Low-cost airline hibernation skills

Amidst all the drama about the "non-reopening" of travel from the UK, we got the March 2021 financial results for Wizz a couple of days ago, which means we now have figures for all three of the biggest independent low-cost carriers in Europe.

For all European airlines, the last six months have largely been an exercise in minimising losses as the second wave engulfed Europe and most European travel markets were subject to heavy travel restrictions.

How did they each do?

Capacity and load factors

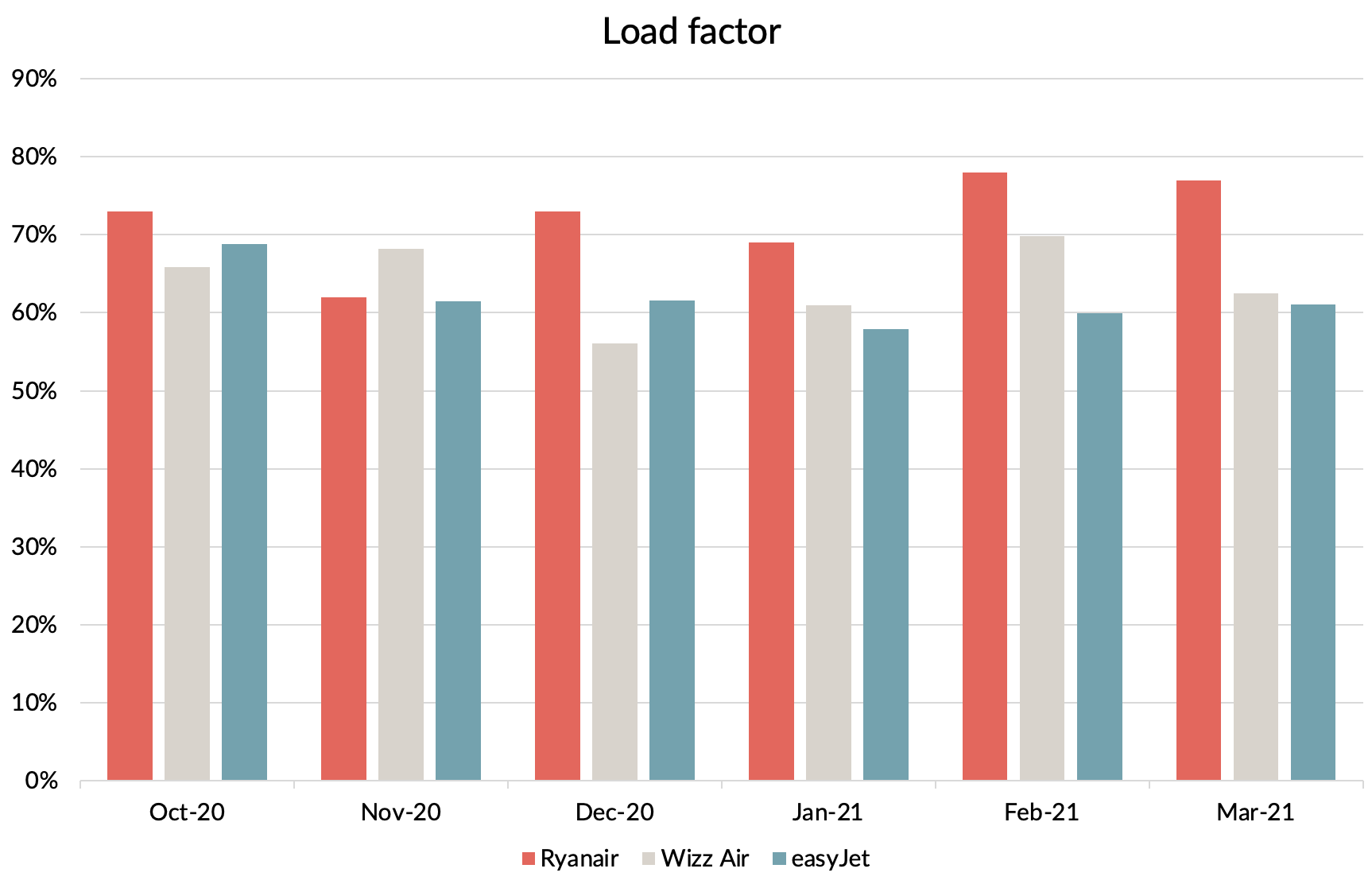

The three carriers took somewhat different approaches to capacity over the last six months. Operating an average of 30% of its pre-pandemic capacity, Wizz flew the most. At the other end of the spectrum was easyJet at only 15%. Ryanair were in the middle.

From a load-factor perspective, Ryanair’s “Goldilocks” capacity strategy, together with their traditional load-focused approach seemed to work the best. They averaged a 69% load factor for the period, well down on the 95%+ that they used to achieve pre-pandemic, but still 5 points higher than easyJet and 6 points higher than Wizz. Although easyJet did slightly better than Wizz overall, that was all achieved in October and December. Wizz has been doing better in 2021, presumably due to its lower UK exposure.

Source: Company reports

Ryanair’s over-performance on load factor did not flow through into unit revenues, with higher volumes more than offset by revenue per passenger declines. Overall, Ryanair was actually the worst performing of the three, with Wizz the clear winners achieving revenue per seat equal to 82% of last year. That’s quite impressive in the circumstances, especially as they operated the most capacity of the three.

Source: Company reports, GridPoint analysis

Costs to the rescue

As we have come to expect, Ryanair was the king of the hill in terms of cost management. It reduced its cash operating costs by more than easyJet, despite cutting capacity considerably less. WIzz achieved a similar unit cost performance as Ryanair, but with the benefit of much smaller capacity cuts.

Source: Company reports, GridPoint analysis

The bottom line

During this period, it was all about minimising losses and overall, Ryanair did the best job. Operating losses per aircraft were 36% lower than at easyJet.

Source: Company reports, GridPoint analysis

The bottom line results at easyJet and Wizz were surprisingly similar, given the very different approaches they took to capacity during the period.

Despite all the positive hype around Wizz, I’d still say that Ryanair continue to show themselves as the class act amongst the low-cost players in Europe.