Tracking the recovery in European airline demand

A mid quarter update on European airlines’ progress in restarting operations

After the groundings of Q2, European airlines are now well into the Q3 restart phase. They have been steadily adding back capacity since late June, but the key question is, what is happening to passenger volumes?

The ultra low cost players are leading the charge

As predicted, the low cost airlines have recovered more quickly than the big flag carriers, even when looking just at short-haul travel. That is in part due to the fact that the fastest recovery has been seen in visiting friends and relatives (VFR) and leisure travel, with business travel continuing to remain moribund. They have also been the most aggressive in adding back capacity.

The two big ultra low cost carriers (ULCCs) publish monthly passenger figures and we can see that they both built back considerable passenger traffic in July, with Wizz back above 45% of July 2019 passenger volumes, albeit with load factors still weak at 60.5%. Ryanair only got back to 30% of last year’s levels, but managed a stronger 72% load factor.

Source: wizz.com, ryanair.com

Short-haul traffic is recovering at the big hubs too, but more slowly

The main hub airports of the European flag carriers also publish monthly statistics and I have also been able to split the passenger figures between short- and long-haul. Again, I have indexed the numbers to July 2019 levels.

Source: heathrow.com, schiphol.nl, parisaeroport.fr, aena.es, magairports.com, fraport.com

I’ve included Stansted airport on the chart for comparison. As the most important base for the ULCCs in normal times, you might have expected to see that airport showing the fastest recovery. In reality, the opposite is true. It is the furthest away from regaining 2019 levels of all these airports, reaching only 17% of last year’s volume in July, although it just about managed to catch up with Heathrow.

The fact that the two London airports were bottom of the list tells you something about the damage that the UK government’s policies on travel are doing, with constant shifts and a failure to take a targeted approach for its travel advisories and quarantine restrictions. It is clear that the ULCCs have been achieving their volume recovery in other markets.

Amongst this group, the best performing airports in July were in Paris, with short-haul passengers at the two airports almost reaching 30% of last year’s levels. That was helped by the relatively robust performance of the large French domestic market, which was only down 55% on last year, compared to a 76% fall in traffic to the rest of Europe. I can’t split the figures for short-haul between Charles de Gaulle and Orly airports, but in total passenger terms both airports performed similarly.

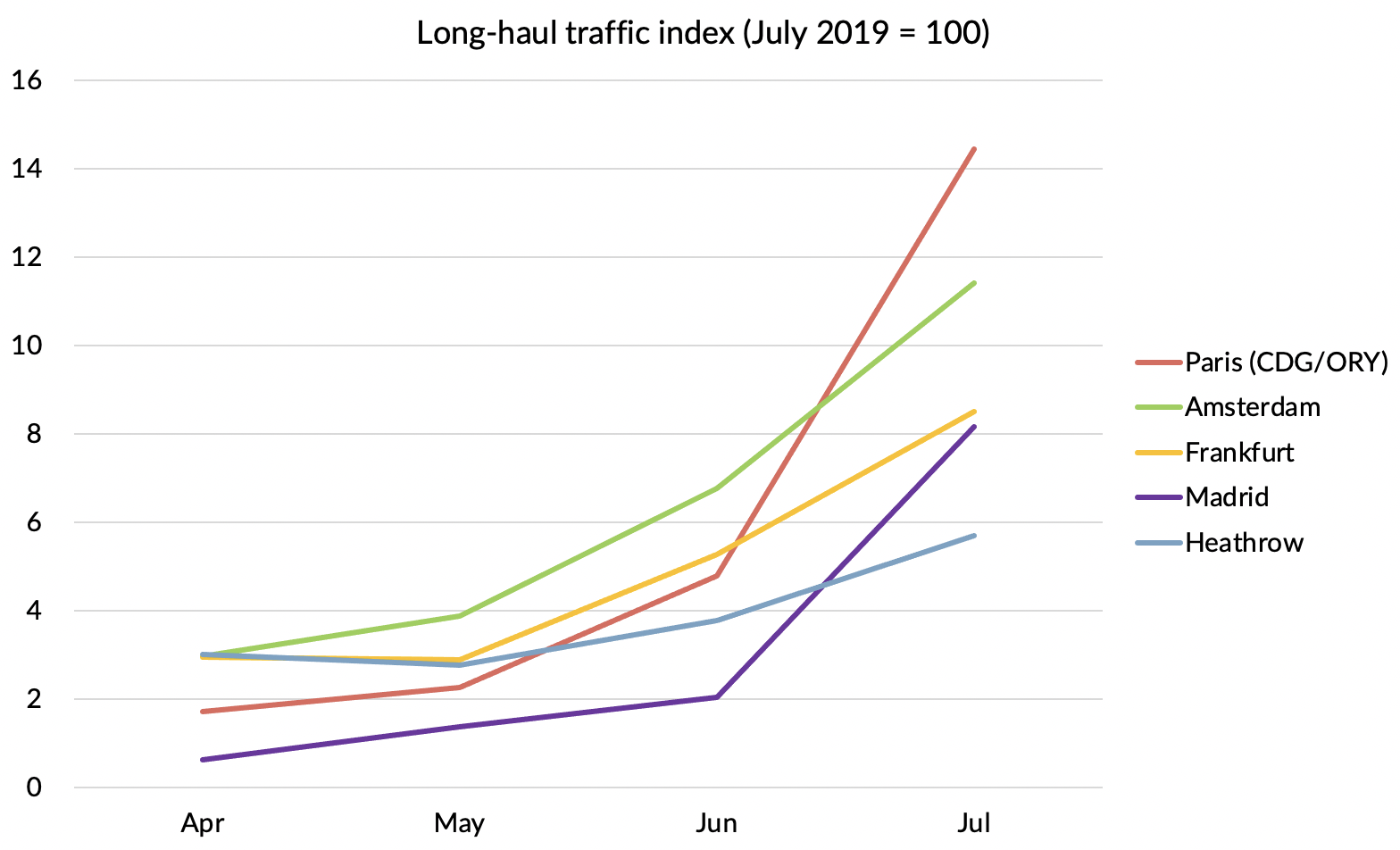

Long-haul shows signs of life

Whilst still lagging considerably behind short-haul (note the different scale on the chart), long-haul traffic showed some signs of life across Europe in July. Again, Paris led the way and Heathrow trailed in at the bottom of the league table.

Source: heathrow.com, schiphol.nl, parisaeroport.fr, aena.es, fraport.com

Has the virus killed the connecting hub?

One of the questions that has been speculated about is whether the pandemic would kill off the transfer hub. For those who think that it will, the theory seems to be that people will avoid hubs going forward, worried about the dangers of contracting the virus whilst making a connection.

I always thought this was a load of rubbish and the power of hubs to concentrate traffic would be even more essential in an environment where market sizes have shrunk.

The evidence to date seems to show that the hub remains very much alive, at least as much as any part of the industry is at the moment. Connecting traffic as a proportion of the total fell slightly at Amsterdam, from 34.2% last July to 31.1% this year. At Paris, the figure also fell, but only slightly.

Given that both Schiphol and CDG are both designed around connections to long-haul, the fact that transfer mix hasn’t fallen further despite the relative weakness in long-haul provides good evidence that hubs remain a key strength for airlines in dealing with the collapse in demand.

What about August?

Source: fraport.com

Frankfurt is the one airport which publishes weekly passenger statistics, albeit only giving a total figure for all passengers at the airport. That gives us some indications for how August is going and it certainly presents a worrying picture, with the recovery stalling at the start of the month and going into reverse last week, although weekly figures can of course be volatile.

However, this picture of a stalling recovery matches with the announcement by Ryanair last week that they were cutting capacity for September and October by 20%, reporting that “forward bookings have notably weakened over the last 10 days”. Capacity cuts will be focused on Spain, France and Sweden, where upticks in COVID-19 cases have led to increased travel restrictions.

Wizz also noted yesterday that ticket data showed that Europe's travel recovery began to stall in August and that 80% of normal capacity was as high as they could go under current circumstances, warning that capacity might fall again.

It seems that even the all conquering ULCCs are not immune to Trump’s “brilliant enemy”, or to the blunt edged and unpredictable swings in government travel restrictions that are being deployed in an effort to contain it.