business, trying to deal with accusations that it plans to asset strip the company:

“Castlelake's ambition is to support easyJet as a stronger, more resilient European airline under European control respecting easyJet's valuable airline assets and continuing to sustain its network, serve the passengers who depend on them and enable future growth”

It is possible that a strategic airline investor will emerge over time as a participant in the deal. I’d be surprised if that happened before the deal goes through, as it would have the potential to raise competition issues which might complicate or delay deal completion.

My best guess is that Castlelake has a baseline plan, which continues the business largely as is, but with more aggressive management focused on financial delivery. I’d expect some management changes as part of this, but maybe some key individuals in the current easyJet team would be looked after, at least for a period. I don’t think it would be hard to justify the bid price on the basis of such a plan.

However, I would be amazed if Castlelake didn’t also have at least half an eye on the upside available from selling off the business, in whole or in part, to one or more strategic airline investors over time. Those airlines would struggle to buy easyJet as a whole, either for competition or financial capacity reasons. But a financially driven private equity investor would have no qualms about breaking up the business if it got offers it couldn’t refuse.

Another possibility is that Castlelake intends to use easyJet as a platform for further acquisitions in the European low-cost airline space. I would certainly agree that there is potential for more consolidation there and that easyJet needs to sell itself (maybe in parts) or build scale through acquisition. As a publicly quoted company, the acquisition path was tricky for a company with no real track record there. But backed by Castlelake, it could become a real option. My personal list of targets in their shoes would be Wizz and Jet2. The former would get access to a lower cost vehicle and the latter would help scale the Holidays business. Both would help reduce the scale gap to Ryanair.

Final thoughts

To summarise my conclusions here, I’d say I think the chances of the bid going through are much higher than the market is apparently assuming. The media headlines about easyJet being broken up or asset stripped are also I think overdone. Yes, it could happen, but I think the chance of Castlelake going in the opposite direction and using easyJet as a basis for growth by acquisition deserve at least an equal weight.

Only time will tell.