Digging around in Ryanair’s Q3 results

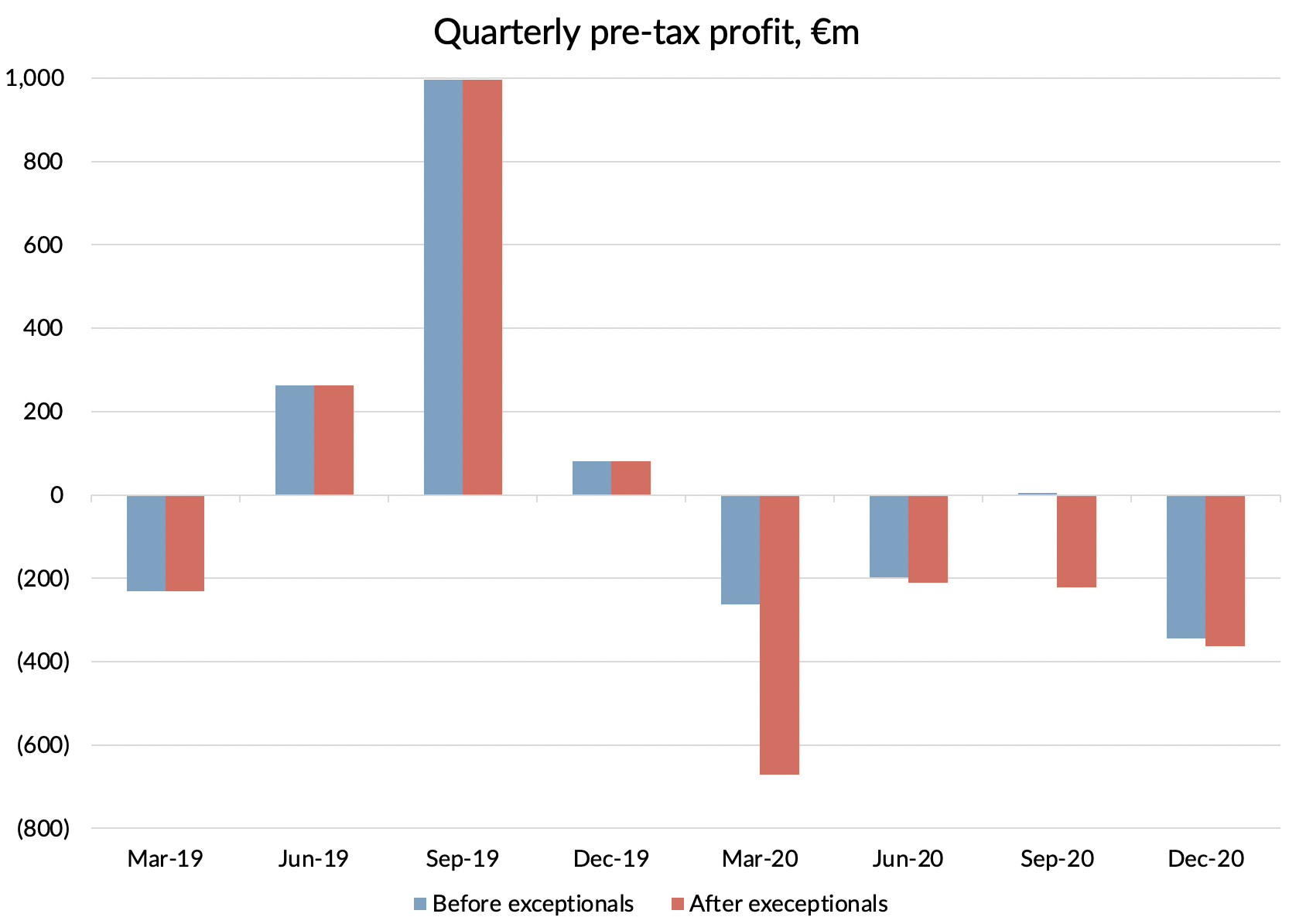

Record losses in the December 2020 quarter

This week Ryanair reported record quarterly losses of €345m at a pre-tax level for their third fiscal quarter.

They also guided for a net loss for the year ending March 2021 of between €850m and €950m. The middle of that range would indicate a pre-tax loss of about €450m for the upcoming March quarter. So things are expected to get worse before they get better.

Whilst the results were pretty bad, they were better than those at rival easyJet, who clocked up £423m (€480m) of losses for the quarter, despite being the smaller company.

This was mainly down to cost performance. easyJet only disclosed “Headline Costs”, which is a figure including all non-exceptional operating costs plus net financial expenses. That figure fell by 59% at easyJet, on a capacity reduction of 82%. Even though Ryanair flew quite a bit more capacity, which was down “only” 69% on last year, absolute costs on the same basis fell further, with a 62% reduction.

I've already looked at Ryanair’s capacity and load factor performance compared to their peers in my post about the easyJet results. That showed that whilst the quarter was ghastly for everyone, Ryanair did relatively well compared to the other big low-cost carriers in Europe.

The additional piece of information we now have is for revenue per passenger, which was down 21% at Ryanair. That was worse than easyJet’s decline of 10% and, even allowing for Ryanair’s stronger load factors, revenue per seat was still worse with a 42% decline compared to easyJet’s 35% drop. But since Ryanair flew more capacity, total revenue “only” fell by 82%, compared to easyJet's 88%.

The company recently announced it was increasing its order for Boeing’s troubled 737 MAX aircraft, adding 75 aircraft to take the order to 210 firm aircraft.

I thought there might be some interesting information about the deal buried in the accounts and I wasn’t wrong. But to find it required quite a lot of detective work digging around in the balance sheet.

Big movements on the balance sheet

During the first nine months of Ryanair’s fiscal year, “Property, plant and equipment” balances went from €9,438m in March 2020 to €8,554m at the end of December. That’s a reduction of €884m, or almost 10%. Most of the decrease happened in the third quarter.

What happened to cause such a big drop? Depreciation over the nine months was €439m, so on the face of it we appear to have a negative capital expenditure of €445m.

The first clue to what is going on is provided by the following comment in the notes to the accounts:

Net capital additions for the nine-months ended December 31, 2020 amounted to a credit of €0.5bn, principally reflecting the reversal of certain aircraft pre-delivery trade payables, supplier reimbursements of €0.3bn offset by capital expenditure €0.2bn.

€445m doesn’t round to €0.5 billion, but close enough I think. Let’s take a look at each of the three elements referred to in this note, starting with the reimbursements from the mysterious “supplier” (cough, Boeing).

Boeing cash-backs

In the Q2 (June) accounts, reference was made to “supplier proceeds”, which I assume are the same thing as “supplier reimbursements”. A more precise figure of €250m is given there. That rounds to €0.3 billion, so I think that is the real figure.

There was no obvious place for a €250m cash-back from Boeing to be hidden in the profit and loss account for Q2, so I don’t think this money was booked to P&L. We therefore need to look in the balance sheet to find out where it ended up.

At the end of March 2020, Ryanair had €1.3 billion of advance payments for aircraft sitting within its fixed asset balance. You might think this was the amount of pre-delivery payments for 737 MAX aircraft that Ryanair had made to Boeing. But actually, it is the amount that they had been invoiced under the contract. They had stopped paying these invoices back in 2019 due to the MAX delays and by the end of March 2020, there were almost €1 billion of unpaid invoices to Boeing sitting in “other trade payables” on the balance sheet.

That means that Ryanair had only made €0.3 billion of pre-delivery payments to Boeing and it looks to me like Boeing refunded even those in Q2, no doubt under some pressure from Ryanair, keen to make their cash balance look better in the midst of the pandemic.

I think it is also worth pausing to consider that at the end of September, €1.3 billion or around 14% of Ryanair’s tangible fixed assets consisted of aircraft pre-payments for which they hadn’t actually made any payments.

We all know that Michael O’Leary is the master of spin, but this one did rather take my breath away.

Capital expenditure

The cash flow statement for the nine months to December shows a figure of negative €114m for capital expenditure, again labelled as “net of supplier proceeds”. Reversing out €250m from that gives us a figure for capital expenditure of €364m. Q2 had €108m of capital expenditure, which was described as mainly heavy maintenance checks, so perhaps this figure is mainly made up of three quarters of the same.

But €364m doesn’t round to the €0.2 billion referenced in the note. Ryanair classifies pre-delivery payments as capital expenditure (even when they are not paying the invoices). Periodically they do come back and reclassify them in the cash flow statement, as they did the previous year:

Operating cash inflows and investing cash outflows for the nine month period ended December 31, 2019 have been reclassified. They both have been reduced by €0.9bn to reflect accrued supplier payables which had previously been presented as capital expenditure in the consolidated cash flows.

Quite what they have done in the current financial year is murky at best. My guess is that the €364m figure actually contains €150m or so of unpaid pre-delivery invoices in the current year which were excluded from the €0.2m capital expenditure figure in the note. Heavy maintenance checks are notoriously lumpy and the fleet was grounded in Q1, so it is entirely possible than they only spent €200m or so on checks in the nine months.

Which leaves us just one part of the note to pull apart, the “reversal of certain aircraft pre-delivery trade payables”, which somehow reduced fixed assets by about €0.4 billion.

Trade payables

Going back to the March 2020 accounts, we know that Ryanair had €957m of unpaid invoices from Boeing at that time, included within “other trade payables”. If there was indeed another €150m added during the next nine months, that would take the figure to about €1.1 billion by the end of December.

The total amount of “other trade payables” at the end of December stood at €511m, down from €1.4 billion in March. Of that total, €305m is listed under current liabilities (i.e. due in the next twelve months) and €207m is shown under non-current liabilities (i.e. due in more than twelve months). Back in 2019, before they started racking up unpaid invoices from Boeing, Ryanair used to have trade payables balances of about €350m. So it looks to me like the current liabilities portion is the “normal” bit and the more than twelve months part is for pre-delivery payments to Boeing that don’t need to be paid until 2022. That looks to me like they’ve hidden an €207m interest free loan from Boeing that doesn’t need to be repaid until 2022 or later in their “other trade creditors” line.

Apart from that €207m piece, there doesn’t seem to be any room left for unpaid Boeing invoices in the December balance sheet.

So where did the remaining €0.9 billion of unpaid invoices go? We know where €0.4 billion of it went. It was netted off both sides of the balance sheet, reducing the pre-payment balances held in fixed assets. But we still have €0.5 billion unaccounted for.

Staring me in the face

You won’t believe how long I puzzled over this missing €0.5 billion. I just couldn’t see what was staring me in the face. How do unpaid invoice balances normally disappear without hitting the profit and loss account?

They get paid, of course.

That’s right. It is now obvious to me that Ryanair ponied up around €0.5 billion of cold, hard cash and wired it to Boeing. It makes perfect sense that this would be part of signing a new deal. 24 aircraft deliveries are due to arrive within 3-4 months with many more to follow. As we saw earlier, Boeing seemed to have refunded all the pre-delivery payments made to date so a considerable amount must have been due and given the history, Boeing will have wanted to see real cash up front this time.

Why did it take me so long to see the obvious? I think it is mainly because I had watched the Q&A section of Ryanair’s third quarter results presentation, available on their investor relations web site. Most other airlines do conference calls with real analysts asking searching questions, which are then made available to all investors. Ryanair do a staged “mock Q&A”, with employees asking the questions. One of them was about why the cash balance had fallen so much during the quarter:

Deferential questioner: “Gross cash fell by €1 billion since the end of H1, why?”

Michael O'Leary: “Well cash generally falls in the third quarter, even in a normal year. However this year we’ve seen an acceleration of passenger refunds into the third quarter, particularly as more flights were short notice cancellations, particularly around the Christmas / New Year period. Deferred route charges from Eurocontrol became payable and due in the quarter and we still continued to fund ineffective swaps which were settled during the period.”

No mention of the Boeing deal. Extraordinary.

You almost got me again, Michael.