Another £342m of pre-tax losses at Virgin

Virgin reports a sixth successive year of losses

Virgin Atlantic has just reported its 2022 results. Once again, it was a pretty sizeable loss, adding up to £341.6m before tax. The company also indicated that they expected to be loss-making again in 2023, but said that they planned to return to profitability in 2024.

The last time Virgin Atlantic reported a pre-tax profit was in 2016. Since then, they have racked up a cumulative £1.9 billion of losses, which by all accounts will be added to next year. As the old saying goes, “How do you become a millionaire in the aviation business? Start off as a billionaire”.

It would be easy to take cheap shots when the headline results are as awful as these were. But instead let us dig a little deeper and try to figure out what is going on.

Profit and loss trends

Rather than the headline statutory accounting figures, Virgin Atlantic likes to focus on a measure of “underlying profits before exceptional items”. The “exceptional items” part of that is relatively straightforward, being made up of the usual “big one-off items” like restructuring costs, aircraft write-downs and such like. Obviously there have been quite a few of those over the last few years.

The part that is harder to wrap your head around relates to fuel and currency hedging. In its underlying profit measure, only realised losses and gains are recognised. The element that relates to as-yet unrealised gains or losses from marking hedges to market is excluded. The best argument for doing that is that those unrealised gains or losses relate to future periods. Assuming that the company is successfully managing to reduce risk with its hedging activity, there will be offsetting gains or losses in future revenues or costs. Many companies employ what is called “hedge accounting” to explicitly match the timing of when hedging gains and losses are recognised in the profit and loss account to those real world exposures. Virgin doesn’t do that, so in their statutory numbers, they get a lot of volatility which they try to adjust out in the underlying profit figures.

There is one other adjustment they make to get to the underlying profit measure, which relates to the nature of their loans from their shareholders. We’ll come back to that topic later, but for now you just need to know that in their underlying profit measure, these loans are treated as not having a cost.

In any event, I think that the underlying profit figures have quite a lot to recommend them if you are trying to understand the trend in current year profitability, excluding big one-off items. The chart below sets out what they show, on both a pre- and post-financing cost basis. I’ve also included the statutory post-financing numbers to show you how they differ.

Source: Company accounts, GridPoint analysis

You can see that before financing costs and exceptional items (essentially the same measure as “operating profits”), Virgin Atlantic made small profits before the crisis. But those weren’t quite enough to cover its interest costs, let alone provide a surplus to cover one-off costs (which tend to recur quite frequently in the airline business), or to provide a return to shareholders.

In 2022, the company almost managed to get back to breakeven on underlying operating profits. However, the amount of interest cost they now need to cover has more than doubled, even on the “underlying” basis, which treats shareholder loans as zero cost.

Source: Company accounts, GridPoint analysis

The company has two challenges if it is to start making money again. Firstly, it needs to boost operating profitability. Getting back to the 2-3% margins it made before the crisis isn’t going to be enough. The second problem it has is to sort out its overstretched balance sheet, so that it can bring down finance costs to affordable levels.

Let’s look at the two issues in turn, starting with the revenue side of things.

Revenue in 2022

Capacity measured in ASKs reached 80.6% of 2019 levels, with seat factors down 7.5 points versus pre crisis levels. The average passenger fare was up 25.7% (27.7% on a per RPK basis as best I can estimate it). The price increases were more than offset by the volume losses, so passenger revenues were down 6.3% on 2019. But relative to capacity, unit revenues per ASK were up 16.2%.

I’ve put that performance next to the equivalent metrics for 2022 from rival British Airways. Of course, there will be a big route mix effect, especially due to BA’s short-haul route network. But I think this comparison shows that Virgin’s revenue performance was pretty good overall. BA started from a better place in 2019 due to a stronger mix of premium traffic, but that has been slower to come back than the leisure market where Virgin Atlantic has always been strong.

Source: Company reports, GridPoint analysis

Virgin Atlantic’s revenue performance in 2022 was achieved despite a difficult start to the year, with COVID related travel restrictions still in place in the UK until March 18th.

Virgin Atlantic gave us a chart showing how passengers and load factors evolved over each quarter of the year, but I think we can do better using CAA data. That enables us to see how ASKs and RPKs compared to 2019 on a month by month basis (see next chart) and also gives us data for the first two months of 2023. You can see how depressed the first half was compared to 2019, and how much better 2023 is going to be, at least in volume terms.

Source: CAA, GridPoint analysis

I should briefly mention cargo revenue too. Although volumes and yields have started to fall from the hugely inflated levels they reached during the pandemic, cargo revenue was still 76% higher than in 2019 due to yields which more than doubled. Other revenue (mainly the non-flight element of Virgin Holidays packages, I think) was down 19.3%.

Altogether, overall revenues were down only 2.5% from 2019 levels and total revenue per ASK (RASK) was up 20.9%.

Operating costs

On Virgin’s “underlying” basis, total operating cost per ASK (CASK) was up 24.0% on 2019. Since that was slightly more than the increase in RASK, operating profit margins fell.

As I did with revenues, I’ve shown the performance compared to BA. Unit costs at BA undoubtedly suffered from the slower recovery of capacity, which showed up in particular in “Property, IT and other costs” which is where the big fixed costs lie. But even allowing for that effect, I think Virgin did a better job of managing its non-fuel costs than BA.

Source: Company reports, GridPoint analysis

Where BA did a lot better was on fuel costs, which only rose by 36.3% per ASK compared to 70.7% at Virgin. That was undoubtedly driven by different hedging positions. Virgin’s balance sheet constraints will have made it hard for them to hedge heavily, whether they wanted to or not.

It is a bit hard to compare the per ASK figures, since the networks are so different. But we can get a good idea for how much of the difference in performance was down to price. Using the CO2 emissions data both companies publish, we can calculate the fuel volumes and therefore the average cost per tonne. Including the benefit of the small hedging gains they made of £18m, Virgin paid £901 per tonne in 2022. That is 16% higher than the £776 per tonne paid by BA.

Virgin operating margin compared to BA

If Virgin had paid the same for its fuel as BA, it would have made £123m higher profits. That would have taken it to an operating margin for the year of 3.6%, almost a point better than BA managed to deliver.

To be fair to BA, the company has an 86% share in IAG Loyalty which was worth about £207m in operating profit during the year. The profits from that are recorded below the operating profit line, whereas the money Virgin makes from its loyalty scheme is included in operating profit. Including BA's share of the loyalty numbers would have boosted its operating margin to 4.6%. But even so, my conclusion is that the operating profit performance of the two companies was remarkably similar, once you adjust for the different fuel hedging policies.

Prospects for operating profits in 2023

As we’ve seen already, 2023 passenger revenue should be substantially up on 2022. The company is planning to operate 16% more capacity and passenger load factors will be stronger too without the poor start to the year. All the industry commentary is that passenger yields are holding up, despite the extra capacity and economic pressures on consumers.

Cargo revenues will undoubtedly fall, despite the extra flying. CAA data shows Virgin’s cargo volume was down 20% versus last year in the first two months of 2023. Industry data showed transatlantic yields down 43% in April compared to last year.

Operating costs will rise due to the extra activity, but higher volumes should help bring down unit costs and provide an offset to inflationary pressures. Landing fees at Heathrow are set to fall considerably following the CAA’s final decision on charges.

But the big benefit on the cost side will be fuel, since fuel prices have fallen considerably since 2022. Assuming that Virgin Atlantic didn’t suddenly change its policy and start hedging its fuel heavily at the beginning of 2023, it should be well positioned to benefit from the fall in prices. At current fuel prices, their annual fuel bill would have been about £300m lower than it was in 2022 on the same volume. That's over 10% of 2022 revenue and would transform the operating results. Some will be lost to hedging and to lower prices as fuel cost savings are passed on to customers later in the year, but the net benefit should still be significant.

Taking all this together, I would have thought there should be every prospect of a meaningful operating profit in 2023.

Yet the company is apparently still pessimistic about its ability to be profitable in 2023. As we saw earlier, they have a lot of finance costs to cover, so let us move onto the other part of Virgin’s challenges, its overstretched balance sheet.

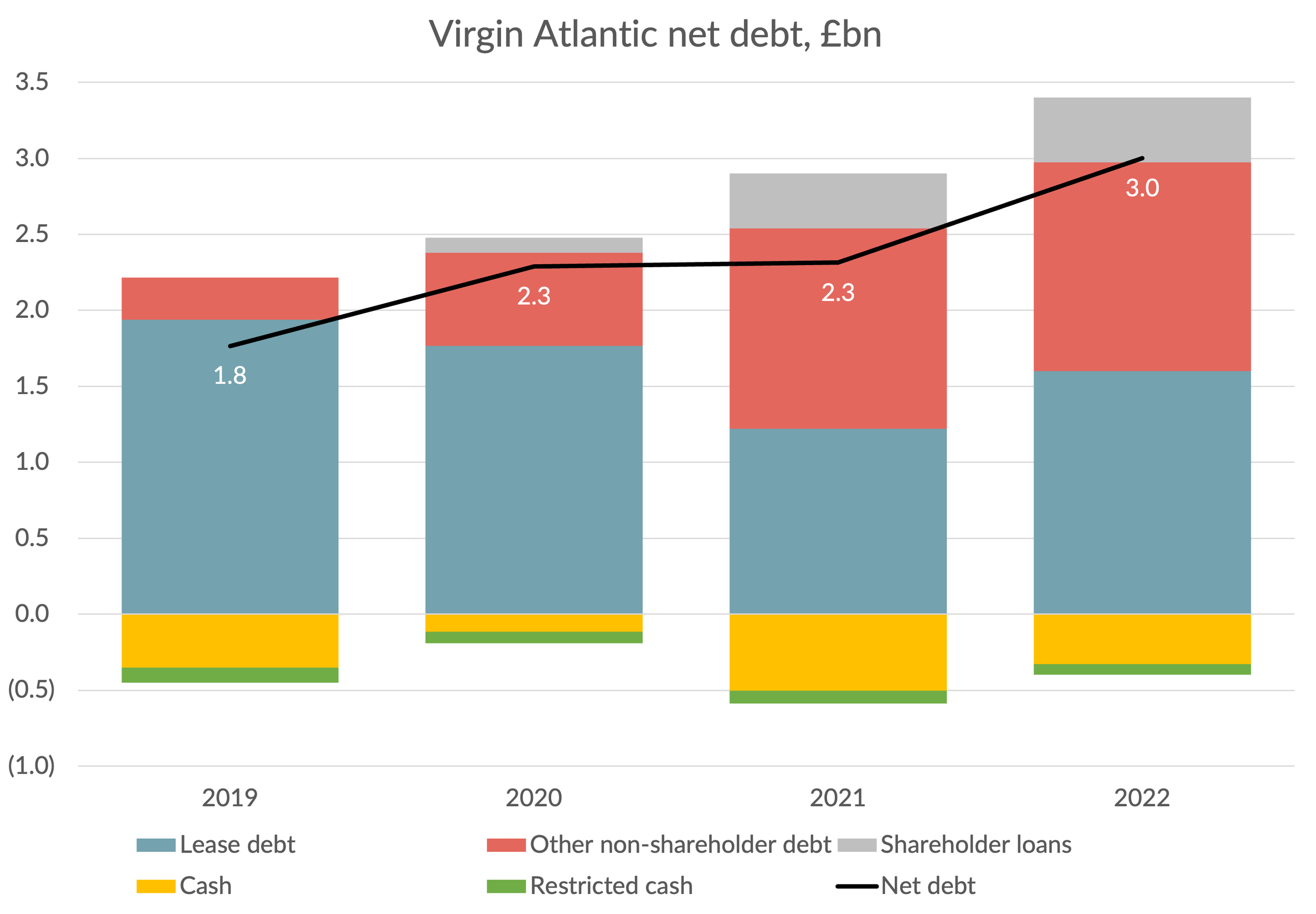

The weight of Virgin's debts

Virgin Atlantic went into the pandemic with £1.8 billion of net debt and it continued to take on new debt obligations during the crisis. The net debt figure now stands at £3.0 billion, up £700m in 2022 alone.

Source: Company reports, GridPoint analysis

There is £1.6 billion of lease debt, and another £1.1 billion of dollar denominated debt which is undoubtedly secured aircraft financing. It includes about £780m of debt associated with sale and lease-backs from prior years which the accountants subsequently found did not qualify as leases and were reclassified as loans. In any event, £2.6 billion of Virgin Atlantic’s debt is dollar denominated, equivalent to $3.1 billion at the year end exchange rate of 1.21. £249m of the increase in debt during 2022 was due to currency revaluations as the sterling exchange rate fell against the dollar from its starting rate of 1.35. At the peak of the Lis Truss debacle in September, when the pound sank to a low of 1.07, the company must have been pretty alarmed. At that exchange rate, the year end debt would have been another £340m higher.

The pound has recovered a little more since the end of 2022, so that should be helpful in 2023.

Source: Yahoo Finance

One thing that will drive increases in finance costs is new aircraft deliveries. During 2022, Virgin Atlantic took delivery of two A330-900s and one A350-1000. This was one of the reasons their un-discounted lease commitments went up by £547m, despite making £139m of lease repayments. Whilst those deliveries were already reflected in Virgin’s year end debt, there will be a full year effect in the profit and loss account through higher interest costs this year. In 2023, they have already taken delivery of two more A330-900s which will need to be paid for, plus any other subsequent deliveries.

Even though most of Virgin's financing is at fixed rates, with dollar interest rates having risen by about 5% since the start of 2022, new aircraft financing will also be more expensive.

Shareholder loans

Earlier in this article I said I would come back to the topic of shareholder loans and how these are accounted for. We saw in the last section that part of the increase in Virgin’s gross debt was due to increases in shareholder loans. Most of the money that Virgin Atlantic raised from its shareholders during the pandemic came in the form of loans, with £275m in 2020 and another £422m in 2021. Of the total £697m raised, £206.9m came from Delta and the rest from Virgin Group.

I’m pretty sure these loans were interest free, but since that was understandably not seen by the accountants as representing an “arms length” interest rate, the accountants did as they often do these days and made up some numbers accounted for the loans using “fair value” accounting. What that means in practice is that initially only £351.7m of these loans were recorded as debt. This is a calculated figure, based on the present value of a £697m repayment in November 2026 with no payments in the interim, discounted using a “fair value” interest rate. I calculate they must have used something like 14% per annum. The rest was treated as an equity contribution. Since Virgin Atlantic isn’t making any interest payments, each year the notional interest gets added to the shareholder debt, increasing the interest charge each year as interest is charged on unpaid interest. At the end of December 2022, the amount of shareholder debt shown in Virgin Atlantic’s balance sheet was £426m. That is still £271m less than the amount that will need to be repaid in November 2026. That £271m will flow through the P&L statement as notional interest payments over the next four years, adding to the debt even if no further loans are extended by shareholders.

As we saw earlier, management adjusts out all the notional interest payments on shareholder loans when considering underlying profits. In 2022, that was a £62.6m adjustment and it will get bigger next year for the reasons discussed above.

Cash and liquidity

Virgin’s unrestricted cash balance at the end of 2022 was £328.7m, equivalent to 11.5% of revenue. That’s not dissimilar to the £352.6m (12% of revenue) figure they had at the end of 2019. But it is still very tight for an airline. BA by contrast had cash equal to 23% of revenue at the end of 2022 and there is cash equivalent to 14% of group revenues sitting at the IAG group level and in the Loyalty arm.

Virgin Atlantic’s 49% shareholder Delta also has oodles of cash, with liquidity of $9.5 billion at the end of March 2023. However, ownership and control restrictions would prevent it putting in more money in the form of equity, unless it could be matched by the Virgin Group. Back in 2021, Richard Branson sold $300m of Virgin Galactic shares, presumably to fund loans to Virgin Atlantic. However, he can’t repeat that trick again, since the subsequent fall in the share price of Virgin Galactic means his remaining stake is only worth $140m. On the other hand, Forbes estimates Richard Branson’s personal net worth at $3 billion, so I guess he could find more cash from somewhere if he wanted to.

What the company really needs is more equity, but with debts £1.5 billion higher than its assets, it will be hard for anyone to justify putting in more money until the company shows that it can generate proper levels of profit and cashflow. The company likes to present adjusted net liability figures by adding in the value of its slot portfolio. But even on that basis, the company had net liabilities of £913m. That’s more than the balance sheet value of its shareholder loans.

So all roads lead back to the need for Virgin Atlantic to start generating profits. What are the prospects of that in the near term?

Prospects for pre-tax profits in 2023

In 2022, net finance costs were £206m, excluding notional interest on shareholder loans. For the reasons we’ve just explored, I think that this is likely to go up a bit in 2023.

We saw earlier that there are good reasons to believe that Virgin Atlantic will start to generate operating profits in 2023, assuming yields hold up and fuel prices stay where they are. Playing with a few assumptions, I could see them achieving operating profits of £300m or better. That would be approaching the double digit operating margins that well-performing airlines target and would be enough to generate a small pre-tax profit on an underlying basis in 2023. Making a profit on a statutory basis will be a tougher task, with another £70m or so of interest on shareholder loans to cover.

Digging itself out of its financial hole

Virgin Atlantic’s management say that 2023 will be “a year of delivery towards achieving our vision of becoming the most loved travel company and sustainably profitable”.

That’s a nice vision, but what does “sustainably profitable” really mean?

Even if Virgin Atlantic manages to start making pre-tax profits of £100m a year, it would still take the company fifteen years to eliminate its negative equity. I can’t see how the company will generate anywhere near enough cash to be able to repay £697m of shareholder loans in November 2026, so the status of those shareholder loans will have to be addressed before then.

If the shareholders agree to write off their loans, the company’s negative net worth would immediately shrink to £1.1 billion. Notional interest on those loans would cease to go through the P&L, improving headline results by circa £70m a year. If Virgin Atlantic could somehow match the 15% operating margin that BA managed pre-crisis, pre-tax profits would rise to something like £300m a year. Add a bit of growth and the company could claw its way back out of its negative equity position within three years. That kind of performance level would also support a real injection of equity capital to get to a decent balance sheet that would be resilient to future shocks.

A more plausible scenario based on the past would be a “muddling through” approach. The shareholders would dribble in small amounts of additional cash in the form of loans as needed to avoid default on the debts, and to maintain a barely adequate level of liquidity. The term of existing shareholder loans will be extended, to the extent required to avoid admitting they can’t be repaid. “Being loved” will trump “being sustainably profitable”, and getting to breakeven will be regarded as “mission accomplished”.

A critical year ahead

I am unclear whether the company has actually given up on getting back to profitability in 2023. Perhaps they are just being cautious in public, with internal targets which are much more ambitious. I also don’t know what the shareholders are going to do, if anything, about sorting out the company’s balance sheet.

What I do know is that Virgin Atlantic is still a great brand and, like everyone in aviation, its people have been through a lot over the last three years. I’m certainly hoping that when I write next year’s article, I won’t be lamenting a seventh successive year of losses.